Iran War Tests Whether Clean Tech Learned Any Lessons From 2022

(Bloomberg) -- For green investors, the current war-fueled surge in oil and gas prices conjures up painful memories of 2022, when renewables were gripped by a selloff that lasted into 2025. But at Jefferies, clients are being urged to double down on a bold upbeat call.

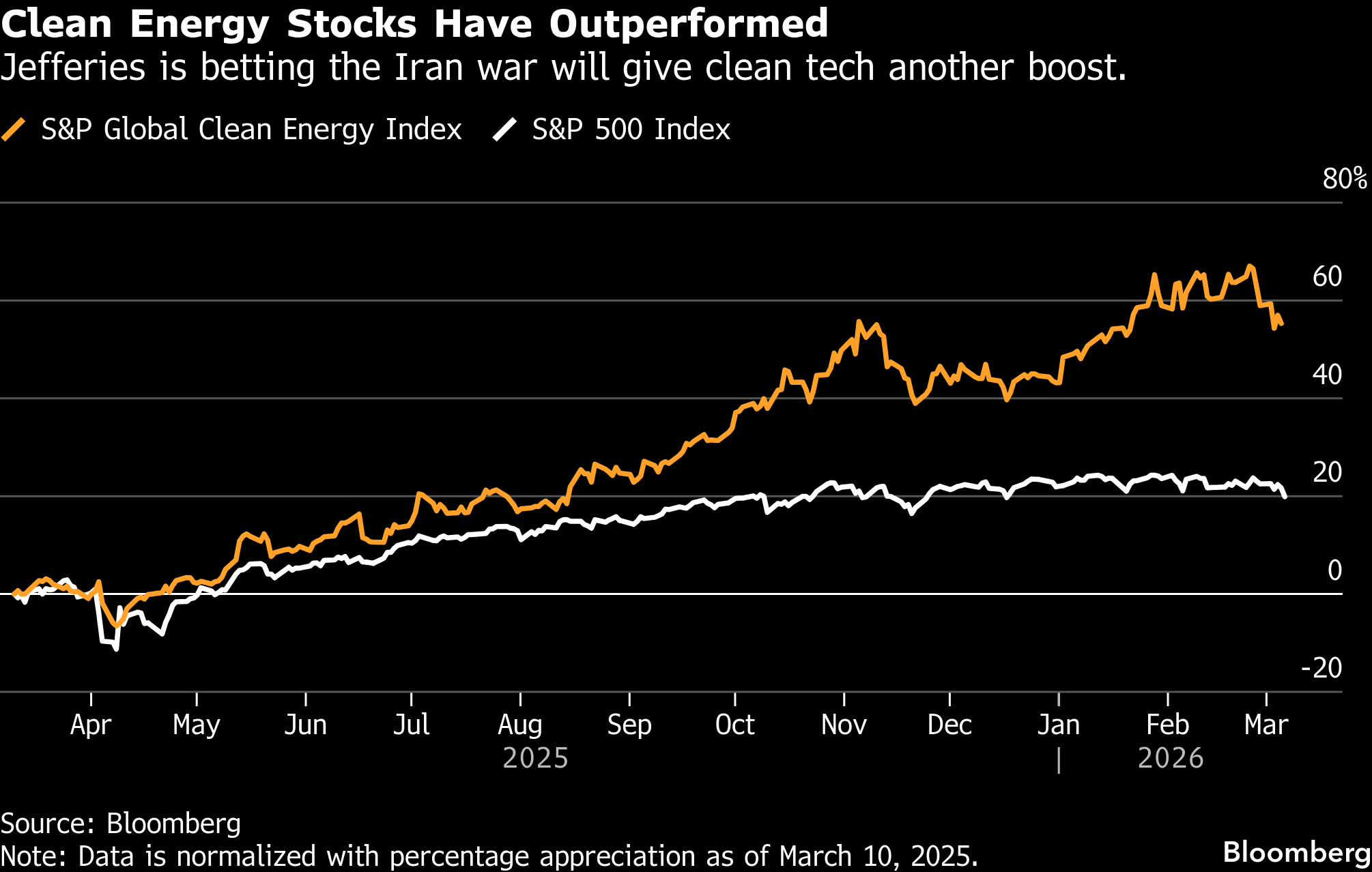

Last year, Jefferies started telling green investors they were entering the “glory days” of a strategy that had long seemed like a losing bet. That advice ended up coinciding with a 44% surge in clean energy stocks in 2025, trouncing the 16% gain in the S&P 500 Index.

Now, despite the prospect of higher inflation, higher interest rates and supply chain disruptions — a cocktail that in the past has derailed green strategies — Jefferies is telling clients not to panic and to stick with the clean energy sector.

The guidance of 2025 is “still very much” the narrative at Jefferies today, according to Aniket Shah, the New York-based bank’s global head of sustainability and transition strategy. Jefferies hasn’t changed its outlook “at all,” and expects the Iran war to trigger a new wave of investment in renewables as governments race to increase energy independence, he said.

Investors staying the course this year have — for now — been rewarded with market-beating returns. The S&P Global Clean Energy Transition Index is up more than 6%, compared with a roughly 1.5% decline in the S&P 500 Index. But the weeks and months ahead look set to test their conviction.

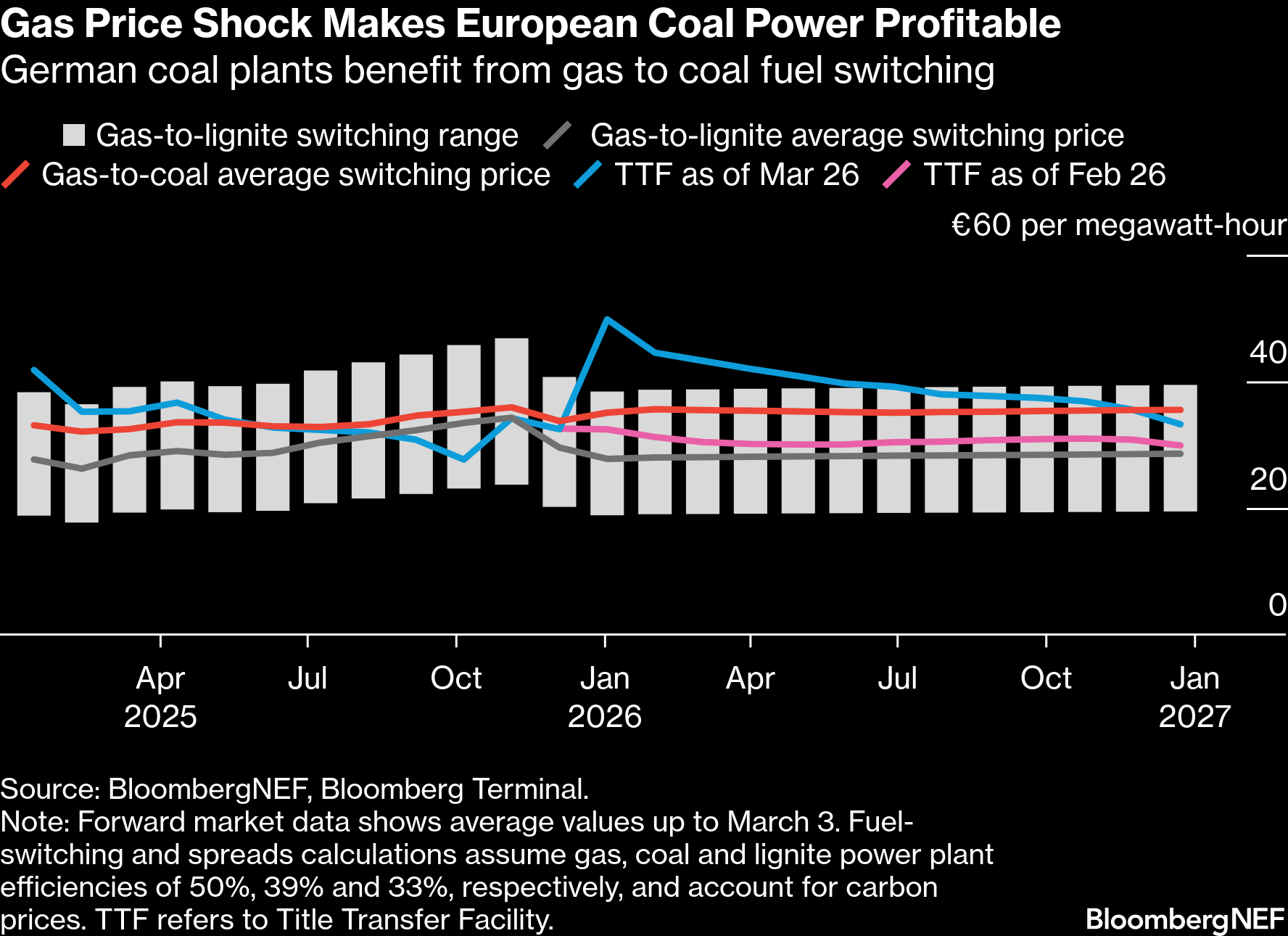

The disruption to energy markets caused by the Iran war is not only bolstering oil and gas prices, but it’s also buoying the dirtiest fossil fuels. BloombergNEF notes that after months of pressure, Europe’s coal and lignite power generators are now back in the money, as a direct result of the spike in gas prices.

“Elevated oil and natural gas prices will strengthen fossil fuel earnings in the short term and they are going to temporarily outperform clean energy equities,” said Patrick J. Murphy, executive director of the geopolitical unit at Hilco Global and a former under secretary of the US army.

At the same time, for long-term investors such as pension funds and sovereign wealth funds, “there is no doubt” that they’ll remain “extremely committed to decarbonization,” he said.

A number of factors are different now compared with 2022, according to analysts, investors and fund managers interviewed by Bloomberg. There’s evidence that green companies have been bolstering their balance sheets, applying stricter risk management standards and higher return requirements before embarking on new projects.

Any interest rate effect may also be less pronounced now than it was in 2022, said Carole Laible, chief executive officer at Domini Impact Investments.

“Rates could be a bit higher in 2026, but I don’t think that it’s enough to have a significant impact in having those projects move forward,” Laible said.

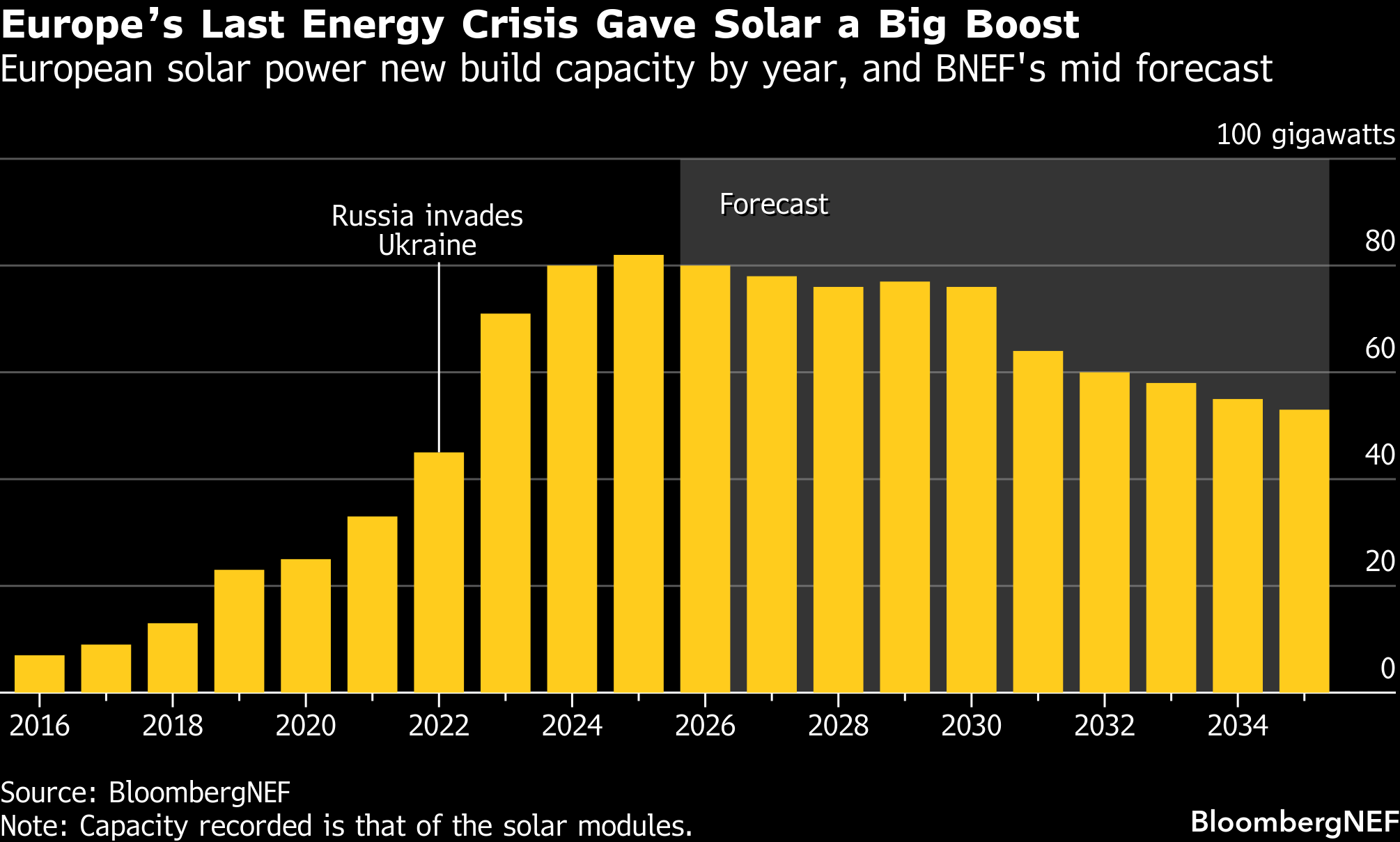

Then there’s the build-out of renewables that’s taken place in recent years. For example in Germany, which suffered a major blow in 2022 due to its reliance on Russian gas, solar power output is now helping to cap electricity prices even as the Iran war drives up global energy costs.

Alex Monk, a portfolio manager for the global resource equities team at Schroders, points out that the wind sector in particular has grown a lot more disciplined in setting contract terms “to allow for greater cost pass through and inflation protection so that profitability challenges do not occur again.”

Another key difference between now and 2022 is the impact of artificial intelligence, with demand for energy to power AI data centers bolstering renewables.

And with the geopolitical landscape arguably even more threatening now than in 2022, energy security has become an increasingly urgent goal. That means countries that successfully wean themselves off gas and oil imports face fewer external shocks to their economies.

“We view these moments of disruption in energy markets to be good for energy, full stop,” said Monk at Schroders. “In the short term we obviously see higher commodity prices and that’s helpful for conventional energy equities, but I think it also starts to bring to the back of everybody’s minds that question of energy security.”

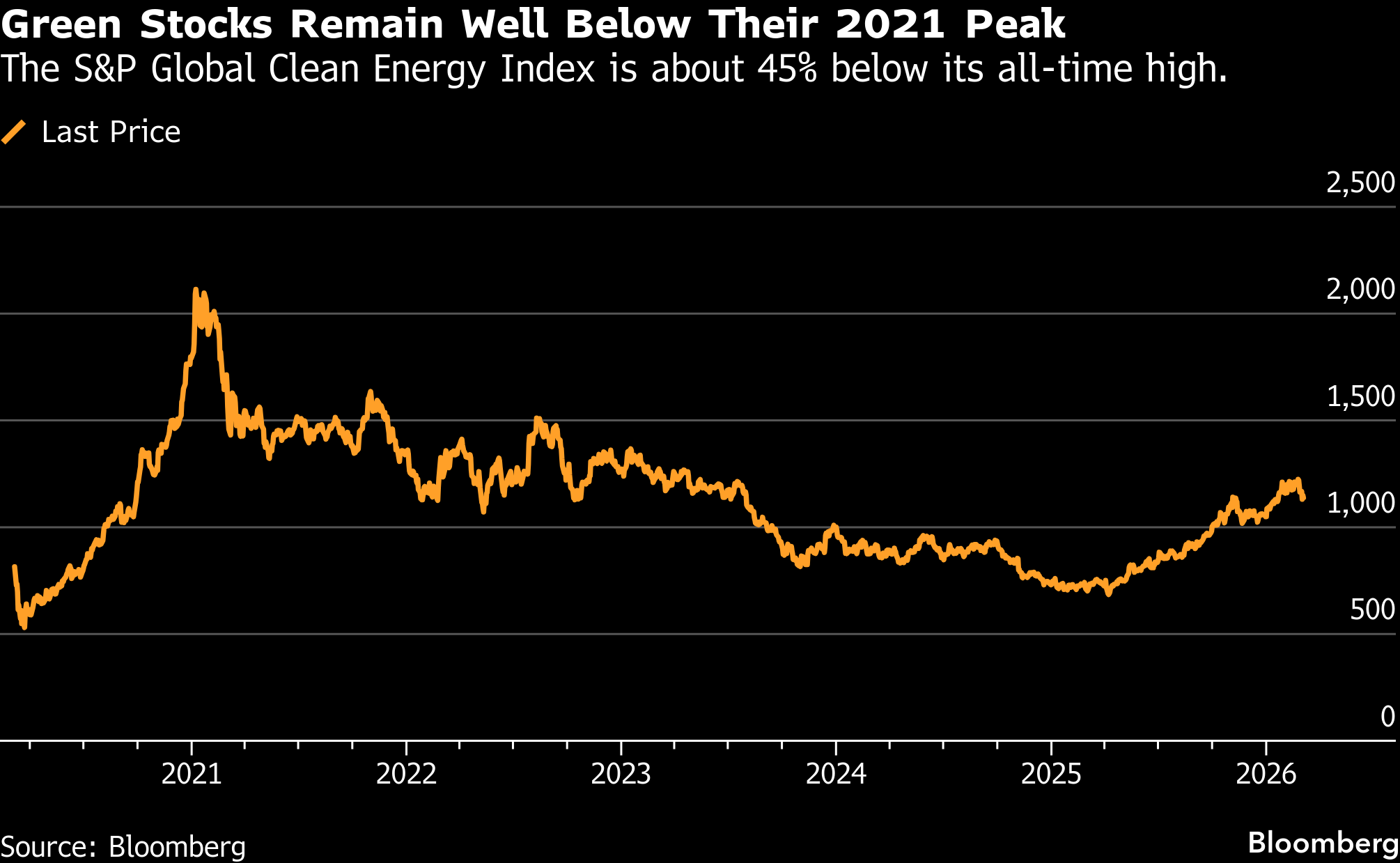

Many green investors are scarred from previous cycles of exuberance that devolved into punishing losses. That’s against a backdrop of US political attacks on the green sector and regulatory upheaval in Europe. But after an historic fall from grace that lasted through April last year, the sector has showed signs of defying the doom-sayers.

“What’s going on in the Middle East actually encourages a new capital cycle” of investments in renewables, Monk said. That’s “because people do need to start questioning that energy security, particularly with electricity demand continuing to grow.”

Much of that demand is coming from so-called hyperscalers, where investments in energy capacity to support AI data centers have emphasized low-carbon options.

“When we look back in 12 months’ time,” the question will be whether “the transformation that AI is reaping on our economy, or the missile attack on Iran will be more important for the shape of the economy over the next five years,” said Deirdre Cooper, head of sustainable equity at Ninety One Plc. “I would argue the former.”

The rise of AI as a tool of war should also guide energy investment decisions, according to Edward Lees, co-head of the environmental strategies group at BNP Paribas Asset Management in London.

“Of course we are going through a period of volatility,” he said. At the same time, “these military actions are now using AI, and all the kit is using chips, and hence energy,” which is “core to many areas we look at.” For that reason, BNP’s allocations to green assets remain “broadly intact” despite the onset of the Iran war, he said.

Europe’s energy transition has evolved from what used to be mainly an environmental agenda into a “core pillar of strategic autonomy,” according to a recent note to clients by Allianz Global Investors.

Christoph Berger, chief investment officer for equities in Europe at AllianzGI, says he and his team have “had intense discussions about portfolio positioning” since the Iran war erupted.

The conclusion was that what’s needed is “a re-emphasis of our existing positions” that tap into “ongoing trends that prevent us from being vulnerable to external supply shocks,” Berger said. That means doubling down on smart grids, smart meters, energy management, where “we have key technology providers in Europe.”

The backdrop of war “reminds us we must decentralize our power supply,” he said.

The comments feed into a broader trend among European investors to allocate funds in keeping with the bloc’s security goals. Money managers across the region have been piling into defense assets, strategic technology and energy as Europe navigates a growing list of geopolitical threats.

At AllianzGI, a “key conviction” is to pursue “a roadmap for European autonomy,” Berger said.

Of course, there are still plenty of unknowns ahead and Shah at Jefferies says there are obviously limits to the kinds of interest rate spikes that green companies can absorb.

So should the yield on the US 10-year bond go as high as 5%, “then there could be trouble,” he said.

©2026 Bloomberg L.P.