It’s Tough to Short Adani Stocks Listed in India. Here’s Why

(Bloomberg) -- Hindenburg Research’s decision to only go short on Adani Group securities outside India has highlighted the limitations of the practice in the nation and the peculiarities of the business empire itself.

India’s authorities have imposed a bevy of restrictions on short selling, including requiring institutional investors to disclose planned trades to the stock exchange before they are executed, and making their retail counterparts close positions each day. They also enforce the globally-favored ban on naked shorts, the practice where investors sell shares they haven’t borrowed first.

Shorting the Adani Group also comes with its particular difficulties. The Indian-listed entities all have a relatively low free float and few institutional investors, which means there is a scarcity of shares for short sellers to borrow, and they are therefore more expensive. Founders and controlling shareholders hold at least 60% in nine of the 10 stocks, data compiled by Bloomberg Intelligence show.

The fact that there was little short selling of Adani shares meant there was hardly any short covering that would normally limit a stock’s downside.

“The delicious irony is that shares of Adani companies are tanking hard or limit down partly because India makes it so hard to short in the first place,” short-selling specialist Scorpion Capital Partners said last week in a tweet. There was “no one to step in on the other side,” it said.

Hindenburg made clear in the disclosure to its report that its positions were all offshore. The shorts on the Adani Group’s companies were held through U.S.-traded bonds and non-Indian traded derivatives, along with other non-Indian-traded reference securities, it said. The short seller declined to comment on its decision to use offshore instruments, when contacted by Bloomberg.

Theoretically the potential gains are enormous. A trader who sold $1 million Adani Enterprises Ltd. shares at the open on Feb. 1 and bought them back at the end of the same day after the record 28% plunge would have made about $280,000, excluding fees and transaction costs, according to Bloomberg calculations.

Shorting Adani Group shares is far more costly than betting against some of its Indian peers.

Borrowing stock of Adani Enterprises cost traders 8 rupees (10 US cents) each on Jan. 16, the latest available figure, according to data compiled by Bloomberg. That compares with a January average of 0.22 rupee for shares in Reliance Industries Ltd., India’s largest stock by market value.

But even for other stocks, the market for borrowing and lending in India remains tiny, according to Kamal Visaria, founder trustee at Visaria Family Trust in Mumbai.

India’s stock-lending-and-borrowing segment “hasn’t matured at the rate at which it was expected to and is still very small relative to similar mechanisms in more developed markets,” he said.

In the US, shares borrowed amounted to about 4.2% of float across the market at the end of last quarter, according to S3 Partners, a provider of financial data. In contrast, volumes in India’s $3.2 trillion cash equities market are negligible and the derivatives segment is more liquid and typically used by traders, Visaria said.

Given that shorting Adani stock in India can be problematic, short sellers may prefer to use derivatives.

An India-based investor can either buy put options, sell calls, sell futures or create a multi-leg options strategy that benefits from a fall in shares of four of the Adani group stocks listed in India, namely Adani Enterprises, Ambuja Cements Ltd., ACC Ltd. and Adani Ports & Special Economic Zone Ltd.

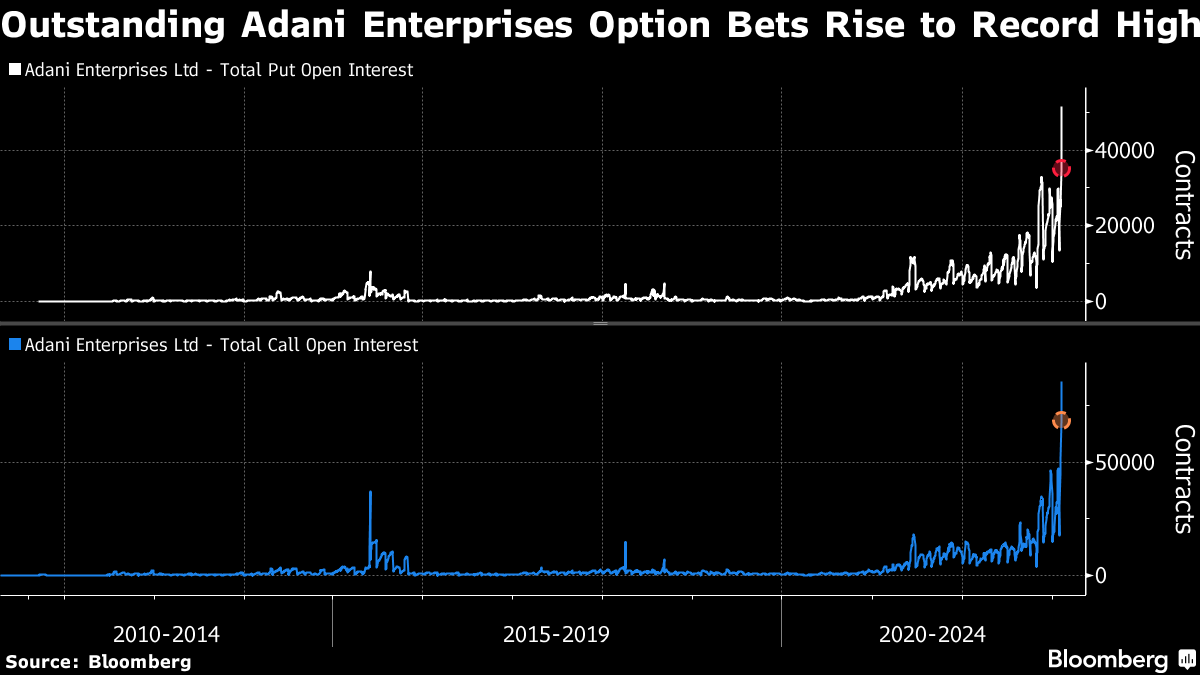

Volumes for options linked to Adani stocks have surged amid the volatility. Open interest on such contracts linked to Adani Enterprises — or positions yet to be settled — climbed to a record last week.

’Very Laborious’

Even to do this though, global investors need a Foreign Portfolio Investor license to be able to trade onshore derivatives, which can be difficult to obtain despite the regulator easing rules in 2019.

“It’s a very laborious process,” said Soren Aandahl, founder of short-selling firm Blue Orca Capital LLC, who is known for his bets against Hong Kong-listed companies. “It’s very difficult to get that license approval from a regulator.”

Alternatively, there are offshore derivatives traded in Singapore and Dubai, but liquidity in those instruments can be extremely thin. About 216,800 lots of Adani Ports & Special Economic Zone’s contracts for February delivery were traded via the National Stock Exchange of India Ltd. by late Friday, compared with just 90 in Singapore.

“There’s a lot of hurdles to trading that market,” Aandahl said of India. “And unfortunately with India, the ones that you can trade through the offshore futures exchanges, they tend to be just much bigger companies but even so the liquidity is not that fantastic.”

--With assistance from and .

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.