Market outlook: AI infrastructure is an energy decision before it is a technology decision

The energy industry has spent the past 18 months revisiting its own textbook on security. Closure of the Strait of Hormuz, the rerouting of tanker traffic around the Cape of Good Hope, sustained pressure on LNG flows into Asia, and, most recently, the March 2026 strikes on AWS infrastructure in the Gulf have reinstated physical infrastructure, redundancy, and chokepoint exposure to the top of every energy executive's agenda. Data is now a kinetic target. The vocabulary of resilience has moved from policy papers to capital allocation decisions inside the largest operators and sovereign wealth funds.

A second infrastructure question is now forming. It concerns a different commodity, a different set of corridors, and a different category of actors. The underlying logic is the same: a scarce, strategically valuable input is being built at scale under conditions of geopolitical fragmentation, and decisions taken in the next 18 months will set pricing power and strategic leverage for 15 years. The commodity is compute. The actors are hyperscalers, sovereign wealth funds, and the utilities that will supply them. The question is where the physical infrastructure of AI is built, and on whose terms.

For energy executives, this is an energy story that was filed under technology. Three interlocking pressures (the cost and availability of firm power, control over model and chip capabilities, and the regulatory standing of jurisdictions hosting the infrastructure) are now shaping where hundreds of billions of dollars of AI capex will land. The map that emerges from this process will reshape power markets, offtake structures, and industrial policy across at least three continents. Senior executives who read that map correctly will find their companies closer to the centre of the story than the conventional narrative credits them with.

Decisions made about AI infrastructure today are setting the cost of capital, the shape of offtake contracts, and the direction of industrial policy for the energy sector well beyond the AI segment itself.

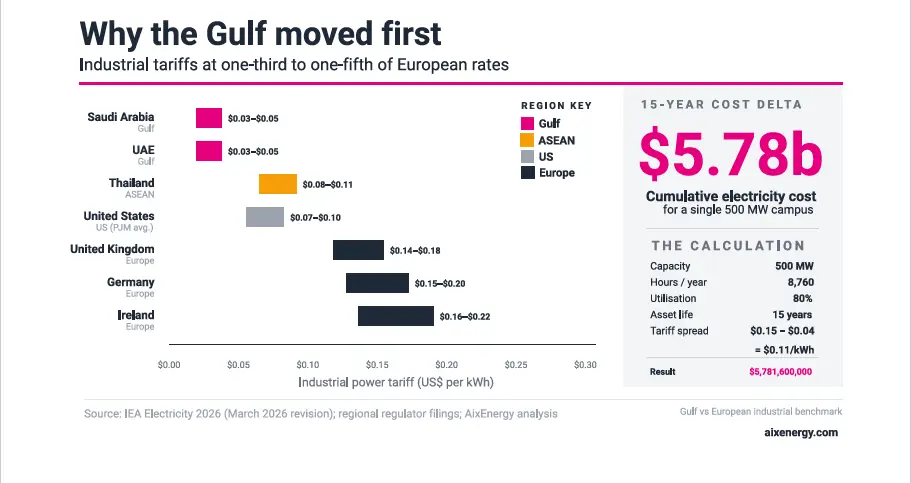

Why the Gulf moved first, and what its lead actually costs to close

The single most durable advantage in the AI infrastructure race is cheap firm power. The Gulf is currently executing on that advantage faster than any region. On 13 May 2025, Saudi Arabia's Public Investment Fund launched HUMAIN, a full-stack AI subsidiary, alongside partnership announcements with NVIDIA (several hundred thousand GPUs over five years), AMD (a $10 billion, 500 MW compute deployment), and AWS (a $5 billion AI zone). In parallel, the UAE's Stargate UAE project, anchored by G42, OpenAI, Oracle, NVIDIA and SoftBank, targets a total campus capacity of 5 GW. Its first 200 MW operational block is scheduled for delivery in Q3 2026.

These announcements are the direct monetisation of the region's most durable comparative advantage at a moment when the global economy is pricing intelligence as the binding input.

The numbers behind this advantage are straightforward. Industrial power tariffs in Saudi Arabia and the UAE range from $0.03 to $0.05 per kWh. In Germany, Ireland, and parts of the UK, the equivalent industrial rate exceeds $0.15. Applied across a single 500 MW hyperscale AI campus running at 80% utilisation over a 15- year asset life, the cumulative electricity cost delta reaches approximately $5.78 billion.

No capital structure, tax regime, or engineering optimisation closes a spread of that magnitude.

Cheap power alone does not win the decision. Speed to interconnection, regulatory certainty, and the willingness of sovereign capital to underwrite the build matter as much. This is where the Gulf's integrated model (state-owned generation, state-owned land, state-directed permitting, and a sovereign wealth fund covering the investment) compresses the decision cycle in ways federal systems struggle to replicate. A project that takes five to seven years to reach commercial operation in PJM or ERCOT can achieve first power in 18 months in Dhahran or Ruwais.

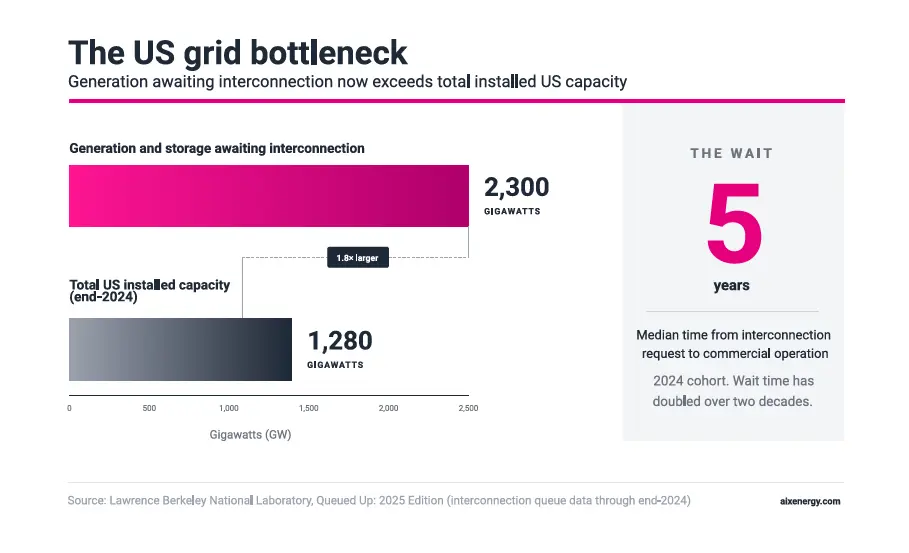

The US designs the chips and writes the models. Its grid may not catch up in time

The United States holds the opposite position to the Gulf. It dominates the capability layer (frontier models, advanced chip design, the majority of the world's AI research talent), but its grid is the binding constraint on converting that capability into deployed infrastructure at home.

As of the end of 2024, Lawrence Berkeley National Laboratory reported approximately 2,300 GW of generation and storage capacity actively seeking interconnection to the US grid, almost double the country's total installed capacity of about 1,280 GW. The median wait, from interconnection request to commercial operation, has doubled over two decades to about five years for projects built in 2024.

Without Meta taking a more active voice in the need to expand the amount of power that’s on the system, it’s not happening as quickly as we would like.

Without Meta taking a more active voice in the need to expand the amount of power that’s on the system, it’s not happening as quickly as we would like.

The asymmetry that follows is the central feature of the current AI build-out. The US can design chips and write the models but cannot reliably secure the power plants needed to run them at scale within its home territory, inside a commercially relevant window. Hyperscalers are responding on two fronts simultaneously: scouring the continental US to acquire existing interconnection rights and placing significant new capacity abroad in jurisdictions with faster build speeds. Brookfield's $5 billion commitment to Bloom Energy to provide fuel-cell power for AI data centres is one answer to the domestic problem. Gulf deployments are the other.

The US response carries a second lever beyond domestic generation: the export control apparatus governing who can buy the highest-performance chips. The May 2025 HUMAIN announcements were possible because the Trump administration rescinded the Biden-era diffusion rule that would have capped advanced chip exports to Saudi Arabia and the UAE. That single regulatory decision, made and communicated in a single week, reordered the AI infrastructure map. It also made visible how contingent the emerging map is.

China

The structural reason export controls exist is the parallel buildout taking place inside China. China's domestic AI infrastructure programme has moved at a pace comparable to the Gulf, supported by domestic chip design (Huawei Ascend, Cambricon, Biren), state-directed compute allocation, and a generation buildout dedicated to AI load. Independent estimates place new AI-dedicated generation capacity announced or under construction in China through 2028 at over 50 GW, with hyperscale campuses anchored in Inner Mongolia, Guizhou, and Ningxia, where industrial tariffs are competitive with the Gulf. The result is two AI infrastructure stacks operating in parallel rather than one. Both are real, both are growing, and both are commercially significant. Energy companies, sovereign allocators, and EPCs across the rest of the world are increasingly working with one, the other, or both.

AI infrastructure carries 1970s-style political risk under 2020s-style contracts

Energy infrastructure has always been shaped by the stability of the contracts that underpin it. Long-tenor gas supply agreements, cross-border pipeline easements, and multilateral investment treaties exist precisely because large capital cannot be deployed against political risk that shifts annually. AI infrastructure is being built under weaker contractual protection than that, and the industry has not yet priced the gap.

Gulf AI deals are, in substance, hybrid trade-and-infrastructure agreements. They combine chip allocations governed by US export licences, host country sovereign capital commitments, compute contracts with Western cloud providers, and training-and-talent programmes tied to local workforce policy. Each of these components sits under a different regulatory regime, and any one of them can move unilaterally. The stability of the whole depends on the stability of the weakest strand.

The existence of two parallel AI stacks adds a second analytical layer for energy executives evaluating offtake. Counterparties that operate Western-stack infrastructure (chips, foundation models, and cloud platforms sourced through US export license regimes) carry one risk profile. Counterparties that operate Chinese-stack infrastructure (Huawei Ascend, domestic foundation models, and Chinese cloud providers) carry a different one. Both are commercially viable. Each has its own regulatory dependencies, supply chain exposures, and capital sources. A 15-year PPA written for an AI campus needs to specify which stack the counterparty operates, what happens if the counterparty switches, and how the offtaker is protected against supply-side disruption on either side. The standard PPA template does not yet contain that language.

Energy companies considering co-location with AI infrastructure (whether through behind-the-meter power contracts, long-term PPAs to data centre operators, or direct equity participation in campus developments) introduce a risk the industry has not previously had to underwrite. The offtake counterparty may be commercially sound, but its ability to operate the asset depends on a chip supply and model licensing regime that is not under the counterparty›s control. That is a different risk profile from an LNG offtaker going bankrupt, and it requires a different analytical apparatus to price.

The implication for capital allocators is that the right comparison for AI infrastructure is not cloud computing economics. It is the risk architecture of cross-border energy infrastructure in the 1970s and 1980s, when large projects required political risk insurance, multilateral guarantees, and carefully negotiated host government agreements to be bankable. Those instruments existed because the underlying exposure was similar to that of AI infrastructure today. Firms applying that institutional memory to the new asset class will underwrite better and charge less than those treating it as an extension of cloud computing economics.

The third pole, with the highest upside and the tightest decision window

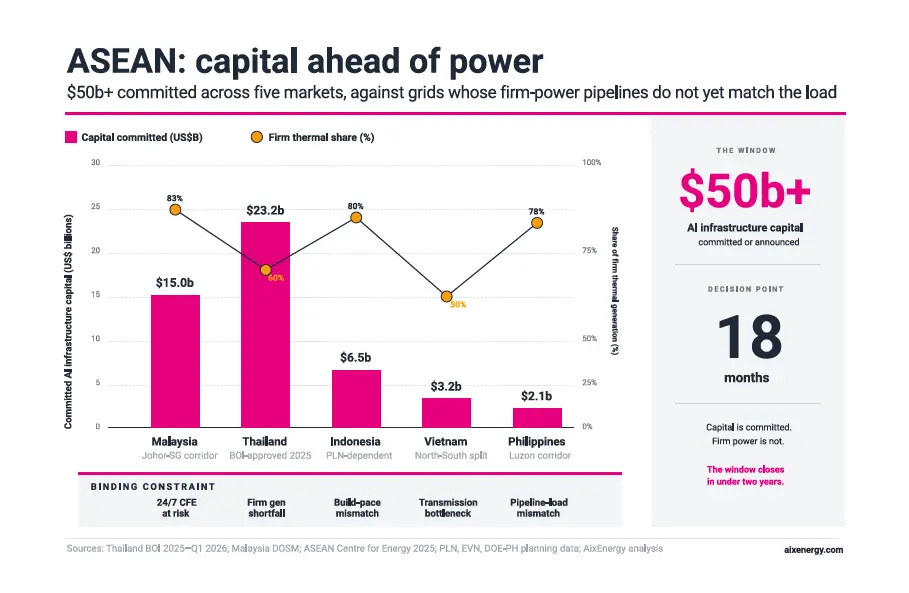

The Gulf has resolved its power question. The US has resolved its capability question. Southeast Asia is advancing on both fronts, which is why the region carries the highest upside in the global AI build-out. Committed and announced AI infrastructure capital across ASEAN now exceeds $50 billion. The energy systems expected to serve that capital are not yet built.

Thailand: the BOI signal

Thailand's Board of Investment approved 36 data centre projects worth approximately 728 billion baht (about $23.2 billion) in 2025. BOI investment applications surged 67% to $60.2 billion across all sectors in the same year, with data centres as the leading category. The BOI approved seven new DC projects at its first 2026 meeting. Thailand's Cloud First Policy is in force, and EGAT has been authorised to sell power directly to data centres above 200 MW. The Eastern Economic Corridor (EEC), spanning Chonburi, Rayong, and Chachoengsao, is the primary development zone, with Google's announced data centre on WHA Group land standing as the largest single ASEAN DC commitment to date.

The constraint is firm generation. Thailand's grid remains roughly 60% natural gas dependent, and its firm generation pipeline through 2028 covers a fraction of the peak load that approved DC projects will create at full build-out. The gap between BOI-approved capacity and firm generation under construction is the single most important variable in Thailand's AI infrastructure story over the next 18 months.

Malaysia: the Johor-Singapore corridor

Malaysia's Johor-Singapore corridor has attracted commitments from Microsoft, Amazon Web Services, ByteDance, and regional operators, including YTL Power and Sea Limited, that collectively exceed $15 billion. Johor's proximity to Singapore (which has a moratorium on new data centre capacity) gives the corridor an arbitrage role: Singapore demand, Malaysian land and power. The structural risk is grid mix. Malaysia's generation remains over 80% thermal (gas and coal combined), and its renewable rollout trails both its targets and the pace of DC commissioning.

Hyperscalers with 24/7 carbon-free energy commitments cannot meet those commitments on the current Malaysian grid, and will not be able to without a step-change in firm clean power build-out. The corridor's longer-term retention risk runs through that gap.

Indonesia, Vietnam, and the Philippines

Indonesia, Vietnam, and the Philippines each carry pipelines in the low-to-mid single-digit billions, and each presents a distinct structural question. Indonesia's announced DC pipeline approaches $6.5 billion, anchored by Microsoft's $1.7 billion Jakarta cloud region announcement and a series of smaller hyperscale and colocation commitments. The challenge is grid: roughly 80% of generation is currently thermal, and the planned PLN renewables build-out is paced to a different curve than DC commissioning.

Vietnam's pipeline sits at approximately $3.2 billion, with Viettel, VNPT and FPT operating domestic infrastructure and international hyperscalers exploring entry. The grid is comparatively cleaner (around 50% thermal) thanks to significant hydro, but Vietnam's hydro capacity is concentrated in the north, while DC demand is forming in the south. The North-South transmission corridor is the binding constraint, not generation mix. Hyperscale siting decisions in Vietnam will track grid reinforcement schedules more closely than headline renewable capacity.

The Philippines carries a lighter pipeline at around $2.1 billion, dominated by ePLDT, Globe, and Converge IT, alongside hyperscale interest tied to the Luzon Economic Corridor announced in 2024. Generation mix is around 78% thermal, with the firm generation pipeline through 2028 not yet matched to announced data centre load.

The China dimension

ASEAN AI infrastructure cannot be read without the China dimension running through it. Chinese hyperscalers operate meaningful regional capacity: Huawei Cloud has data centre presence in Singapore, Malaysia, Thailand and Indonesia; Alibaba Cloud operates regions in Singapore, Malaysia, the Philippines and Indonesia; Tencent Cloud has expanded into Indonesia and Thailand. A substantial share of the firm power that will serve all five ASEAN markets, including campuses operated by Western hyperscalers, is being engineered and built by Chinese EPCs and equipped with Chinese gas turbines, transformers, transmission equipment, battery storage and cooling systems. PowerChina, CEEC, Sungrow, CATL, and BYD are visible counterparties in the regional buildout.

This is a new reality. We have to keep the lights on, power the AI economy, and make sure no one gets left behind.

ASEAN governments are increasingly making explicit choices about which stack each project supports. Those choices are commercial and technical before they are political: which equipment is bankable, which financing is available, which timeline is achievable, which standards apply. The choices are also durable: a campus built around one stack rarely converts to the other inside its 15-year asset life. The map of ASEAN AI infrastructure is being drawn through these decisions as much as through the BOI approvals and PPA discussions covered earlier in this section.

The ASEAN window

In aggregate, the resulting situation across the five markets is the textbook definition of high variance. If the region's Independent Power Producers (IPPs), utilities, and regulators can coordinate firm power expansion at the pace AI capital requires, ASEAN becomes an additional pole on the global AI infrastructure map.

The decision point is not 10 years away. It is in the next 18 months. Resolution will not happen in one capital or through one bilateral agreement. It will happen through serial engagement between operators, hyperscalers, sovereign allocators, and regulators whose decisions sit upstream of every project.

Strategic implications

The conventional reading of the AI build-out framed it as a technology story with energy consequences. The sequence now runs the other way: firm, cheap, fast-to-connect power is the constraint that determines where AI infrastructure goes. Energy companies, utilities, and sovereign allocators hold more agency in this build-out than the prevailing narrative credits them with.

Three implications follow:

- First, capacity planning: AI load forecasting needs to enter capacity plans as a structural variable. A single 500 MW hyperscale campus is a larger load than most industrial cities, and the decision to host or refuse one reshapes a utility's capital plan for a decade.

- Second, offtake structures: the standard PPA was not designed for counterparties whose operational viability depends on chip export regimes and foundation-model licensing terms. Risk-sharing provisions, change-of-law clauses, and minimum offtake guarantees need to be redrafted to reflect the actual risk geometry.

- Third, industrial policy framing: governments are beginning to treat AI-ready generation capacity as strategic infrastructure, on par with pipelines, LNG terminals, and grid interconnections. Companies that align with that framing early will shape the regulatory environment rather than be shaped by it.

A fourth implication sits underneath these. The industry's established playbook for pricing political and regulatory risk, built over decades of cross-border oil, gas, and LNG projects, contains most of the tools needed to underwrite AI infrastructure correctly. Those tools have not yet fully migrated across. Political risk insurance, host government agreements with stabilisation clauses, multilateral guarantees, and carefully structured offtake priority rights were all developed in response to the kind of contingent, multi-jurisdictional exposure that AI infrastructure now carries.

The most resilient position in the emerging map belongs to actors who operate across all four dimensions simultaneously: exposure to cheap firm power, meaningful influence over the capability stack that runs on it, jurisdictional standing that survives political cycles, and a clear operating relationship with both AI infrastructure stacks. Few organisations currently do. The ones that move first to build that position will define what the energy-intelligence convergence looks like for the next industrial era. The next 12 to 18 months are when the map gets drawn. After that, the positions are taken.

- This Market Outlook report was produced for AixEnergy. For more information and to register as a delegate, visit AixEnergy2026.