Oil Hits Four-Year Low as Trump Tariffs Stoke Recession Fears

(Bloomberg) -- Oil tumbled to a four-year low as markets remained on edge about the next steps for President Donald Trump’s global tariff plans.

West Texas Intermediate futures swung in a roughly $5 range before settling near $61 a barrel. Futures had briefly surged earlier on speculation about a pause in some tariffs, which the White House later denied. WTI has slid about 16% in the past three sessions.

Crude has plunged as Trump’s tariffs imperil global energy demand and a surprise output hike from Saudi-led OPEC+ raises the prospect of swelling supplies. Trump signaled on Monday that he’s willing to press his trade war even further, threatening an additional 50% tariff on major oil importer China.

The levies “came in above even the most hawkish of expectations, driving markets, notably growth-sensitive commodities, to more meaningfully price in a US and possibly global recession,” JPMorgan Chase & Co. analysts including Tracey Allen and Natasha Kaneva said in a note to clients.

The pullback is threatening the coffers of oil-producing nations that need far higher prices to meet their budgets. Over the weekend, Saudi Arabia slashed the price of its key Arab Light crude to Asia — the top market — by the most since 2022.

At the same time, crude’s drop may take some of the sting out of inflationary pressures from Trump’s tariffs on trade partners, which are leading some market participants to boost expectations for Federal Reserve rate cuts. Industries from trucking to airlines are likely to benefit from lower fuel costs, and Trump heralded the decline in oil prices on his Truth Social platform on Monday.

Along with the moves in headline crude prices, there have been shifts across other parts of the oil market.

WTI prices for next year are now trading close to $58 a barrel and shale-oil company shares are down more than 15% since Trump announced his tariff policies. A survey by the Dallas Federal Reserve last month said average prices need to be $65 to profitably drill new wells.

There was also record trading of bearish put options on Brent futures on Friday, another sign that traders are bracing for further declines. Options profiting from price drops are at their biggest premium to those betting on a rally since late 2023.

Banks are turning more gloomy. Goldman Sachs Group Inc. cut its forecasts for the second time in less than a week, while Morgan Stanley reduced its estimates, hot on the heels of other banks last week.

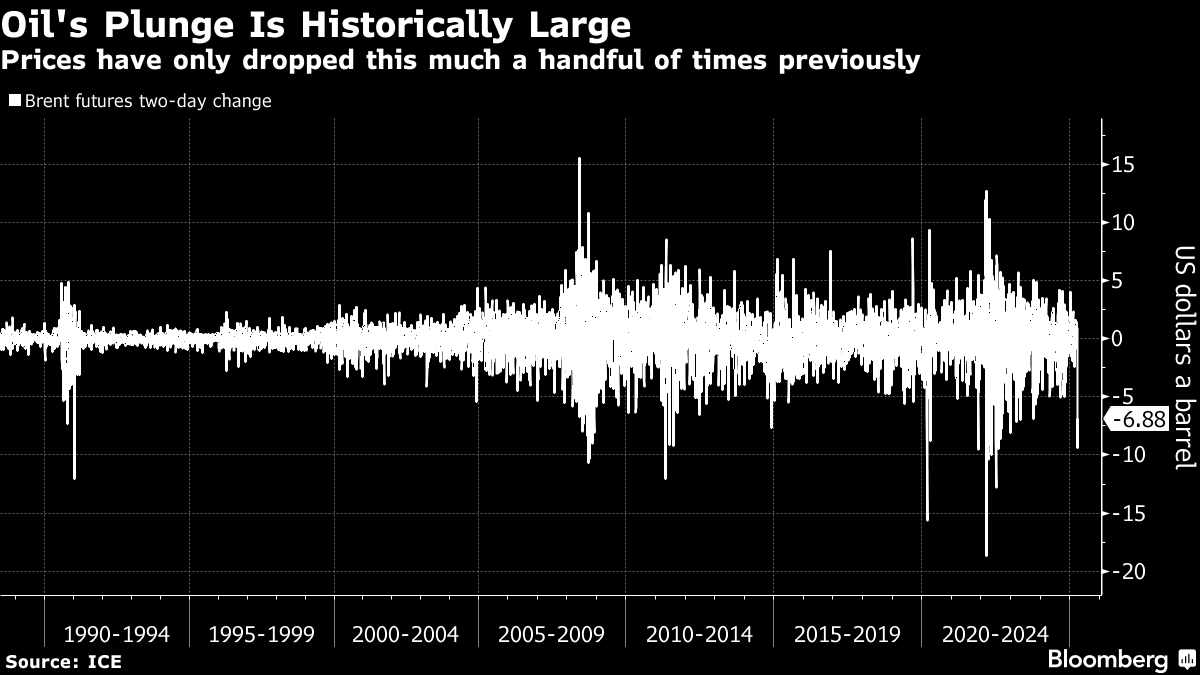

“Such sharp declines are rare,” Morgan Stanley analysts including Martijn Rats and Charlotte Firkins wrote, noting that, in percentage terms, Brent has only fallen this much over two days 24 times since the 1980s. “Of those, 22 are associated with recession.”

©2025 Bloomberg L.P.