China Emerges as Unlikely Haven as Oil Price Shock Hits Global Markets

(Bloomberg) -- As the war in Iran sent oil prices soaring, one market holding up unexpectedly well is that of the world’s largest crude importer: China.

Chinese stocks have fallen less than global peers since the conflict began, the yuan has held steady against the dollar and government bond yields have barely moved. Together, this amounts to surprising resilience in a crisis that, at first glance, appeared likely to leave the country vulnerable.

For decades Beijing has sought to insulate its economy from precisely this kind of shock. It poured investments into renewables, secured dominance across much of the clean-energy supply chain and promoted electric vehicles at a remarkable speed. The result is an economy still dependent on imported fossil fuels but less beholden to them than before — providing some protection as oil prices have jumped as much as 65% since the conflict.

“Chinese asset classes are something that is missed by global investors as a safe haven,” said Cary Yeung, head of Greater China debt at Pictet Asset Management.

Global markets have been on a roller coaster since the war broke out late February. Stocks slid as crude — which briefly surged to almost $120 a barrel — threatened to stoke inflation and delay central bank easing, only to rebound on signals from Washington hinting at a possible end to the fighting.

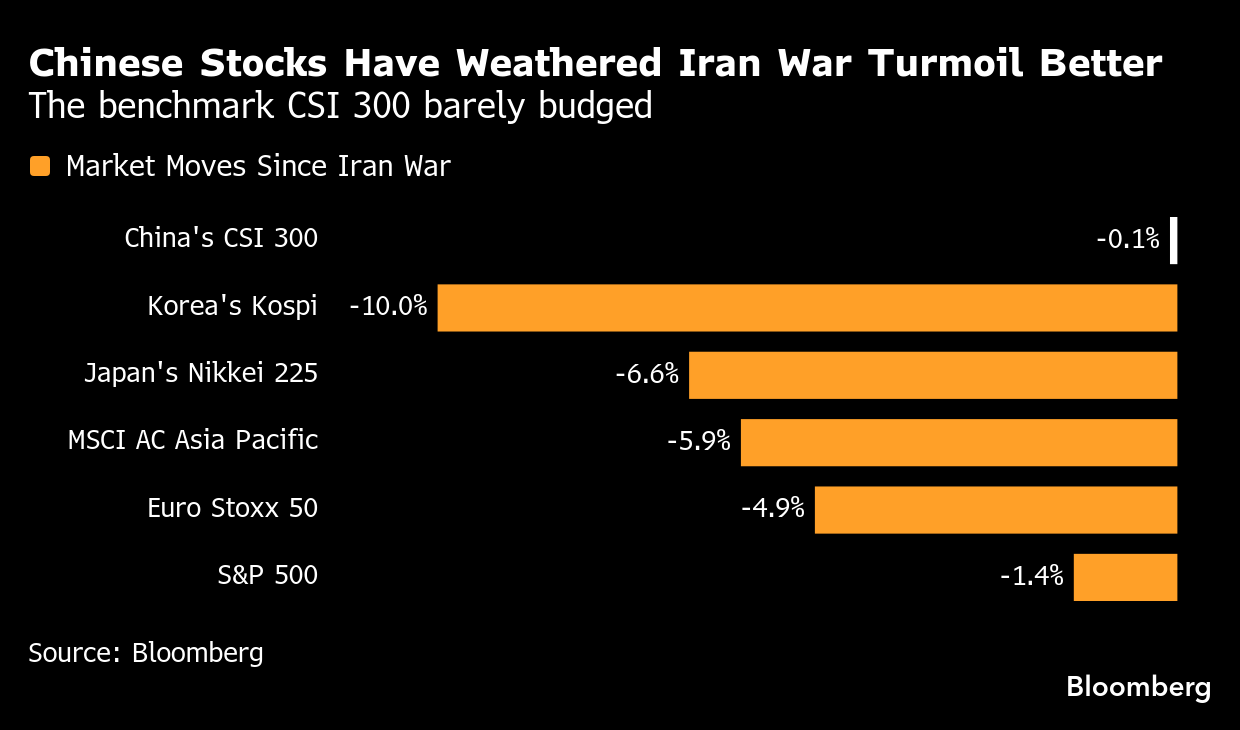

Asian equities have taken the hardest hit, given the region’s heavy reliance on imported energy. Japan, Korea and India are down about 7%, 10% and 5% respectively since late February. European markets have lost around 5% and US stocks fell 1.4%.

Yet China’s CSI 300 barely budged, slipping just 0.1%. That means an investor who parked money in Chinese shares instead of moving out from Asia into America would have preserved more capital than in most major markets. Goldman Sachs Group Inc. this week reiterated its overweight rating on Chinese equities.

Currency and bond markets paint a similar picture. The yuan has outperformed all Asian peers and is little changed against the dollar, even as the greenback climbed on haven demand. The trade-weighted CFETS RMB Index hit a one-year high last week. China’s 10-year government bond yield has climbed by less than one basis point — far less than the more than 20-basis-point jump in comparable US Treasuries and French debt.

‘Relative Outperformance’

An anticipated summit between President Donald Trump and Chinese leader Xi Jinping later this month may reinforce that perception of stability. It’s “certainly not crazy” to think a productive meeting could be a positive pillar of support, said Trevor Slaven, global head of asset allocation and multi-asset at Barings.

To be sure, few investors see the geopolitical jolt alone as reason to rotate broadly into Chinese assets.

“Chinese assets could continue to show relative outperformance in the near term, though we would view this as tactical rather than structural,” said Clarence Li, lead portfolio analyst for multi-asset and equity strategies at T. Rowe Price.

Ultimately, the market outlook still hinges on the domestic economy and policy execution. “The China angle is therefore more about selective thematic exposure than a conviction call across equities, bonds or FX,” he added.

Investors looking at China are focusing on sectors linked to energy security and domestic demand. The CSI 300 Energy Index has risen about 8% since late February, making it the best performing sub-gauge. Renewables, an industry China dominates, have jumped, with Jinko Solar Co. up around 11% in Shanghai.

Conditions still favor derisking. Any defensive shift into Chinese assets would probably come only after volatility subsides — and more likely into equities than government bonds, according to Barings’ Slaven.

Energy Security

Beijing’s energy strategy helps explain why its markets are holding up better than expected.

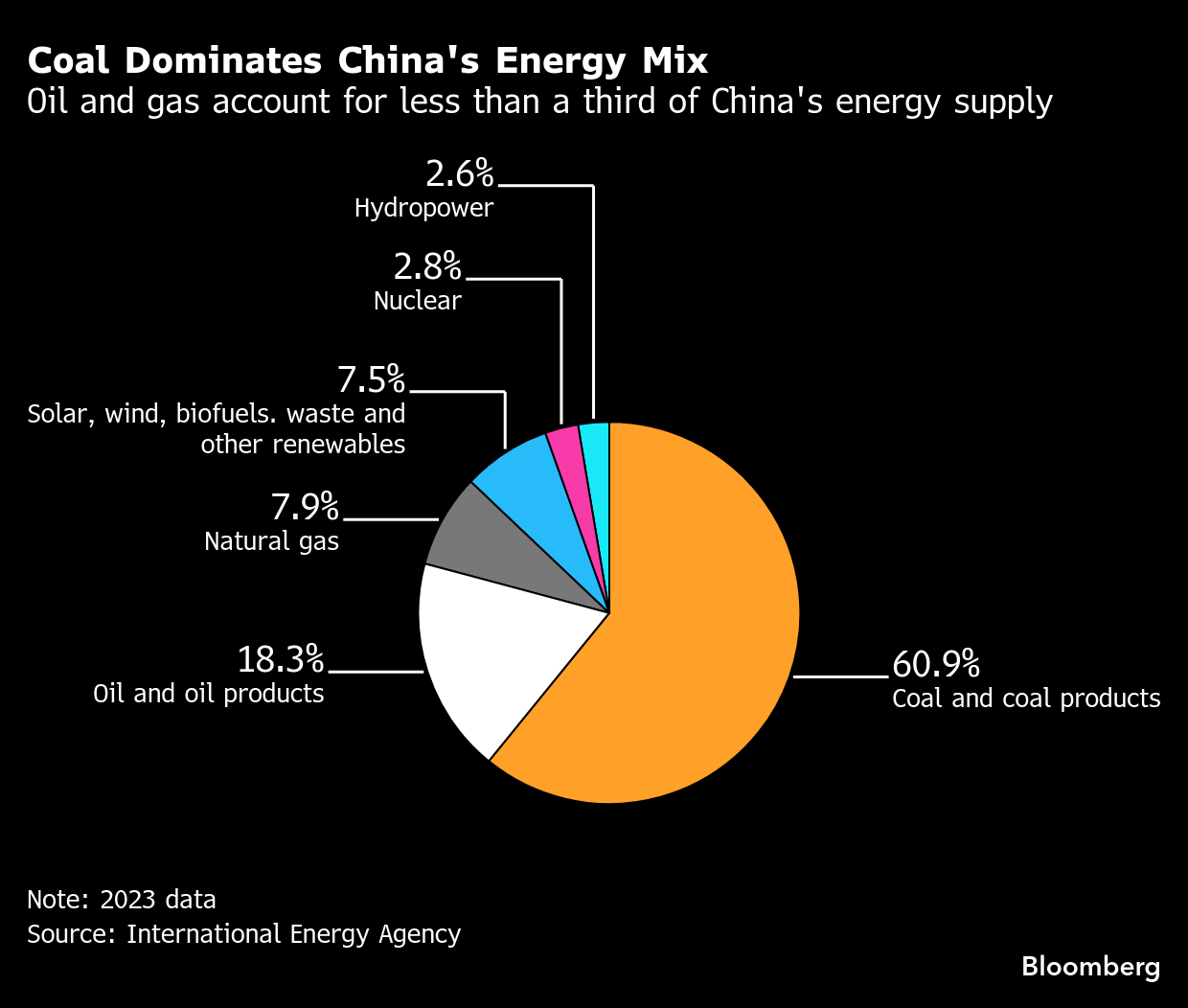

The government has prioritized ensuring stable energy supplies after being stung by a series of power shortages in 2021 and 2022. Coal mining surged to a record, coinciding with a huge wave of solar and wind supply and their battery backups, which are more than meeting growth in electricity demand. China has also been steadily increasing oil and gas production at home.

The country has been chipping away at fossil fuel use in key areas. EVs and hybrids now outsell traditional autos in China, leaving gasoline — which makes up more than a fifth of the country’s oil consumption — in long-term decline.

Beijing has built significant buffers as well. Tens of millions of barrels of illicit crude from Iran, Russia and Venezuela are sitting on tankers near its coast, according to data provider Kpler. China’s strategic oil reserves have risen to an estimated 1.4 billion barrels — more than triple US levels, and enough to cover about six months of lost Middle Eastern imports in a worst-case scenario.

“The short-term impact is limited and can be cushioned,” said Larry Hu, head of China economics at Macquarie Group. Even if crude is at $100 a barrel, he estimates China’s consumer inflation would rise to just around 1%.

The bigger risk is that elevated oil prices dent global growth and, in turn, China’s exports — a crucial engine of its economy, according to Hu.

Domestic challenges also remain significant. Weak consumer demand, a prolonged property downturn and cautious policy easing continue to weigh on investor sentiment. T. Rowe Price, for instance, remains neutral on China overall despite the market’s relative stability.

Officials in Beijing have signaled restraint on stimulus, preferring to preserve policy ammunition in case of a deeper oil shock or renewed US-China tensions. This year’s GDP growth target was set at the lowest level since 1991 and fiscal support has been dialed back, though economists expect borrowing and spending to ramp up if the economy encounters a major setback.

If the conflict in Iran drags on longer than expected, China’s relative resilience could become even more pronounced, William Bratton, head of cash equity research for APAC at BNP Paribas SA, said in a note Monday.

“We view China as relatively attractive versus the rest of the region given its more domestically-oriented economy, including in terms of energy supplies,” Bratton said.

(Updates with Goldman’s rating in seventh paragraph)

©2026 Bloomberg L.P.