The discovery deficit reshaping global oil and gas supply

The world’s adoption of an energy-addition policy over transition, coupled with economic and technological growth, means the world needs more hydrocarbons.

But a potential future shortfall is emerging as the industry confronts pressure to discover more oil and gas resources to service future needs and ensure energy security.

Exposing the gap

A financial disconnect is increasingly evident after a decade where investment in exploration has lagged behind production.

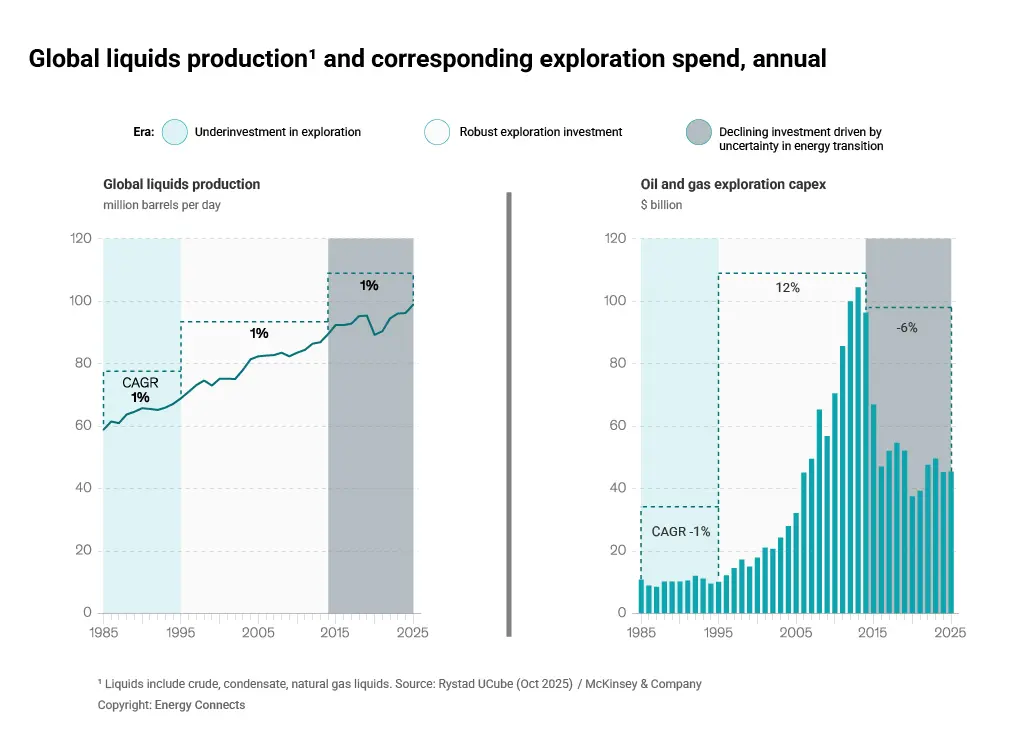

McKinsey & Company says capital spending on exploration has never been so low relative to production, suggesting a “discovery gap” as industry outlooks predict demand through to 2040. Part of the reason lies in uncertainty over the pace of the transition, combined with the need to generate investor returns.

This equation has led some energy companies to seek income from short-cycle projects, meaning more funds for finding projects such as onshore shale instead of areas requiring longer-term strategies, such as exploration and well discovery.

As the narrative has shifted, so too have conversations, as executives contemplate finding new oil and gas in the face of rising energy demand that cannot be met by renewables alone.

The supply-and-demand gap is widening, but reserves cannot be rebuilt without renewed exploration.

McKinsey’s Global Energy Perspective (GEP) projects a 25 million barrel per day oil shortfall by 2040, while production from existing wells declines each year.

Total discovered resources in the last decade have dropped by more than 50%, from 331 to 156 billion barrels of oil equivalent. Only Guyana has yielded a sizeable new basin in the last decade. McKinsey notes: “Many companies now face hollowed-out exploration teams, long cycle times, increased unit exploration costs, and low success rates.”

Shrinking capital

The US/Israel conflict with Iran has resulted in damage to oil and gas infrastructure in the UAE, Qatar, Bahrain, and Saudi Arabia. The extent varies, as do the anticipated duration and cost of repairs; further disruption is being factored in by an industry currently confronting frozen production as shipping remains stalled through the Strait of Hormuz.

In addition, consumers and refiners are tapping into oil inventories to mitigate the immediate impact of supply upheaval. In March, global oil stocks fell by 85 mb, even as on-land and offshore inventories grew in the Middle East and China, according to the IEA’s Oil Market Report (OMR).

“Global crude throughputs continue to struggle with disruptions to feedstock supplies and infrastructure damage that are tightening global product markets,” said the OMR.

McKinsey notes that reserve-replacement ratios have hit historic lows. Many firms now produce more oil and gas than they discover.

It identifies reduced capital expenditure as the primary of six reasons exploration has shrunk, falling about 6% each year since the 2014-15 crash; the same percentage increase for exploration wells drilled until then from 1995. That has since dropped about 12% annually.

Finding costs per barrel have climbed amid diminishing discovered resources and unattractive, lengthy cycle times averaging 20 years from exploration to oil recovery.

McKinsey says investors have tended to be risk-averse about long-term oil and gas returns in an uncertain energy transition climate, pushing firms towards near-term cash flow opportunities. This has “diluted portfolio optionality”.

In turn, talent pools and experience in companies have eroded, while few discovery prospects have clear seismic or geophysical signatures, increasing uncertainty in technical assessments and making portfolio outcomes less reliable.

Addressing the supply gap

Experts suggest a reset is required, beyond the geopolitical shocks currently impacting energy supplies.

It is clear long-term energy demand is going one way, so upstream investment must scale in exploration, infrastructure, and human capital — to ensure secure, reliable, affordable supplies.

McKinsey says companies will be required to make “integrated shifts in strategy, operations, and capabilities”.

This includes prioritising commercial barrels, moving faster with agile governance, and modernising risk frameworks to back more and larger bets.

It echoes suggestions to deploy digital capabilities and AI to compress cycle times and improve hit rates, “all while delivering strong risk-adjusted returns and lower environmental intensity to meet investors’ expectations”.

If limited exploration traits persist, operators could rely on costlier, more carbon-intensive barrels, something that clashes with decarbonisation aspirations in a delicate global economic environment.

McKinsey concludes: “With renewed talent, strategic partnerships, and a focus on advantaged resources at scale, exploration can play a decisive role in securing future oil and gas supply."