US Frackers Return to Haunt OPEC’s Pricing Strategy

(Bloomberg) -- OPEC’s one-time nemesis — US shale — is rearing its head just months after the sector was all but written off as a threat to the cartel’s sway over worldwide oil markets.

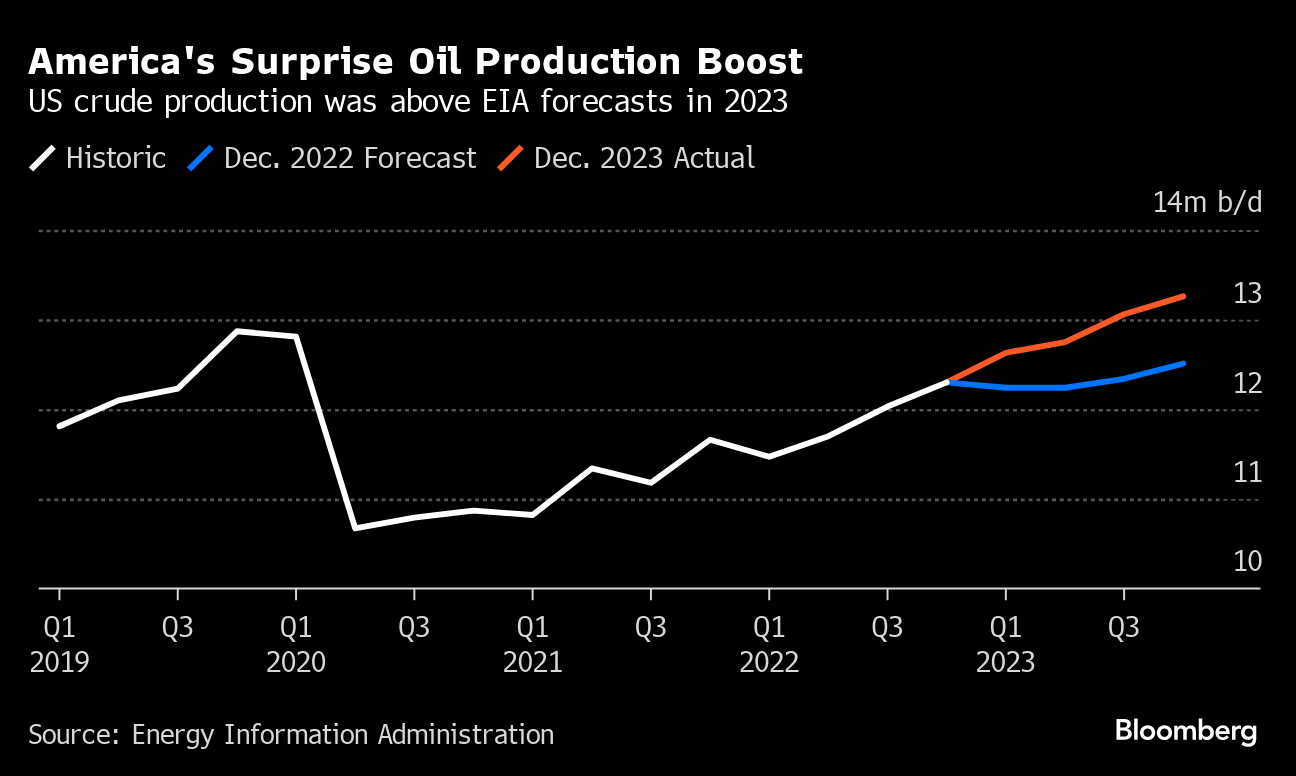

Drillers from the Permian Basin in West Texas to the Bakken Shale of North Dakota have ramped up oil production well beyond what analysts foresaw, pushing output to a record just as OPEC and its allies put the brakes on supplies in a bid to arrest price declines.

This time last year, US government forecasters predicted domestic production would average 12.5 million barrels a day during the current quarter. In recent days, that estimate was bumped to 13.3 million; the difference is equivalent to adding a new Venezuela to global supplies.

That growth is reverberating around the world, calling into question the OPEC+ group’s strategy of curbing supplies to prevent the potentially catastrophic price impacts of a glut. It also makes clear that the legions of companies that pump oil from US shale fields still wield enough power to bedevil the cartel’s efforts.

“The US clearly played a huge role in the global market in 2023, including pressuring OPEC+ to curtail their output,” Wood Mackenzie Ltd. analyst Ryan Duman said during an interview.

The Organization of Petroleum Exporting Countries, abetted by its Russian ally, overtly sought to check the influence of North American shale as early as 2014, when the group flooded world markets with crude in a bid to recapture market share from the ascendant US oil sector. The move aggravated an existing supply glut and triggered a 65% plunge in crude prices that took 14 months to bottom out.

That collapse sent a jolt through the economics of US shale, ending years of breakneck production growth. And although the expansion eventually resumed, it was thrown into reverse by the global pandemic in early 2020. The shale industry emerged from that setback with a resolve to prioritize returning cash to investors instead of chasing production gains.

Meanwhile, in the years since the 2014-2016 selloff, the OPEC+ alliance, as it came to be known, worked to enforce supply quotas among member nations as part of a broader strategy of balancing global supply-and-demand to maintain robust prices.

That self discipline helped stabilize the market in 2020, and again this year in the face of slowing demand and a glut of oil. But OPEC+’s latest cuts announced at the end of November haven’t stopped crude from slipping further. And all the while, US shale — plus production in places like Brazil and Guyana — has crept higher. Further action by OPEC+ may be needed to shore up the market: Saudi Energy Minister Prince Abdulaziz bin Salman told Bloomberg earlier this month that the group can “absolutely” maintain discipline beyond the first quarter of 2024 if required.

What Bloomberg Intelligence Says

The OPEC+ 1 million barrels-a-day voluntary output cut won’t inspire much confidence as smaller members have little incentive to abide by its terms and larger ones may not reduce exports due to seasonality. ... US shale growth and a recovery in Iranian and Venezuelan output could effectively offset all the additional proposed cuts through 1Q.

— Fernando Valle and Salih Yilmaz, BI analysts

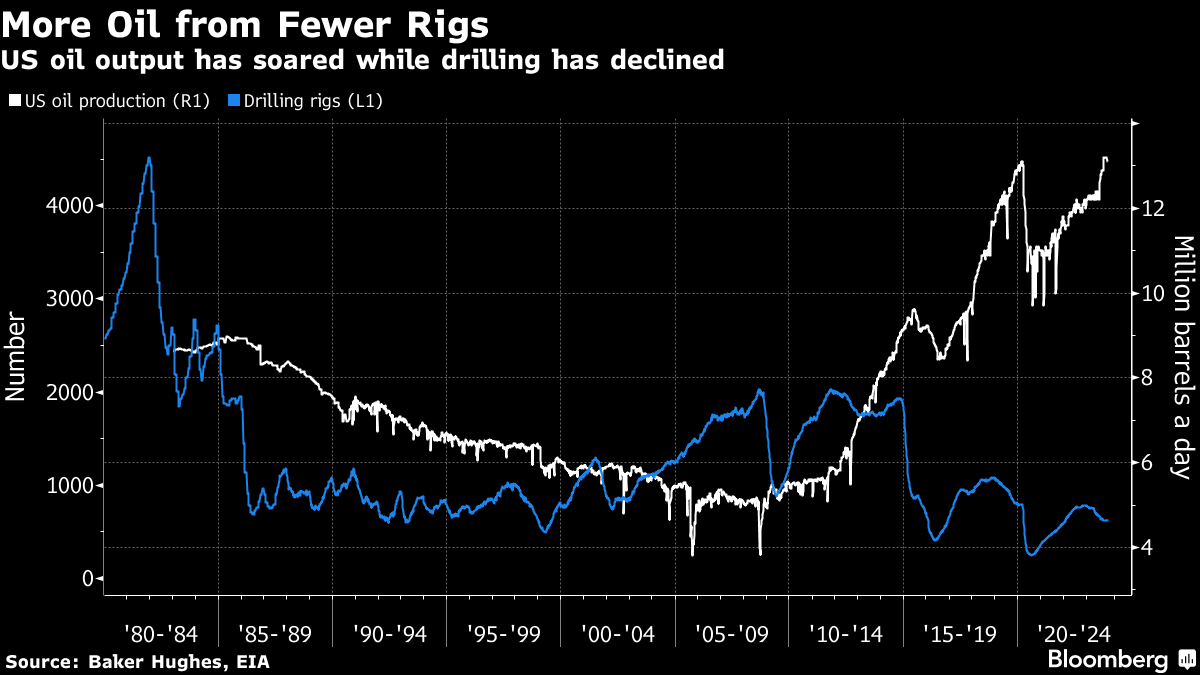

Part of what makes the US crude surge surprising is that companies managed to increase production even as the number of drilling rigs at work fell roughly 20% this year. That productivity gain has confounded many analysts and researchers who have long relied on the so-called rig count as a predictor of future crude output.

Explorers are squeezing crude out of new wells more efficiently because of innovations in everything from electric-pump technology to new strategies for deploying workers while fracking wells to minimize downtime. A key example has been the replacement of the iconic, decades-old pumpjack with high-tech underground gear as tall as a three-story building that sits inside a well to push more crude to the surface.

On a recent windswept morning in the Permian Basin of West Texas, Diamondback Energy Inc. drilling chief Yong Cho stood in a control room part-way up a 180-foot (55-meter) rig as a crew went to work on a fresh well. The company has reduced the time it takes to drill an average well by about 40% over the last three years, thanks in part to boring slightly smaller holes, adjusting the solution that’s pumped down shafts to power drills, and subtle refinements in the steel-and-polycrystalline-diamond-tipped bits.

“In 2019, the average well took me 19.5 days,” Cho said during an interview afterward. “Now it takes me 11.5 days.”

But a shale well isn’t finished when the drilling is done. A separate array of workers and gear is called upon to frack it so that crude can begin to flow. It’s the last and most-expensive part of oil production, and frackers have achieved similar efficiency gains, shortening the process by three days to little more than a week per well, according to Kimberlite International Oilfield Research.

“Every year we’re seeing more efficiency,” Chevron Corp. Chief Executive Officer Mike Wirth said during a recent talk at the Council on Foreign Relations. “And you’re seeing, through a number of acquisitions and consolidations, companies that have the scale to bring these capabilities to bear in a way that just drives further efficiency and industrial kind of progress there.”

Analysts had expected US producers to increase output modestly this year. That’s partly because after years of heavily investing in production and being burned by downturns, companies pledged to keep spending in check and focus on returning cash to shareholders.

The role of private producers may have also caused forecasters to underestimate oil production because their activity is harder to model than publicly-listed peers who report earnings every quarter.

Out of the 10 fastest growing producers by volume since the pandemic, seven of them were private companies, according to S&P Global. Mewbourne Oil Co. and Endeavor Energy Resources LP led the charge, adding more barrels to the market than Exxon Mobil Corp. since 2019.

There are indications that US drillers may once again exercise more restraint when it comes to expanding budgets. Annual growth in industry spending is estimated to be just 2% in 2024, down from this year’s 19% growth rate and a fraction of the record 44% increase of two years ago, according to Evercore ISI.

“It’s not drill, baby, drill like it was during the shale boom,” Angie Gildea, who leads KPMG’s US energy practice, said in an interview. “It’s meaningful but measured growth.”

©2023 Bloomberg L.P.