Market outlook: reshaping the global energy map — 12 weeks of the conflict

More than 80 days into the 2026 Middle East conflict, global energy markets have moved from acute disruption into a stabilised crisis regime, one in which disruption is managed but not resolved.

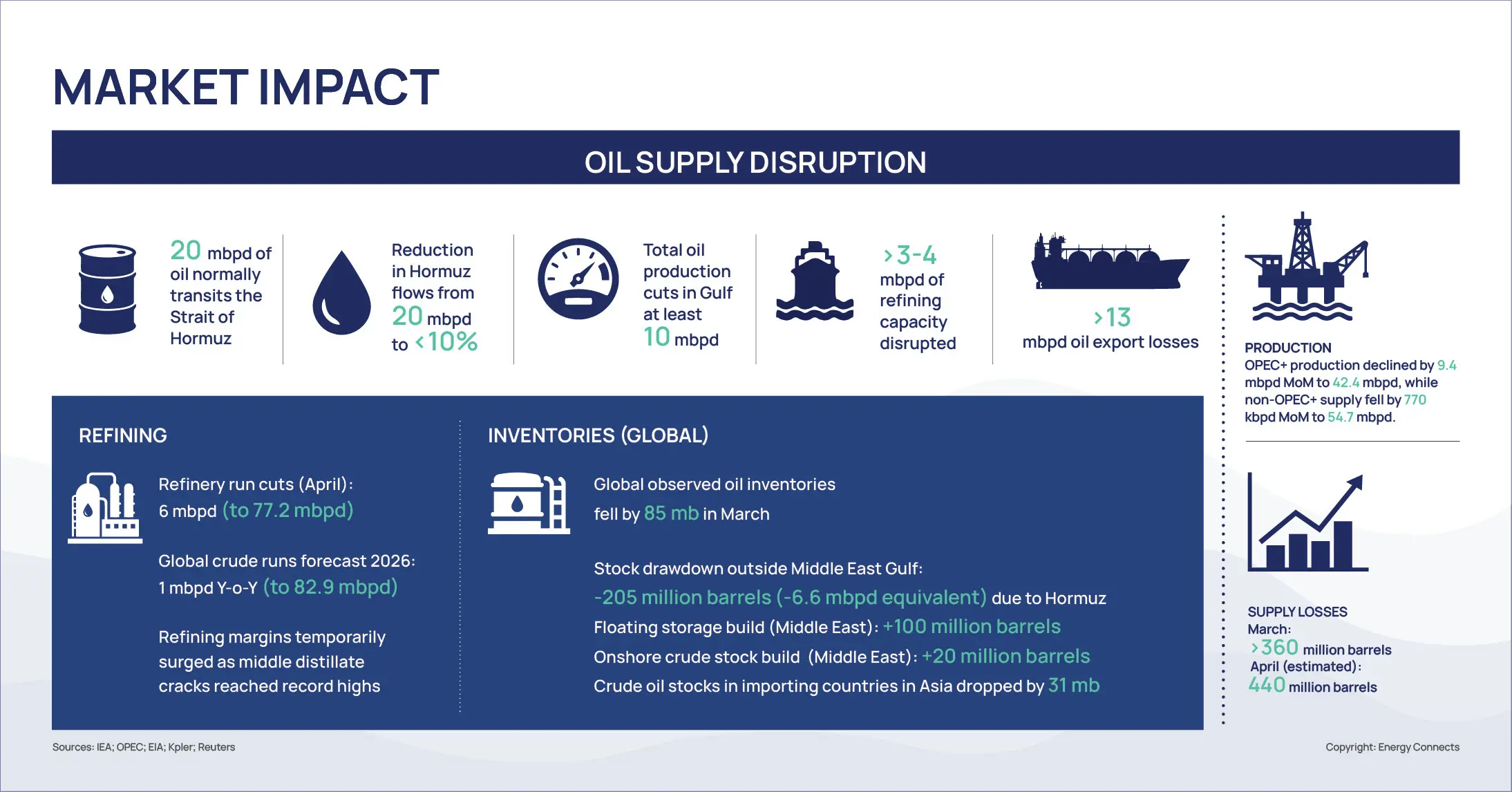

At the centre of the disruption lies the Strait of Hormuz, through which approximately 20 million barrels per day (mbpd) — close to 20% of global oil consumption, and around 20% of global LNG trade — typically transits. This disruption, described by experts as the largest oil supply disruption in history by affected volumes, has acted as a real-time systemic stress test, triggering immediate shocks across oil and gas markets, freight and insurance costs, and industrial supply chains.

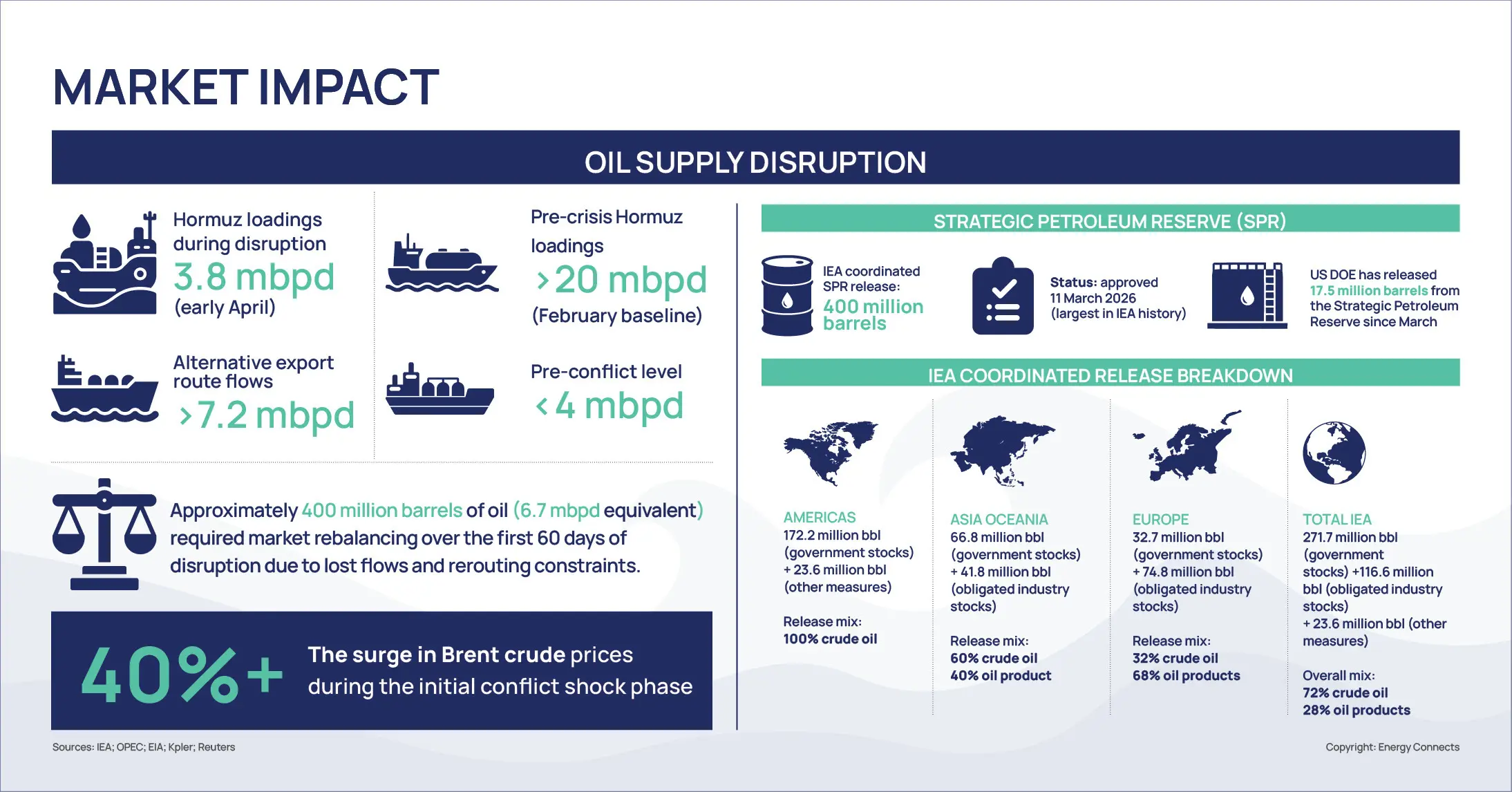

Despite the scale of the shock, the system has largely stabilised through a combination of rerouting (approximately 6 mbpd of bypass capacity), strategic stock releases, and demand adjustment, offsetting much of the estimated 6.7 mbpd of disrupted flows. However, 65–70% of Hormuz-dependent volumes remain non-divertible in the short term, which underscores persistent structural vulnerability.

30-50%

The average increase in voyage distances on key rerouted Gulf export routes

Market dynamics have been driven by expectations rather than actual shortages. Brent crude experienced sharp price swings, including increases of over 40% during the initial phase, while European gas benchmarks, particularly Dutch TTF, rose by approximately 15-25% in the initial shock phase, driven by LNG rerouting toward Asia, before stabilising. At the same time, freight rates and insurance premiums surged, reinforcing logistics as a key constraint.

The shock has propagated beyond energy into the wider economy, with uneven impacts across petrochemicals, fertilisers, aviation, and manufacturing. Overall, the crisis is accelerating a structural shift from efficiency-led optimisation toward resilience-led system design. Energy security is increasingly defined not by access alone, but by the ability to manage disruption across molecules, electrons, and data in real time.

The Hormuz factor: the systemic fault line

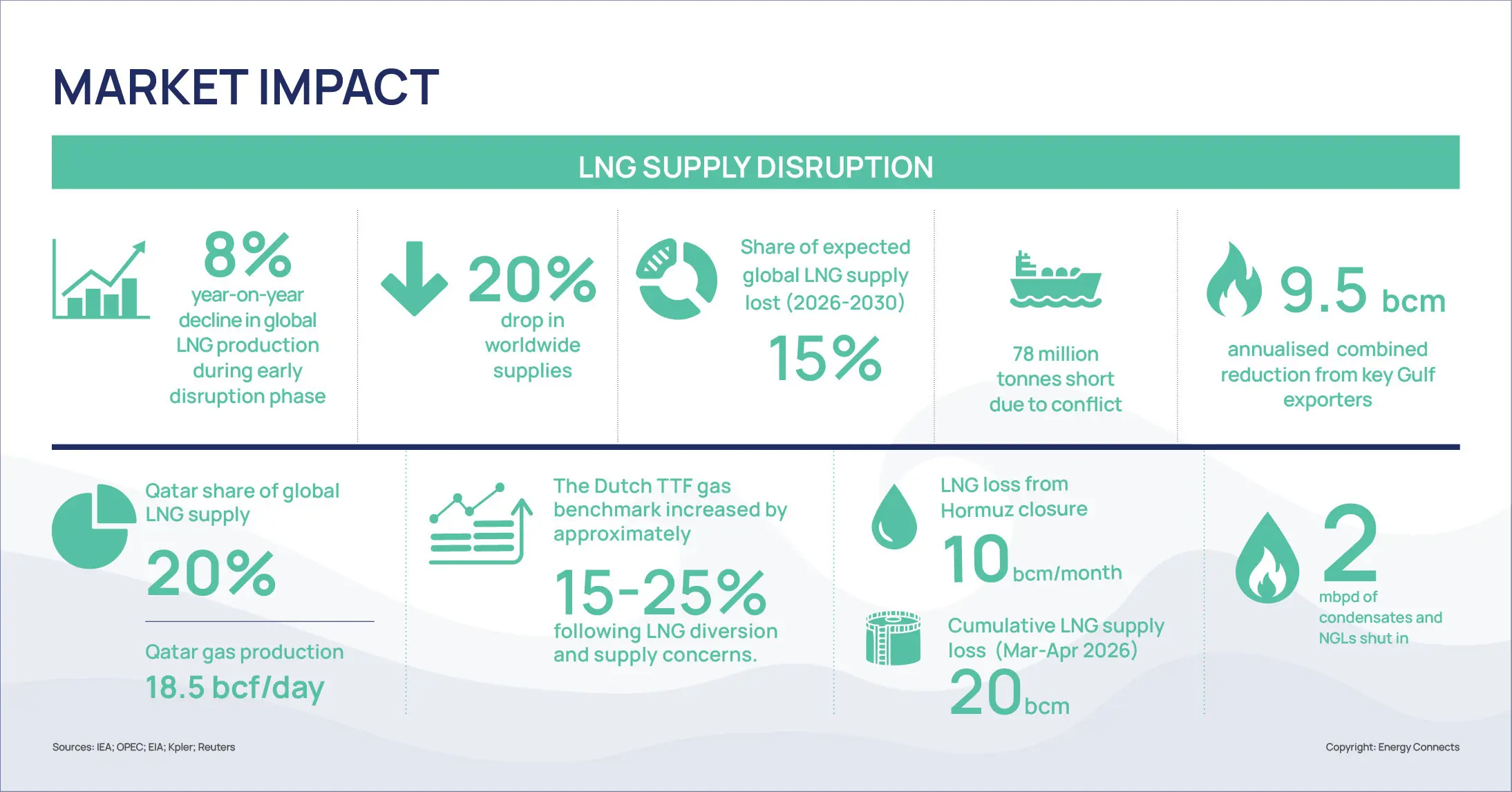

The Strait of Hormuz remains the single most critical chokepoint in the global energy system. Approximately 20 mbpd of crude oil, condensates, and petroleum products transit the Strait daily, representing close to one-fifth of global oil consumption, alongside roughly 20% of global LNG trade.

This creates extreme concentration risk: a single maritime corridor, less than 40km wide at its narrowest navigable point, effectively functions as a global macroeconomic lever. Its partial disruption immediately propagated across Asian and European markets, with Asian LNG importers in Japan, South Korea, China, and India experiencing spot market tightening, while European gas markets reacted through upward pressure on Dutch TTF pricing.

The impact extended beyond hydrocarbons. Delays and rerouting affected petrochemical feedstocks, fertilisers, food supply chains, and critical mineral logistics. Rising ammonia and fertiliser costs increased agricultural inflation risks, while petrochemical volatility disrupted plastics, industrial materials, and manufacturing inputs globally.

The Strait’s closure demonstrated that maritime chokepoints are no longer transport corridors only, but strategic nodes through which energy, food, industrial production, and inflation shocks are transmitted simultaneously.

Market volatility and pricing the war premium

As the crisis deepened, Brent crude markets rapidly embedded a geopolitical war premium, with sharp price swings, including increases of over 40% during the initial phase. Price formation reflected uncertainty over the magnitude and duration of the disruption and its impact on transport reliability, rather than over immediate production shortages. Historical precedent reinforces this dynamic.

During the 2019 attacks on Saudi Arabia’s Abqaiq facilities, a disruption of approximately 5.7 mbpd triggered a 15-20% surge in Brent crude prices, one of the largest single-day increases in decades, showing the non-linear sensitivity of oil markets to perceived supply risk. In 2026, Brent pricing similarly reacted to three overlapping uncertainties: the magnitude of supply disruptions, route uncertainty, and conflict duration.

European gas markets, particularly Dutch TTF, recorded forward pricing increases of approximately 15-25% in the initial shock phase, driven by anticipated LNG diversion away from Europe toward Asian demand centres. Even in the absence of immediate shortages, TTF pricing reflected tightening marginal LNG availability and increased competition for Atlantic basic cargoes.

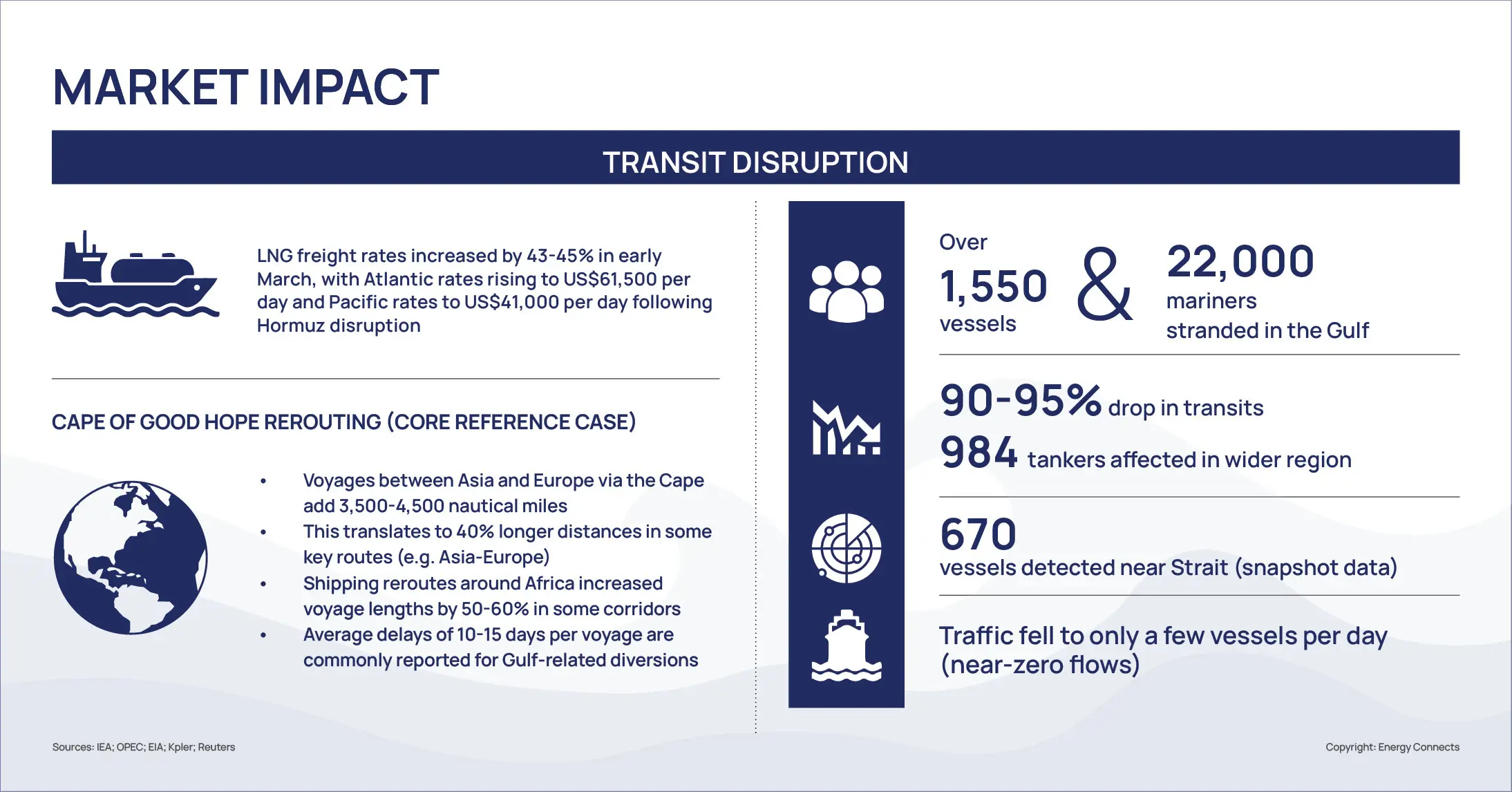

Freight markets reinforced this effect, with LNG shipping rates rising significantly and crude tanker spot rates increasing materially, reflecting reduced effective fleet capacity due to longer voyage cycles and rerouting constraints.

This illustrates a defining characteristic of modern energy markets: expectations move faster than molecules. In tightly interconnected systems, anticipated scarcity is priced before physical shortages materialise.

Pipeline bypass and logistical agility of the Gulf

Despite severe disruption, global supply systems remained operational due to the Gulf’s redundancy infrastructure. Saudi Arabia’s East-West Pipeline (approximately 5 mbpd capacity, with technical capacity up to 7 mbpd) enabled partial Gulf-to-Red Sea rerouting, while the UAE Abu Dhabi- Fujairah pipeline added approximately 1.5 mbpd of export capacity outside Hormuz.

Together, this provides approximately 6 mbpd of bypass capacity under stress conditions, which arguably marked the first major live test of Gulf bypass infrastructure at scale under real crisis conditions.

However, even at full utilisation, 65-70% of Hormuz-dependent flows remain structurally constrained, reinforcing the persistent vulnerability to single-node disruption in global energy logistics.

Supply chain fragmentation: the force majeure era

Disruptions from the Strait of Hormuz closure rapidly cascaded far beyond energy markets into global industrial supply chains, triggering widespread force majeure declarations across energy, petrochemicals, LNG shipping, and downstream manufacturing. Kpler vessel tracking and industry reports indicate that the disruption led to widespread congestion across LNG and tanker flows, with significant cargo delays and vessel backlogs forming within the Gulf and at key downstream hubs such as Fujairah, Singapore, and Rotterdam. These delays reflected not only rerouting but also systemic congestion across tanker fleets, port operations, and extended voyage cycles.

Petrochemical markets experienced immediate feedstock volatility, with prices increasing by up to 40% due to inventory tightening and delivery uncertainty. Global fertiliser markets rose in parallel by 15-30% in the initial disruption phase, driven by ammonia and gas feedstock constraints, with sharper spikes in urea during peak stress periods, reinforcing downstream agricultural inflation pressures.

A particularly sensitive transmission channel emerged in aviation. Jet fuel prices more than doubled, reflecting refinery rebalancing between diesel and jet production and tighter Gulf-linked supply logistics. Airlines faced dual pressure from higher fuel costs and operational inefficiencies caused by rerouted flight paths and constrained refuelling hubs. Given aviation’s limited storage capacity and just-in-time fuel procurement model, cost increases were rapidly transmitted into operating costs, increasing the cost per available seat kilometre (CASK), particularly for long-haul carriers dependent on Gulf and Asian hubs.

15-30%

The rise in global fertiliser markets during the initial disruption phase

Manufacturing sectors exposed to energy-intensive inputs saw mid-single- to low-double-digit increases in input costs, depending on energy intensity and supply chain exposure. Disruptions to delivery schedules and feedstock availability further amplified inefficiencies in industrial production cycles across chemicals, metals, and industrial materials.

Overall, the force majeure environment evolved into a multi-sector transmission shock, in which energy disruption propagated simultaneously across petrochemicals, agriculture, aviation, and manufacturing, with stranded cargoes serving as a physical indicator of global supply chain desynchronisation.

The strategic pivot: building resilience

The Middle East conflict has reinforced a structural lesson: systems optimised for efficiency under stable conditions are not inherently resilient under stress. As a result, a strategic pivot toward resilience is underway as a core organising principle of global energy systems.

This is increasingly expressed through geopatriation, as governments and companies seek greater strategic control over energy, technology and industrial assets. This is driving localisation of supply chains and expansion of domestic industrial capacity in critical sectors. Energy infrastructure itself is evolving away from rigid centralised models toward more adaptive architectures, including districted energy systems, battery storage, flexible load management, and AI-managed microgrids that reduce reliance on single points of failure and improve overall system responsiveness under disruption.

These adjustments reflect a system shifting from supply adequacy to transport and insurance scarcity

These adjustments reflect a system shifting from supply adequacy to transport and insurance scarcity

Beyond distributed systems, AI has also emerged as an operational resilience tool in constrained infrastructure during routine operations. In hydrocarbon systems, ADNOC’s AI-enabled platforms (ENERGYai and Neuron 5) integrate predictive maintenance, upstream optimisation, production forecasting, and digital twins to reduce unplanned shutdowns, improve asset utilisation, and strengthen operational reliability under routine stress. ADNOC reports that these tools have halved unplanned shutdowns and cut planned maintenance by approximately 20%, illustrating how digital intelligence can improve efficiency and system reliability under normal operating conditions. While there is no evidence that these systems directly mitigated the Strait of Hormuz crisis, their predictive and optimisation capabilities could help preserve operational continuity during disruptions.

Global grid investment is projected to exceed US$600 billion annually by 2030 as countries modernise energy systems to accommodate electrification, digitalisation, and growing resilience requirements.

More fundamentally, the system is moving from reactive crisis management toward proactive system design. Energy security is increasingly defined by the ability to respond dynamically to physical and digital disruptions across interconnected infrastructure, market and information systems.

The 2026 conflict, therefore, has not simply exposed vulnerabilities within the global energy system but accelerated its redesign. Energy security is no longer defined solely by access to resources, but by the capacity to manage disruption across molecules, electrons, and data.

- This Market Outlook report was produced as a part of ADIPEC’s Energy & Geopolitics series. For more information and coverage, visit: https://www.adipec.com/press-media/insights/