Beyond Hormuz: Gulf states explore alternative energy supply corridors

When free-flowing traffic will return through the Strait of Hormuz is currently the energy industry’s most topical question, as the world’s most critical energy corridor remains effectively closed for 52 days and counting. With the impact of closures due to the Iran war felt worldwide, Gulf states and the wider Middle East are examining longer-term alternative routes to avoid the Strait altogether and ensure secure, stable energy supplies.

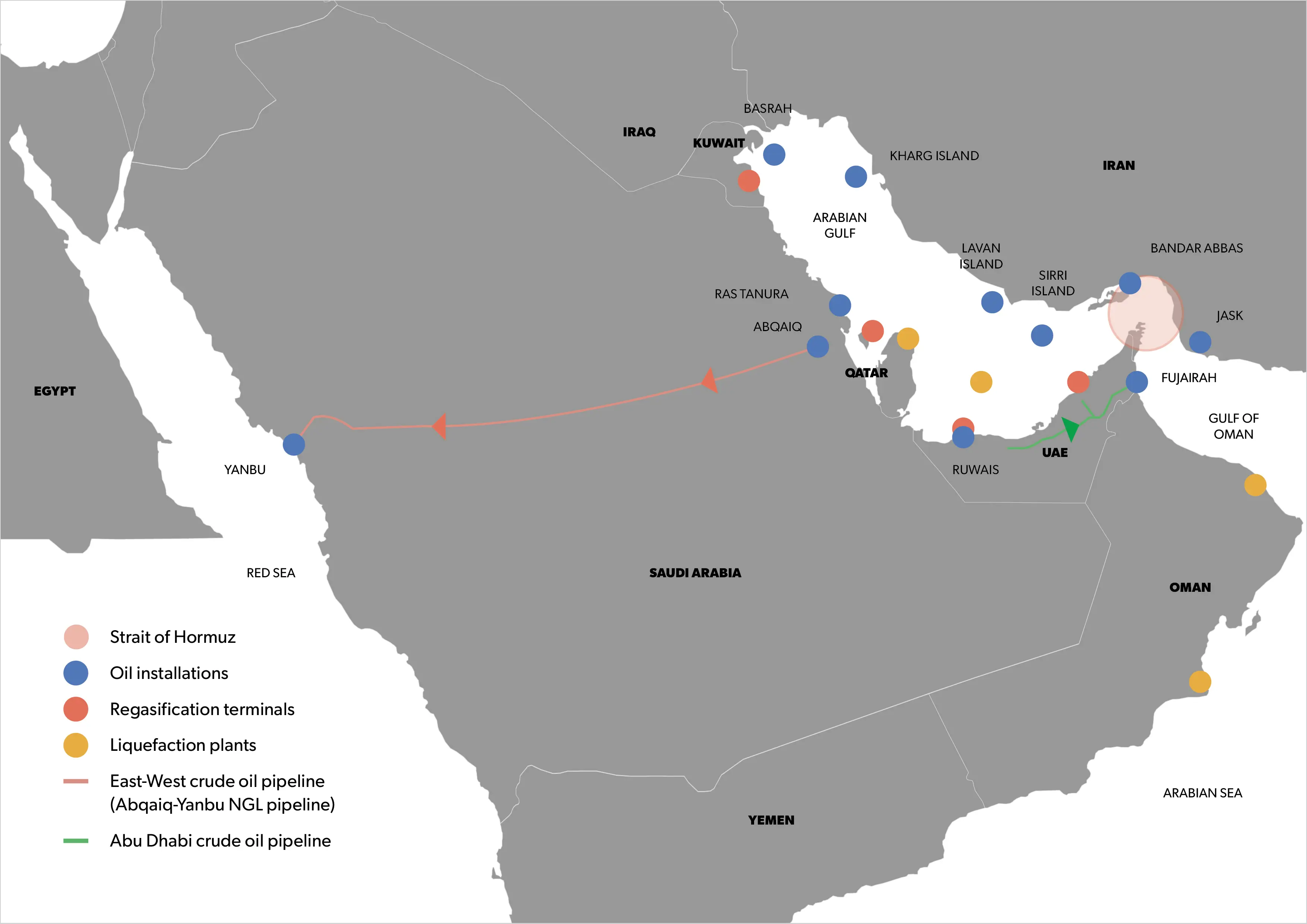

Proven alternatives

The global dependence on this narrow waterway has been laid bare during the Israel/US war with Iran, sending economic pain across continents. With about 20% of global oil supply — some 86 tankers daily — usually passing through Hormuz, existing bypass options have confirmed effectiveness and rewarded investment.

The UAE’s Abu Dhabi Crude Oil Pipeline (ADCOP) by ADNOC proved critical when the Strait closed, allowing movement of up to 1.8 mbpd from onshore Habshan fields to Fujairah port on the Indian Ocean. International Energy Agency (IEA) data shows a parallel natural gas liquids pipeline with a capacity of 300,000 bpd.

Saudi Arabia’s 7 mbpd capacity East-West Petroline — built during the 1980-88 Iran-Iraq war to ease Strait reliance — takes supplies from Abqaiq to the Red Sea coast Yanbu terminal.

The efficacy of each has underlined the need for more shipping methods, not least if Tehran again chokes Strait traffic or introduces tolls.

Energy shocks highlight Hormuz exposure

Iranian missile attacks also made the 1,200km Petroline and Fujairah facilities targets, while Red Sea shipments remain exposed to Yemen’s Houthi rebels.

Kuwait, Bahrain, and Qatar have no alternatives to Hormuz, and the LNG sector, where Qatar and the UAE together represent almost 20% of global exports, is transit-vulnerable.

“There are no alternative export routes other than tankers through the Strait,” said Ross Wyeno, Associate Director, Lead LNG Short-Term Analysis at S&P Global Energy.

All this drives the need for suppliers to shape the future via substitute routes for hydrocarbons from the Gulf.

An average of 20 mbpd of crude and oil products were shipped through the Strait in 2025, along with about 25% of global seaborne oil trade, of which 80% was destined for Asia. Regardless of negotiated outcomes to the conflict, Iran could still wield influence over shipping lanes in the Hormuz.

Options in focus

KSA could potentially rehabilitate its 1.65 mbpd Iraqi Pipeline through Saudi Arabia (IPSA) and Trans-Arabian Pipeline (Tapline).

The former linked Al-Zubair, southern Iraq, to Red Sea port Mu’ajiz, but hasn’t carried Iraqi crude since August 1990.

Tapline could hypothetically channel 500,000 mbpd Saudi crude to the Mediterranean. Built in 1950 from KSA’s Eastern Province to the Zahrani terminal near Sidon, Lebanon, it remains robust despite ceasing operations in 1983. Oil transportation costs via Tapline to Europe could prove up to 40% less than shipping through the Suez Canal.

The IEA has proposed building a new pipeline linking Iraq’s Basra oil fields and Türkiye’s Mediterranean terminal in Ceyhan.

Türkiye has also proposed extending the strategic Kirkuk-Ceyhan pipeline, which began moving crude from northern Iraq in 1976.

Syria is being considered as a potential transit route to the Mediterranean, though this could increase transit times and costs for Asian customers. Kuwait has no meaningful bypass capacity but could revive discussions about linking into Saudi infrastructure.

Türkiye, Syria and Jordan also recently agreed to modernise their railway systems — eventually creating a contiguous corridor between southern Europe and the Gulf — although this would require specific fuel-carrying railcars.

The UAE and Jordan signed an agreement last week to build and operate a $2.3 billion railway linking Jordan’s mining areas to Aqaba port. The 360km project is the first step in building a Jordanian national rail network connecting Aqaba with neighbouring Arab countries, including ports in Syria and the Mediterranean.

Mapping the hurdles

New or rehabilitated cross-border arteries could be costly, politically and geographically complicated, and take years to complete.

However, energy suppliers and consumers now fully recognise the Strait’s fragility — and the price of disrupting vital supplies.

Christopher Bush, CEO of Lebanon-based Cat Group, cited a $5 billion cost to replicate Saudi Arabia’s pipeline today. He said more complex routes from Iraq through Jordan, Syria, or Türkiye could top $15-$20 billion, besides potential security risks, operation and ownership disputes, or terrain challenges.

But, Bush added, “You have a lot of smart minds looking at all of this now.”

Beyond Capex, market realities could limit the viability of many options, not least as Middle Eastern crude flows mostly to Asia rather than Europe.

That could flip policymakers toward growing existing infrastructure: gradual expansion, such as increasing pipeline capacity or storage, could prove more achievable in enhancing resilience.

The Financial Times said KSA is considering expanding capacity or developing additional export routes and Red Sea terminals, including NEOM-linked projects.

Possible long-term options could embrace broader trade corridors stretching from India through the Gulf to Europe.

And the UAE already reportedly has new pipeline capacity under development. According to Robin Mills, CEO of Qamar Energy and Energy Connects columnist, ADNOC planned to build another 1.5 mbpd pipeline to connect offshore fields to Fujairah.

As economists assess the fiscal impact of the Strait’s weaponisation, the energy industry is appreciating the risk-reward calculus of investing in alternative channels.

ADCOP was reported to have cost $4.2 billion after completion in 2012. “Under current wartime oil pricing, the invaluable exports it carries would pay within a month,” added Mills.