Aramco Investors Miss Out on Oil Stock Rally After Output Cuts

(Bloomberg) -- In a year when shares of some major oil producers have hit records, Saudi Aramco’s stock has gone the other way.

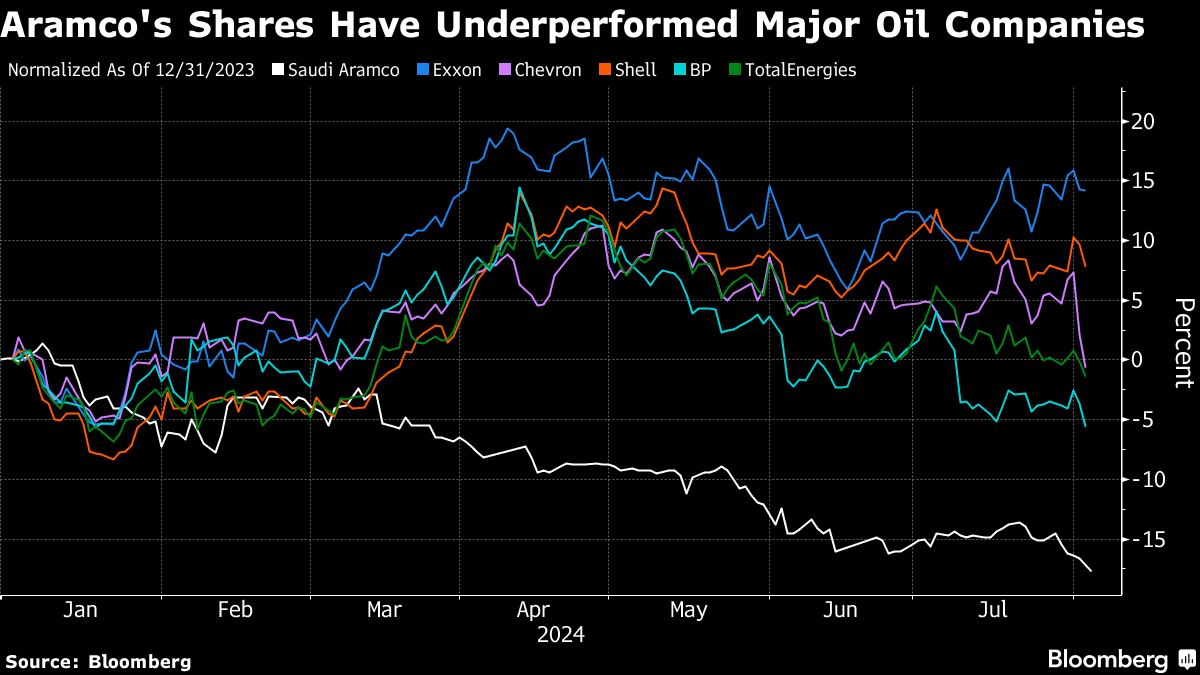

Aramco is down in 2024, the worst performance among the world’s 10 biggest oil companies by revenue, as the company has cut production at the behest of its government owner. The stock on Sunday dropped below the price of this year’s secondary share sale. PetroChina Co., by contrast, is up in Hong Kong, while Exxon Mobil Corp. has gained and Shell Plc is higher.

Of course, Aramco is unlike those other oil firms. The Saudi government and its investment fund own a combined 97% of the company, and the kingdom relies heavily on the business for its funding needs as Crown Prince Mohammed Bin Salman pushes ahead with his economic transformation plan. There may be additional pressure following a global stocks selloff on Monday over concerns the Federal Reserve is behind the curve with policy support for a slowing US economy.

The government oversight on Aramco, along with the war in Gaza and mounting regional tensions, has weighed on the stock even as crude prices have risen this year: Aramco has curbed production as part of OPEC+ policy, and the state raised more than $12 billion in June by selling shares in the company. The company also pays a fat dividend, equal to almost 7% of the share price, most of which goes to the state.

“Aramco will be one of the last standing oil producers after a long transition to renewables and its dividend yield is significantly higher than oil major peers,” said Hasnain Malik, head of equity strategy research at Tellimer in Dubai. “But, near-term, its growth is hamstrung by Saudi shouldering the burden of OPEC+ output restraint whereas the majors are under no such constraint.”

Aramco is under pressure to maintain the dividend because the Saudi government needs the funds more than ever. The economy shrank for a fourth straight quarter and officials say the kingdom’s budget will be in deficit for at least several years. MBS, as the crown prince is known, has set in motion a massive spending plan intended to create jobs and develop entirely new cities and kickstart industries.

Investors are now awaiting second-quarter earnings on Tuesday. Morgan Stanley’s Martijn Rats estimates Aramco’s net income at $27.8 billion, in line with the previous quarter.

“We expect slightly higher oil prices to offset the impact from softer refining margins globally in the period,” the analyst wrote in a note.

Special Payout

Aramco, which has a market value of $1.8 trillion, said last year it would pay an additional, variable dividend tied to the company’s free cash flow. Rats said he sees limited room for the company to continue paying such surplus dividends beyond 2024. The performance-linked payout is likely to make up about $43 billion of Aramco’s $124 billion total payout for this year, according to the company.

“The new variable dividend component marks an important and long-awaited change to the company’s remuneration policy,” Rats said. “But we think this catalyst has now largely played out.”

Aramco shares closed Sunday at riyals, below the secondary offering price of 27.25 riyals. The stock is underperforming the kingdom’s benchmark Tadawul All Share Index, which is down this year. Some of the pressure on the company may ease later this year, since OPEC+ plans to gradually unwind part of its production cuts.

Aramco didn’t respond to a request for comment.

Shares of oil companies such as Shell have done better this year as they focus more on their core businesses, dialing back some of their energy transition plans and boosting shareholder returns.

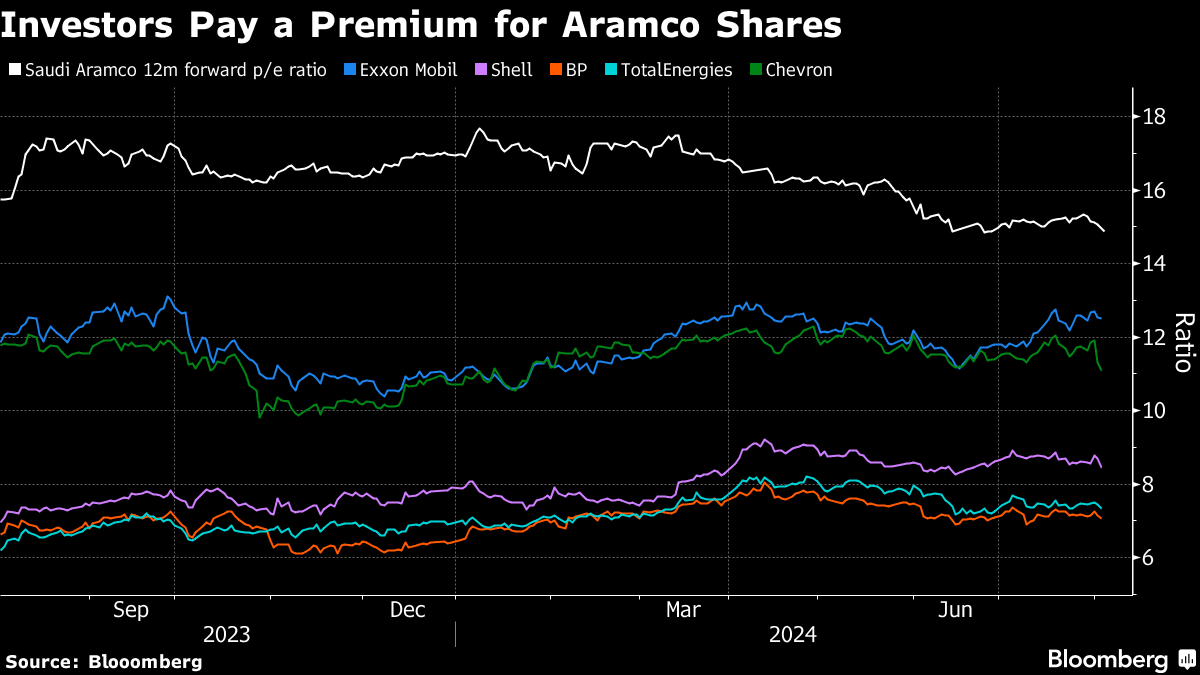

Even after this year’s drop in the stock price, investors still value the Saudi company at 15 times estimated earnings, double the valuation of BP Plc and Shell.

That reflects the sustained, bond-like payments that shareholders can expect from Aramco.

“It’s a stock that’s a quasi-fixed income instrument, and that’s how we hold it,” said Ryan Lemand, chief executive officer of Neovision Wealth Management. “It’s a buy and hold over the long term, and we do believe Aramco will pick up again and that we will continue to hold it.”

©2024 Bloomberg L.P.