BOE’s Mann Says Global Inflation Today is Different from 1970s

(Bloomberg) --The world today is different to the inflation-wracked 1970s and as a result the Federal Reserve remains well placed to respond to evolving price pressures, said Catherine Mann, the newly-appointed Bank of England policy maker who was a former chief economist at Citigroup Inc.

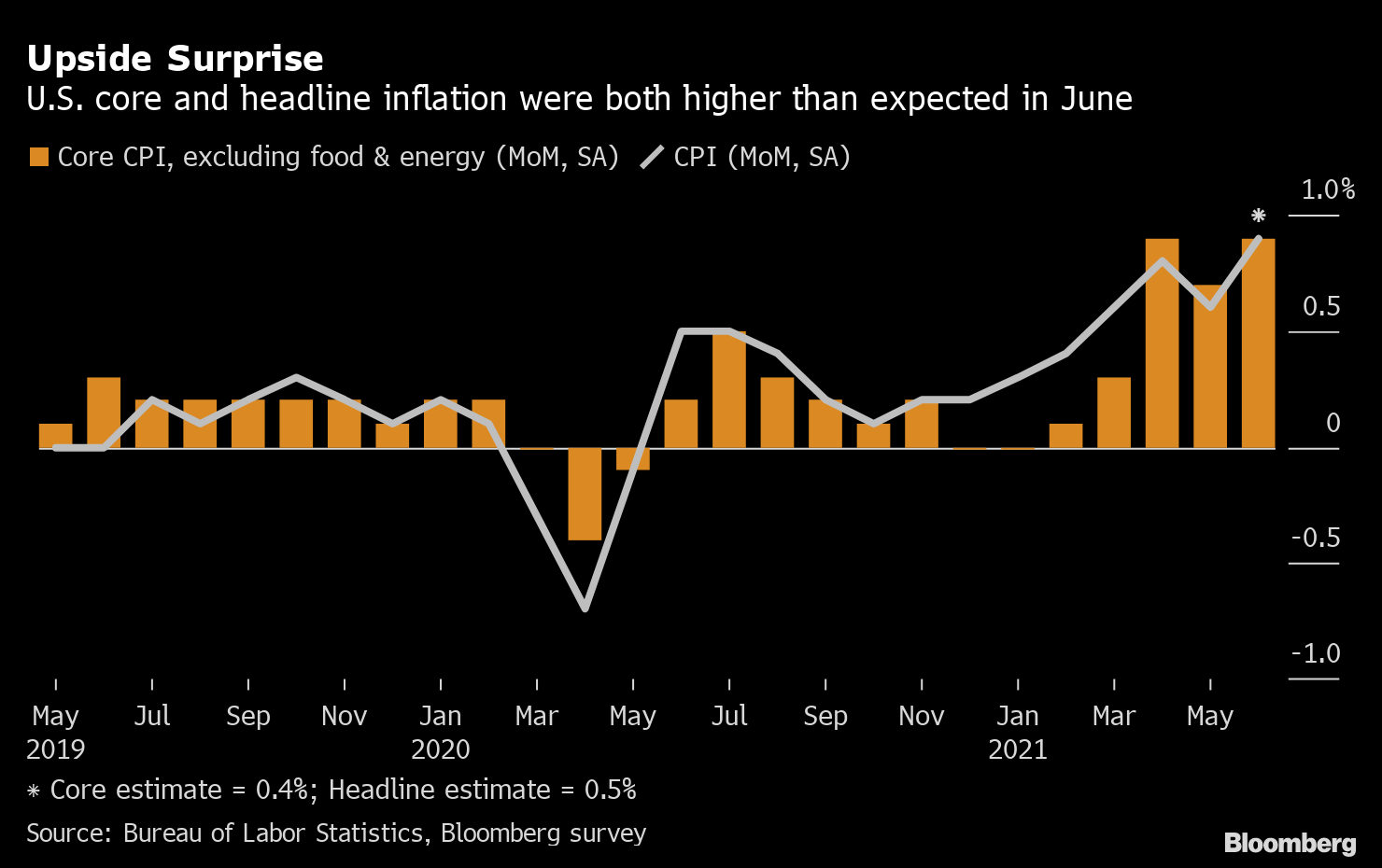

“History is an important guide,” Mann told an Australian National University conference Monday by video, responding to a question on the similarities between the 1970s and today and whether the Fed should respond to the latest 5.4% surge in inflation. “We should always pay attention to historical data. But I think we ought to pay attention to some historical institutional differences as well.”

She set out four factors that distinguished today from the 1970s:

- The extent to which wages and prices were indexed to each other relatively more in the 1970s than now

- The “period of rapid change” in exchange rates and oil prices in the 1970s, and no history of anchored expectations for inflation then;

- The slope of the Phillips Curve, noting back then there was a “much stronger relationship” between wages and labor-market tightness than has been the case over the last 10-15 years; and

- The extent to which firms have pricing power and use that. Firms, she said, remember their inability to make price increases “stick” after the global financial crisis. Now, things are changing a little bit, but companies are reticent about raising prices.

“So I would say the Fed is not behind the curve, and they have the tools in order to address the inflation concerns as they develop,” she said.

Fed Chair Jerome Powell argues that recent increases in inflation reflect disruptions linked to the U.S. economy reopening after the Covid-19 pandemic and are likely to prove transitory.

At the Jackson Hole conference late last month, he sounded a note of caution about employment levels and didn’t provide a specific timeline to start scaling back $120 billion-per-month in bond buying. August’s non-farm payrolls came in weaker than expected on Friday, prompting economists to see a decision to taper this month as off the table.

More stories like this are available on bloomberg.com

©2021 Bloomberg L.P.