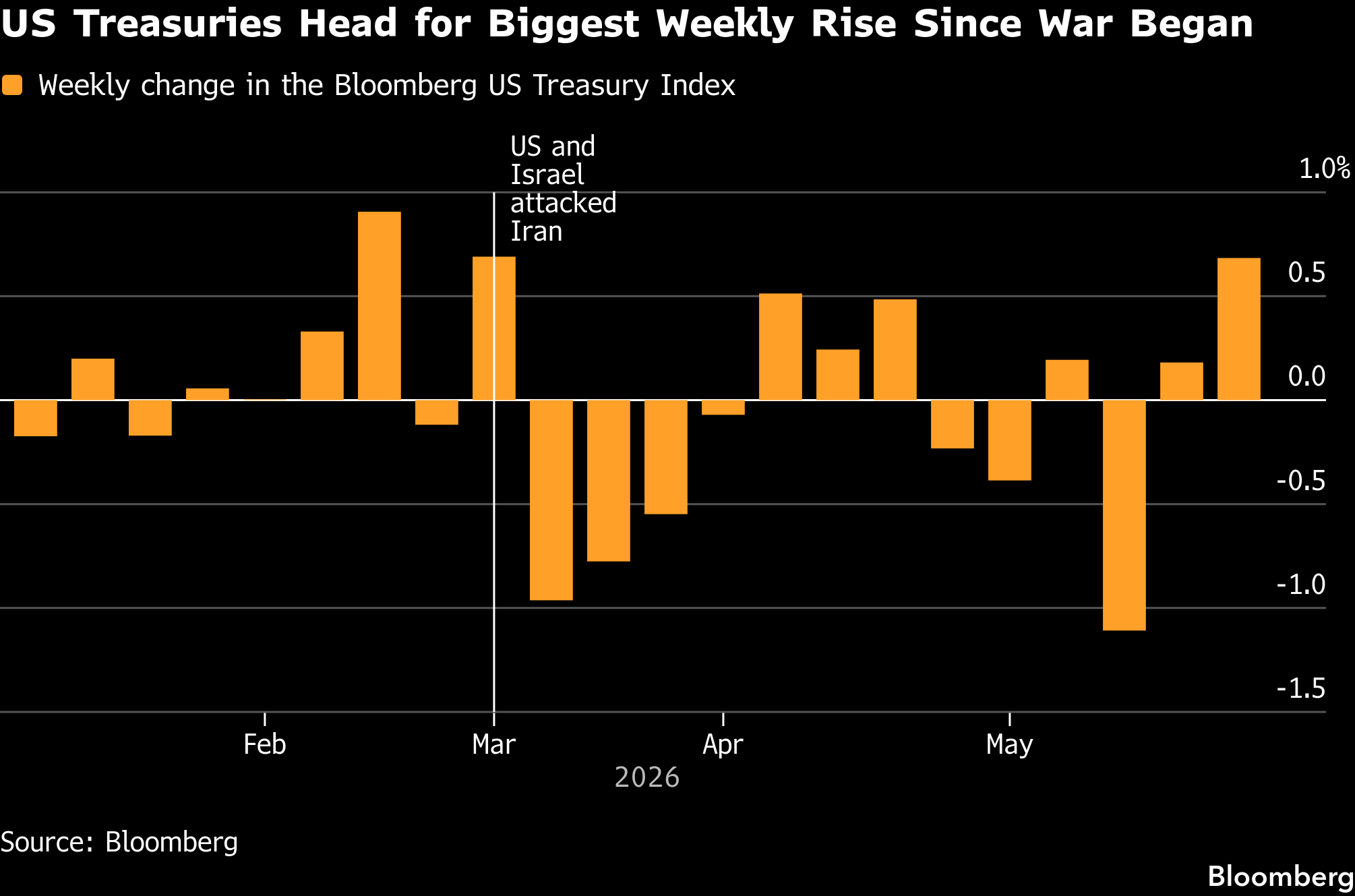

Treasuries Set for Best Week Since War Began as Oil Retreats

(Bloomberg) -- The US government bond market headed for its best week since the start of the war on Iran as oil prices declined in anticipation of an agreement to end the conflict.

The Treasury market rally trimmed yields across maturities by nine to 12 basis points since last Friday’s close, pointing to its best weekly performance since Feb. 27, the day before the war started. Two- to 10-year yields declined to weekly lows Friday after US President Donald Trump said a meeting “to make a final determination” on Iran was under way.

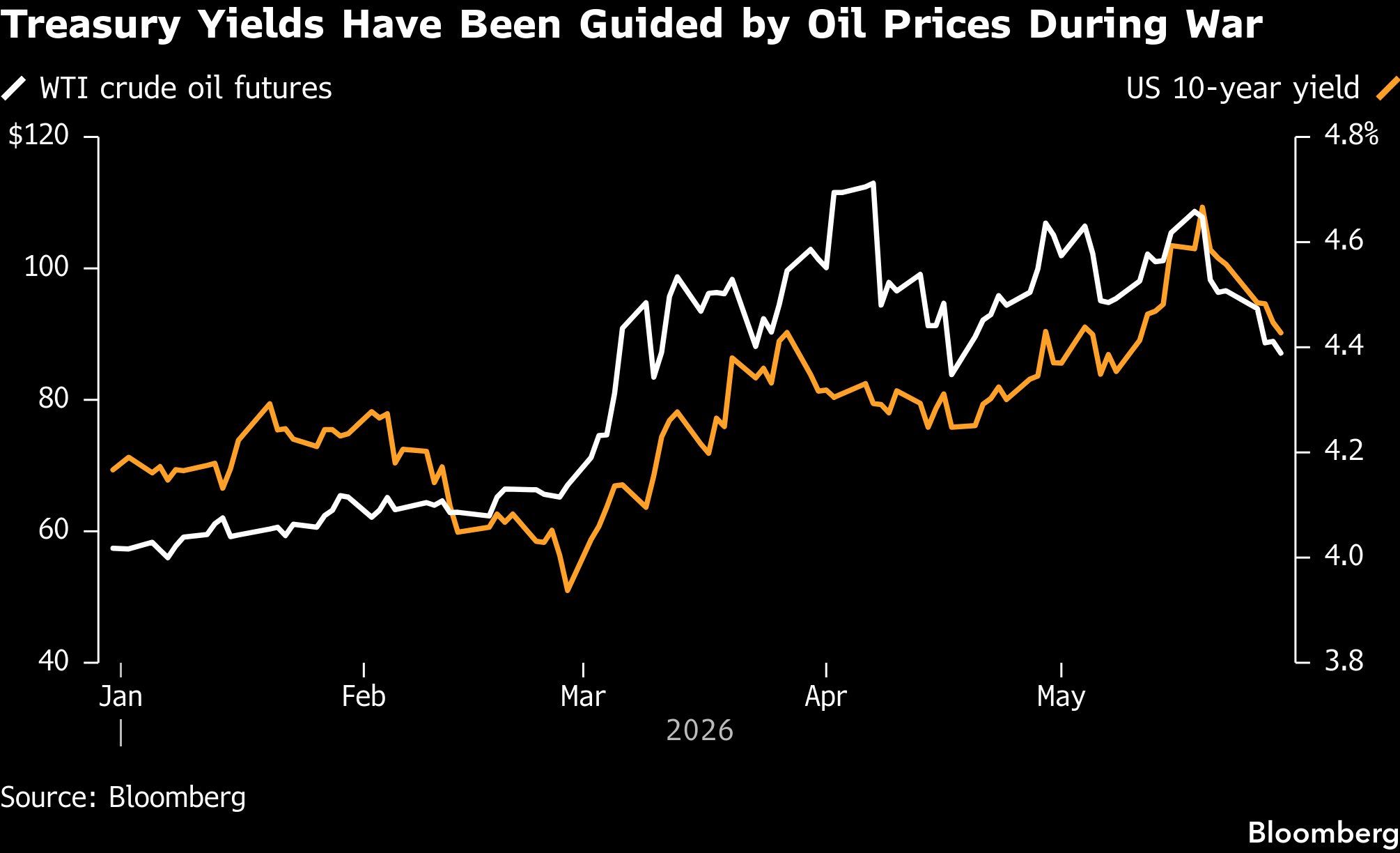

Earlier in the session, the 30-year yield touched 4.96%, the lowest level since May 11.

“It’s pretty evident they’re going to get a deal done sometime in the next week or so,” Raghav Datla, an interest-rate strategist at Citigroup Global Markets, said. “That builds confidence that you might not see a second-order impact from these oil prices into core inflation.”

The weekly moves represent a turnaround from earlier this month, when global bonds tumbled on concern about the war’s impact on the world’s economy. The moves were driven in large measure by elevated oil prices because of a war-related supply shock. Traders, who before March were pricing in two Federal Reserve interest-rate cuts this year, wagered on an increase by mid-2027.

Less than two weeks ago, the US government’s longest bond yield had reached almost 5.20%, the highest level since 2007. Shorter-maturity Treasury yields reached their highest levels since early 2025 earlier this month.

Over the past week, however, tentative indications that the US and Iran are nearing an agreement that would restore Middle East supply sent benchmark oil prices to the lowest level in six weeks, and Treasury yields retreated.

Residual Risk

“There’s still some residual rate-hike pricing risk, but once a deal is finalized, most of that will be priced out,” Datla said, referring to the roughly 15 basis points of Fed tightening priced into swap contracts linked to the Fed’s policy rate at the end of the year.

While the market will have difficulty resuming pricing in rate cuts for this year, it has scope to wager on them during the next two years, he said. That’s based not only on oil prices, but also on actual inflation data including the price indexes for personal consumption expenditures released earlier this week for April.

While the 3.8% year-on-year increase in PCE prices was the highest since 2023 and has exceeded the Fed’s 2% target since 2021, the monthly increases were smaller than economists estimated.

This week’s gains for Treasuries also have technical underpinnings. Friday was the last day of the month, in which $324 billion of notes and bonds were sold. Those will join the Bloomberg Treasury Index at 4 p.m. New York time, and index funds and other passive investors conventionally buy them on or around that time in order to match the performance of the index.

Month-end index additions are larger in February, May, August and November, when Treasury auctions are biggest. About $240 billion of notes and bonds were added to the index at the end of March and April.

Index Rebalancing

The index rebalancing isn’t guaranteed to drive buying, however, as passive funds may already have met their needs to some extent. This week’s Treasury auctions of two-, five- and seven-year notes drew good demand as measured by the proximity of their yields to indicated levels. By contrast, auctions of those tenors in March and April drew higher-than-anticipated yields, a sign demand fell short of expectations.

The weekly advance may fully offset the market’s losses through the end of last week, leaving it close to flat on the month.

Higher Treasury yields and anticipation of Fed interest-rate increases also are unfolding amid a pattern of upside surprises by US economic activity gauges and record highs for US stocks — including on Friday, suggesting it may take more than lower oil prices to sustain the bond market rally.

“The US economy remains broadly resilient and supply side price pressures are still working through the inflation data,” Monty Gandhi, an interest-rate strategist at SMBC Group, said in a report. “As a result, we think it will be difficult for a sustained rally in yields without either a concrete geopolitical resolution or signs of labor market deterioration.”

The US Labor Department is slated to release May data on June 5. Economists estimate it will show a slowdown in job creation, to 85,000 new nonfarm jobs from 115,000 in April.

(Adds additional comments and updates yield levels.)

©2026 Bloomberg L.P.