Peak LNG Looms In Europe With Investors Wary Of New Projects

(Bloomberg) --

Utilities in Europe are to find alternative uses for liquefied natural gas projects in a sign that demand for newbillion euro import terminals has peaked.

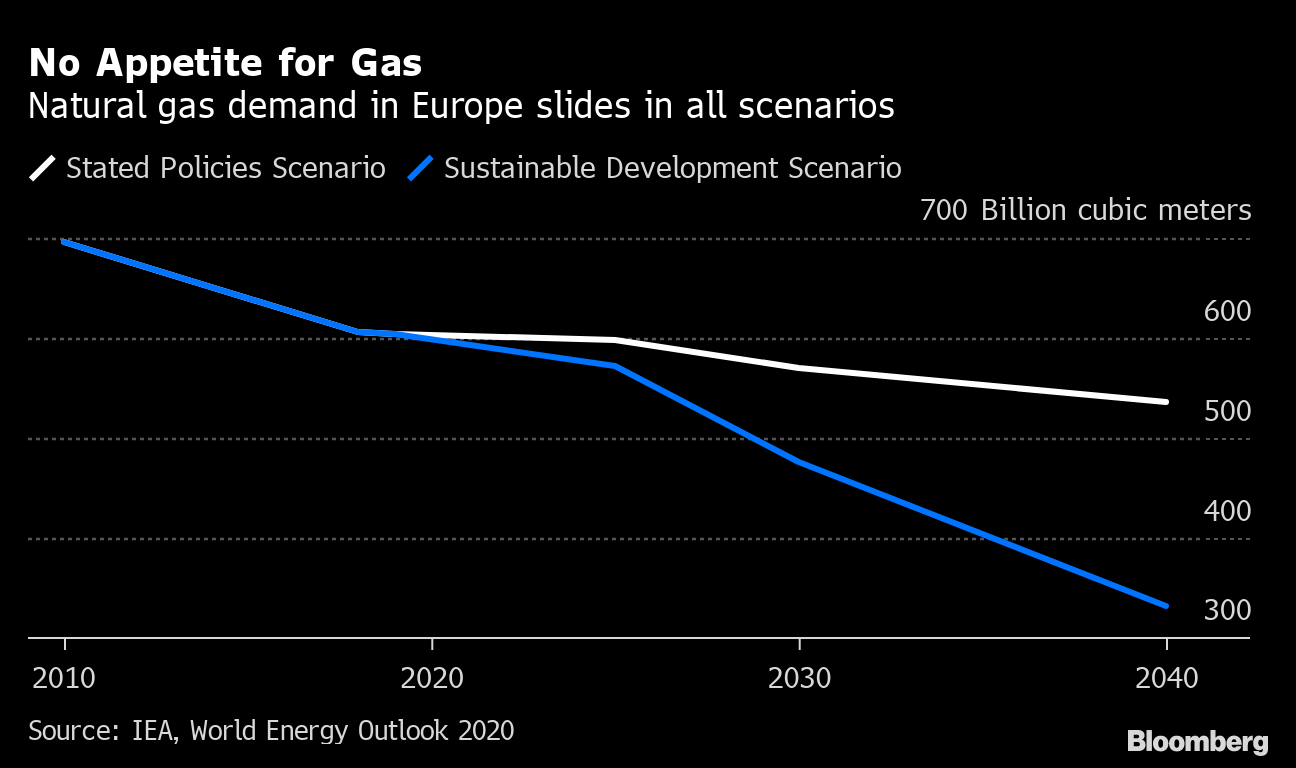

The viability of new LNG projects has never been more uncertain with European gas use expected to wane over the next two decades as ever-cheaper, greener energy sources take hold. The demand outlook means the payback period for gas assets such as LNG terminals is shrinking, according to Accenture Strategy.

Germany’s Uniper SE is the latest to acknowledge waning investor appetite for new LNG capacity when it decided last month to turn a planned terminal into a hydrogen hub. It follows a similar project in Ireland that was redesigned to produce green hydrogen using power from an offshore wind park. RWE AG is exploring ways to handle imported hydrogen at a planned LNG facility in Germany.

“Most European utilities don’t want to touch gas-related projects with a barge pole as companies seek to improve their ESG metrics, improve valuation and avoid stranded asset risks,” said Elchin Mammadov, an analyst at Bloomberg Intelligence.

Only a couple of years ago, Uniper and U.S. LNG developer NextDecade Corp. bet that new facilities to import LNG into Europe would look attractive to diversify fuel supplies amid abundant global production.

The risk LNG developers face now is that billions is invested in new gas infrastructure that becomes unsaleable, or stranded, assets. Terminals under construction in Europe total 2.6 billion euros ($3.1 billion), and those in pre-construction would add another 13 billion euros, according to a survey by Global Energy Monitor.

“Companies that remain excluded from the green bubble become less attractive,” said Nicolas Bouthors, an equity analyst at Alphavalue SAS in Paris, which is excluding fossil-fuel assets from its valuation of some energy companies. “It is ever more difficult to raise equity and green bonds are not a solution for such projects, which means energy companies have lost two important ways to finance LNG terminals.”

Concerns about the long-term future of gas are making companies take steps “in the right direction for hydrogen,” said Deepa Venkateswaran, managing director at Bernstein Autonomous LLP. Still, hydrogen is unlikely to make a significant difference in the short term because the economics remain unknown, she said.

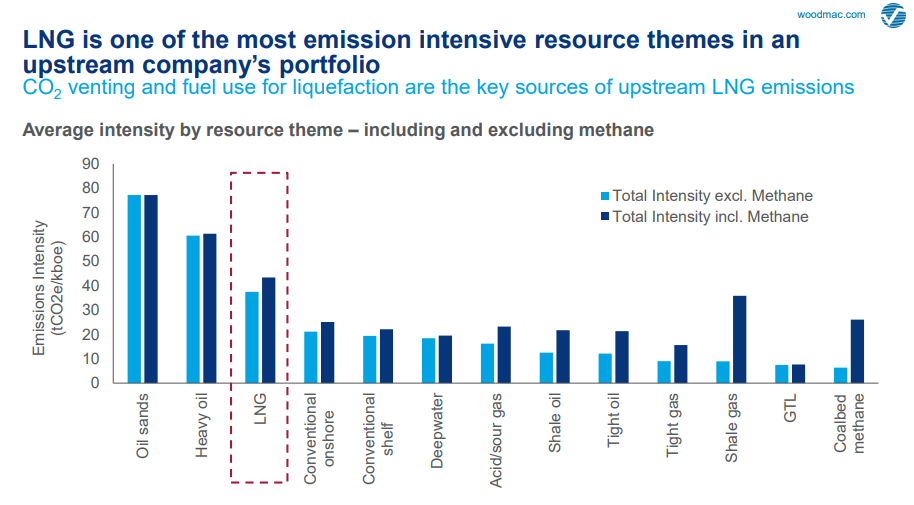

Source: Wood Mackenzie Ltd.

With hydrogen technology still in its infancy and facing headwinds in its cost and complexity, not all LNG terminal projects in Europe are likely to be scrapped. As global trading of the fuel develops and Asian demand is set to boom for another two decades, LNG still plays a key role in Europe’s energy mix.

Uniper is still active in northwest European and Spanish LNG regasification capacity and “we don’t see that changing any time soon,” Peter Abdo, the company’s chief commercial officer for LNG, said in an interview.

For RWE, adding the ability to import hydrogen at its proposed terminal in Germany is a natural evolution from its LNG trading experience, according to Andree Stracke, chief executive officer of the utility’s trading unit.

The role of gas as a transition fuel will be “increasingly scrutinized” said David Rabley, a managing director at Accenture Strategy. Any decision not to invest in gas or LNG will be tied to demand trends, he said.

(Updates with analyst comment in seventh paragraph.)

For more articles like this, please visit us at bloomberg.com

©2021 Bloomberg L.P.