Market outlook: fortifying energy infrastructure and supply chain resilience in a fragmented world

Global energy systems are entering a structurally new phase defined by the primacy of energy security and systemic resilience over cost optimisation. In an increasingly fragmented geopolitical environment, energy infrastructure is being redefined as a strategic asset, with chokepoints, supply chains, and industrial capacity functioning as core determinants of national and regional power.

This shift is driven by the high concentration of global oil and LNG flows through a limited number of maritime corridors, where disruptions can rapidly propagate through pricing, logistics, and supply security. In response, states and producers are pursuing a dual-track strategy: reinforcing hydrocarbon-based systems while simultaneously scaling electrified and digital energy infrastructure.

In an increasingly fragmented geopolitical environment, energy systems are being redesigned around reliability, redundancy and control over critical infrastructure. Infrastructure is therefore no longer viewed as a neutral technical network of pipes, wires, and grids, but as a strategic asset that underpins national security and geopolitical leverage.

In an increasingly fragmented geopolitical environment, energy systems are being redesigned around reliability, redundancy and control over critical infrastructure. Infrastructure is therefore no longer viewed as a neutral technical network of pipes, wires, and grids, but as a strategic asset that underpins national security and geopolitical leverage.

At the same time, the system is becoming more fragmented and multipolar, with growing reliance on regional energy hubs, redundancy mechanisms, and alternative routing infrastructure. Industrial supply chains are also emerging as a parallel layer of vulnerability, characterised by long lead times, supplier concentration, and capacity constraints.

Together, these dynamics point to a transition away from a globally optimised energy system toward a more complex, multi-layered architecture defined by redundancy, optionality, and geopolitical control over infrastructure.

The year of energy realism

Global energy policy has entered an era of energy realism, in which energy security and systemic resilience have overtaken cost optimisation as the dominant decision framework. In an increasingly fragmented geopolitical environment, energy systems are being redesigned around reliability, redundancy and control over critical infrastructure. Infrastructure is therefore no longer viewed as a neutral technical network of pipes, wires, and grids, but as a strategic asset that underpins national security and geopolitical leverage.

76%

Of global oil supply is transported via maritime routes

20%

Of global shipping tonnage is accounted for by tankers

This shift is driving a dual-track system strategy: reinforcing and securing existing hydrocarbon-based energy security while simultaneously scaling investment in electrified and digital energy systems. Global energy investment, which exceeded US$3 trillion in 2025, increasingly prioritises grid reinforcement, domestic production capacity, redundancy, and security of supply. This marks a clear departure from a previous policy era defined by cost minimisation and the optimisation of efficiency gains.

The central policy question is now centred on a new narrative: not what is cheapest, but what remains reliable under disruption.

Infrastructure as geopolitical leverage

A major reason for the new energy realism framing is the fact that energy infrastructure has emerged as a core determinant of global power distribution. Around 76% of global oil supply (~80 million barrels per day) is transported via maritime routes, making a small number of shipping corridors critical to global energy stability. Tankers (used for transporting oil, chemicals, and LNG) account for nearly 20% of global shipping tonnage, which underscores the dependence of the global energy system on constrained maritime infrastructure.

This concentration creates systemic chokepoint vulnerability, where localised disruptions propagate rapidly through global pricing, inventory cycles, and expectation-driven market repricing. Key maritime arteries, such as the Strait of Hormuz, the Bab el-Mandeb, and the Suez Canal, serve as critical pressure points within this system.

407 MPTA

Reached in the global LNG trade in 2024

50%

The percentage that LNG demand is expected to grow by 2040

Empirically, the consequences of disruption are immediate and systemic. During the 2021 Suez Canal blockage, an estimated US$9.6 billion of trade per day was disrupted, including 9% of crude oil and 8% of LNG flows transiting between Asia, Europe, and the Middle East. More recently, the Red Sea crisis reduced Suez-related traffic by around 50% in early disruption phases, forcing widespread rerouting around the Cape of Good Hope and significantly increasing voyage times, freight costs, and insurance premiums, particularly for oil and LNG cargoes.

As a result, infrastructure is no longer a passive conduit of trade, but an active mechanism of geopolitical leverage and risk transmission. Control over, or exposure to, these corridors increasingly shape alliance structures, regional security postures, and pricing power across energy markets.

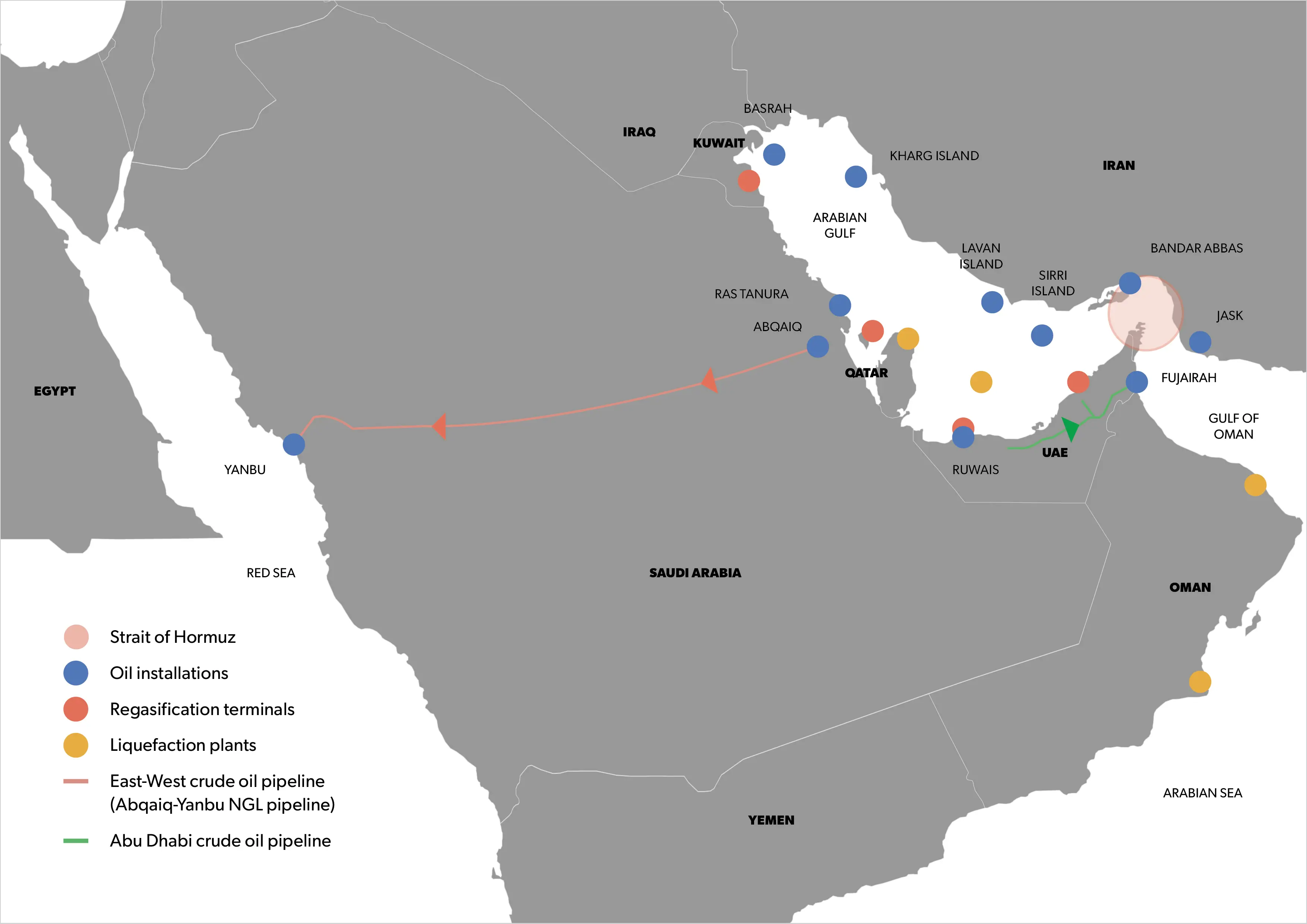

The bypass strategy and infrastructure redundancy

Faced with chokepoint exposure, states and producers are actively developing redundancy architectures and bypass strategies. However, the global system remains structurally constrained.

The Strait of Hormuz (~20 mbpd) remains the most critical global oil chokepoint, including LNG exports from Qatar and the UAE. The Bab el-Mandeb Strait (4–9 mbpd) connects the Indian Ocean to the Red Sea corridor, and the Suez Canal and SUMED pipeline (~5 mbpd combined) form the northern gateway to Europe. Together, these chokepoints represent systemic single points of failure in global energy logistics.

Existing bypass infrastructure provides only partial mitigation. Only ~3.5–5.5 mbpd can bypass Hormuz via alternative pipelines. This remains far below the ~20 mbpd transiting the Strait of Hormuz.

Key bypasses include Saudi Arabia’s East–West Pipeline (Petroline), Egypt’s SUMED pipeline, and the UAE’s Fujairah export terminal system, which function as continental “pressure release valves” enabling partial rerouting of flows during disruption events.

The central implication is that resilience does not come from avoiding chokepoints entirely, but by layering redundancy, flexibility and control across the system — accepting higher structural complexity as the cost of energy security.

Dual-track energy system: hydrocarbons and electrification

The structural response to chokepoint exposure is not about route substitution but about expanding the system into a dual-track architecture.

On the hydrocarbon side, LNG has become a central balancing mechanism in an increasingly fragmented system. Global LNG trade reached 407 million tonnes in 2024, which reflects continued expansion under tight supply conditions and rising regional divergence. LNG demand is expected to grow by over 50% by 2040, driven primarily by Asian import growth, fuel switching away from coal, and declining domestic gas production across multiple regions.

Crude oil remains the dominant physical vector of global energy trade, with approximately 80 mbpd transported via seaborne routes, reinforcing the importance of maritime chokepoints in global energy logistics. The coexistence of oil and LNG flows through the same constrained corridors amplifies systemic exposure to disruption, as a single geopolitical shock can simultaneously affect multiple energy carriers.

US$600 bn

The amount that global grid investment is projected to exceed by 2030

In parallel, the electrification of end-uses is accelerating as a second structural layer of the system. Global grid investment is projected to exceed US$600 billion annually by 2030, driven by electrified transport, industrial electrification, cooling, and rapidly expanding digital energy demand, particularly data centres and AI-related load growth.

This creates a system in which hydrocarbon logistics and power infrastructure evolve side by side, rather than sequentially.

Multi-molecule infrastructure evolution

As systems expand rather than transition, infrastructure itself is becoming multi-molecular. Assets originally designed for oil or gas are increasingly adapted to accommodate hydrogen, carbon flows, and future fuels.

40 MTPA

Of CO2 already exceeded annually in global carbon capture capacity

150 MTPA

The demand that clean hydrogen is projected to reach by 2030

Clean hydrogen demand is projected to reach around 150 million tonnes by 2030, while global carbon capture capacity has already exceeded 40 million tonnes of CO₂ annually, signalling early-stage scaling of new energy carriers.

This shift implies a structural transition from static infrastructure optimisation to infrastructure optionality, where assets are designed for repurposing across multiple energy systems over time.

Hydrocarbon supply chains: structural concentration risk

Beyond physical transport corridors, hydrocarbon systems face additional vulnerability in upstream and midstream supply chains. Critical components such as subsea systems, LNG liquefaction modules, and high-pressure compressors are highly specialised, capital-intensive, and produced by a limited number of global suppliers concentrated in the US, Europe, and East Asia.

This creates manufacturing bottlenecks that mirror physical chokepoints, where supply constraints arise not from resource scarcity but from manufacturing capacity limits and long lead times, which are typically up to 24 months for major components, and several years for full offshore developments. The result is a structurally rigid system in which responsiveness to demand shocks is constrained by industrial bottlenecks rather than geological availability.

In response, governments and firms are increasingly embedding energy security into industrial policy through supplier diversification, localisation of manufacturing, strategic stockpiling, and vertical integration of supply chains.

Strategic convergence: ADNOC as a system example

ADNOC offers a practical illustration of how these dynamics converge at the corporate level. Its infrastructure resilience is anchored by a Fujairah-linked export system that bypasses the Strait of Hormuz, reducing exposure to a key global chokepoint. This is reinforced by industrial localisation via the In-Country Value programme, which expands domestic manufacturing capacity and reduces external dependency, alongside investments in hydrogen and CCUS.

1.5 MTPA

Of CO2 captured annually by ADNOC as part of their carbon management investment

At the same time, ADNOC is investing in carbon management, capturing around 1.5 million tonnes of CO₂ annually, with plans to scale this to up to 10 million tonnes per year by 2030, embedding carbon management into its long-term operating model.

Overall, this reflects a broader strategic shift: energy resilience is increasingly defined not by individual fuels, but by integrated control over infrastructure, supply chains, and emerging energy systems.

The strategic imperatives for 2026 and beyond

Infrastructure is emerging as the central determinant of energy security in a fragmented global energy system. As energy markets shift from efficiency to resilience, control over infrastructure, supply chains, and critical transit routes increasingly defines national security and economic power.

In this era of energy addition rather than substitution, the most resilient actors will be those that operate simultaneously across hydrocarbons, electrified systems, and digital energy networks integrating molecules, electrons, and intelligence into a coherent strategic architecture capable of absorbing disruption rather than avoiding it.

- This Market Outlook report was produced as a part of ADIPEC’s Energy & Geopolitics series. For more information and coverage, visit: https://www.adipec.com/press-media/insights/