Navigating India’s evolving power market: capitalising on the renewable revolution

Feb 02, 2026

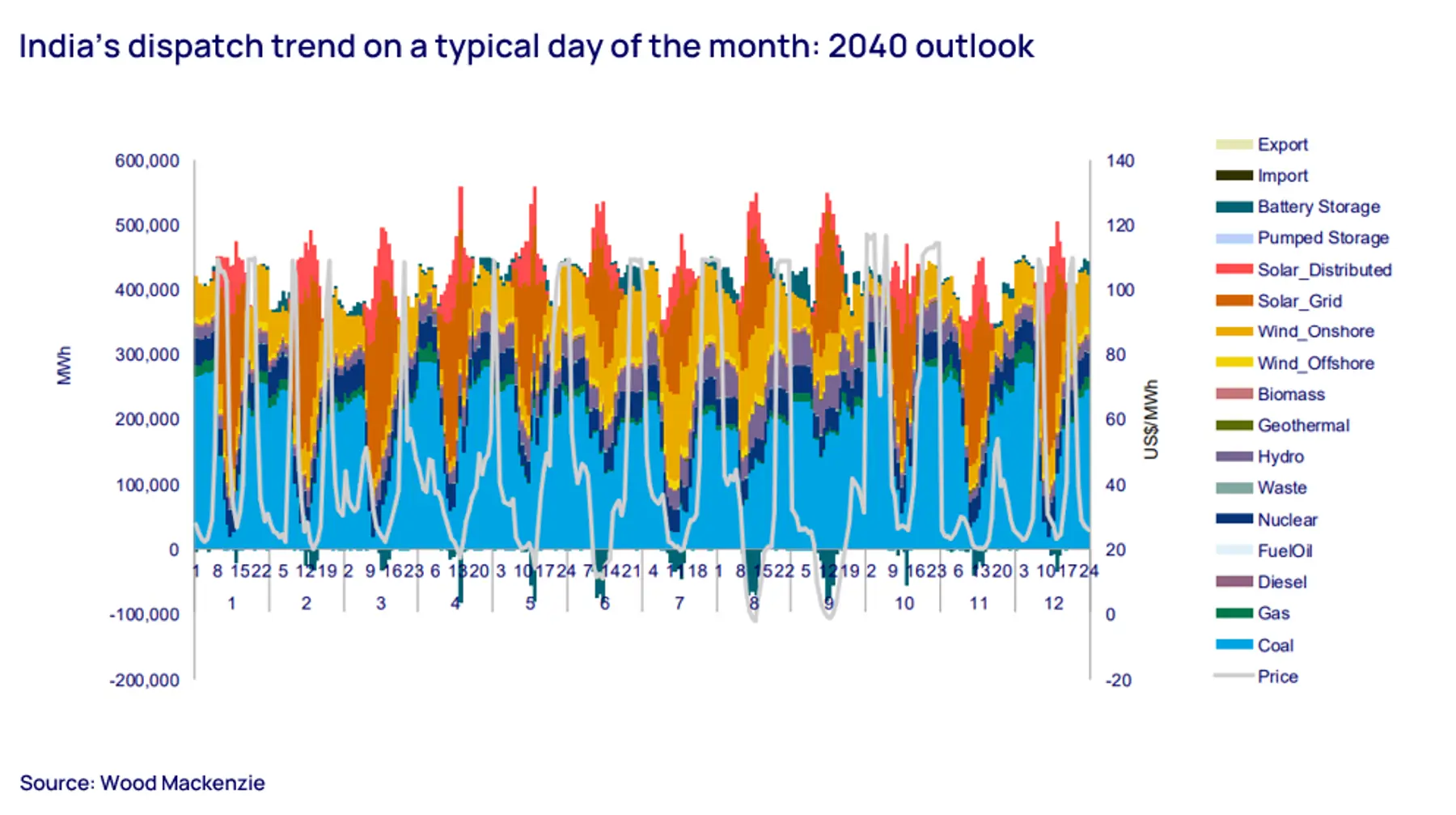

India has big ambitions to transition its energy supply from fossil fuels to renewable energy (RE) by 2030 and beyond. Although coal remains the dominant fuel in the current energy mix, the transition to renewables is evident and being driven by falling costs and climate commitments.

By 2050, renewable energy will account for 57% of India's generation mix - up from 30% in 2030. Wind and solar power combined will contribute 21% of total power generation by 2030 and 51% by 2050. Fill in the form to download the slides from our Navigating India's evolving power market presentation or read on for highlights.

Room for green growth

The acceleration behind the transition is strong government incentives and strategic plans. While the top six players own and operate about 22% of the total installed renewable capacity (including hydro) and about 130 GW of pipeline capacity, there is a shift towards a more competitive, auction-based framework shared between central and state authorities.

Central government tenders accounted for over 52% of renewable auctions in 2024, reflecting a focus on large-scale projects. The government has set up a 50 GW annual bidding plan until 2028 to tender 40 GW of solar, hybrid and round the clock (RTC) projects, along with 10 GW of wind. This structured bidding will give developers long-term financial planning stability and supply chain management.

Considering India's 500 GW renewable target will be met by 84% of wind and solar, there are many opportunities for investors. As the total capacity share of coal and gas falls from 55% in 2023 to 42% in 2030, renewables will increase from 42% to 52% in the same period.

Opportunity in a five-pronged approach

The introduction of policies which improve competition and promote scaling and integration of RE resources underpins a five-pronged systematic approach to India's transition. These five key areas are: cleaning of supply; infrastructure strengthening; efficiency improvements; technology adoption and market liberalisation.

- Cleaning of supply – Mandatory washing of domestic coal travelling more than 500km and mandatory biomass blending in coal plants.

- Infrastructure strengthening – Schemes to improve rural electrification and strengthening of the national smart grid and transmission network from renewable energy zones.

- Efficiency improvements – Ultra-super critical technology will be mandatory in new coal builds and a revamped distribution sector scheme (RDSS) will improve grid efficiency and reduce losses.

- Technology adoption – Policies for adoption of new technology and clean fuels, with production linked incentive (PLI) schemes to boost domestic manufacturing of solar modules, electrolysers, etc.

- Market liberalisation – Market reforms include green open access, uniform renewable energy tariff, carbon markets, the draft Electricity Act to improve retail competition, and a draft policy for market based economic despatch.

Sector focus on growing demand

India is the third largest electricity market globally, but electricity consumption per capita remains low at about 1200 kWh. This is set to almost triple by 2050 as the growing middle class and industries increase wealth and consumption. Around 50% of demand comes from the commercial and industrial segment.

To meet this, government schemes and subsidies support the promotion of RE sources across the value chain:

- Supply chain (manufacturing): PLI scheme for solar equipment manufacturing has a total outlay of US$2.45 billion to boost local solar manufacturing and reduce import dependence, supported by customs duty on imported solar cells and modules and domestic content requirements.

- Generation: Policies provide easier permitting, subsidies to farmers producing solar power, and ultra mega power projects (UMPP) to facilitate quicker build-up of large plants. Central government auctions give developers payment security.

- Storage: India's battery energy storage services (BESS) capacity will reach 2 GW by 2025 - a ten-fold increase from 2024. The national programme on advanced chemistry cell (ACC) battery storage focuses on boosting domestic manufacturing and demand creation.

- Transmission and open access: Green energy corridor (GEC) projects were initiated to evacuate about 40+ GW of RE capacity. Green open access rules promote purchasing of green energy by consumers through a transparent platform for managing transactions.

Energy Connects includes information by a variety of sources, such as contributing experts, external journalists and comments from attendees of our events, which may contain personal opinion of others. All opinions expressed are solely the views of the author(s) and do not necessarily reflect the opinions of Energy Connects, dmg events, its parent company DMGT or any affiliates of the same.