How a Company Collapse Is Denting Trust in Carbon Markets – Again

(Bloomberg) -- This year was supposed to be a turning point for carbon markets, with the United Nations’ long-delayed country-to-country trading system coming into force and airlines preparing to enter a mandatory program to offset their emissions.

But the high-profile collapse of a World Bank-backed clean-cooking company has delivered another blow to confidence in the market, which has been battered by credibility issues for years and, more recently, by a retreat on climate commitments by governments and companies.

Koko Networks Ltd., which sold cooking stoves and clean-burning ethanol to about 1.3 million households in Kenya, folded in January amid concerns it was issuing more carbon credits than its products warranted, a claim the company has denied.

The bankruptcy has had a ripple effect across projects selling carbon credits, companies buying them and the marketplaces on which those offsets are traded. Prices on Corsia, the marketplace for airlines where Koko was looking to sell its credits, fell as low as $12.25 from about $15 just before the firm’s collapse, according to data compiled by Bloomberg, and now sit at $12.85.

“The events of Koko have definitely created an undermining of confidence,” said Douglas Greenwell, commercial director and head of the carbon business at Burn, the world’s largest clean-cookstove developer and a seller of carbon credits.

Buyers have been unnerved by Koko’s failure to deliver credits they had been counting on and are reluctant to commit until there is more certainty, Greenwell said. He expects the softening of prices to be short term. “Corsia buyer demand [that] was emerging last year has not gone away, but it’s elongated,” he added. “Decision-making cycles have increased.”

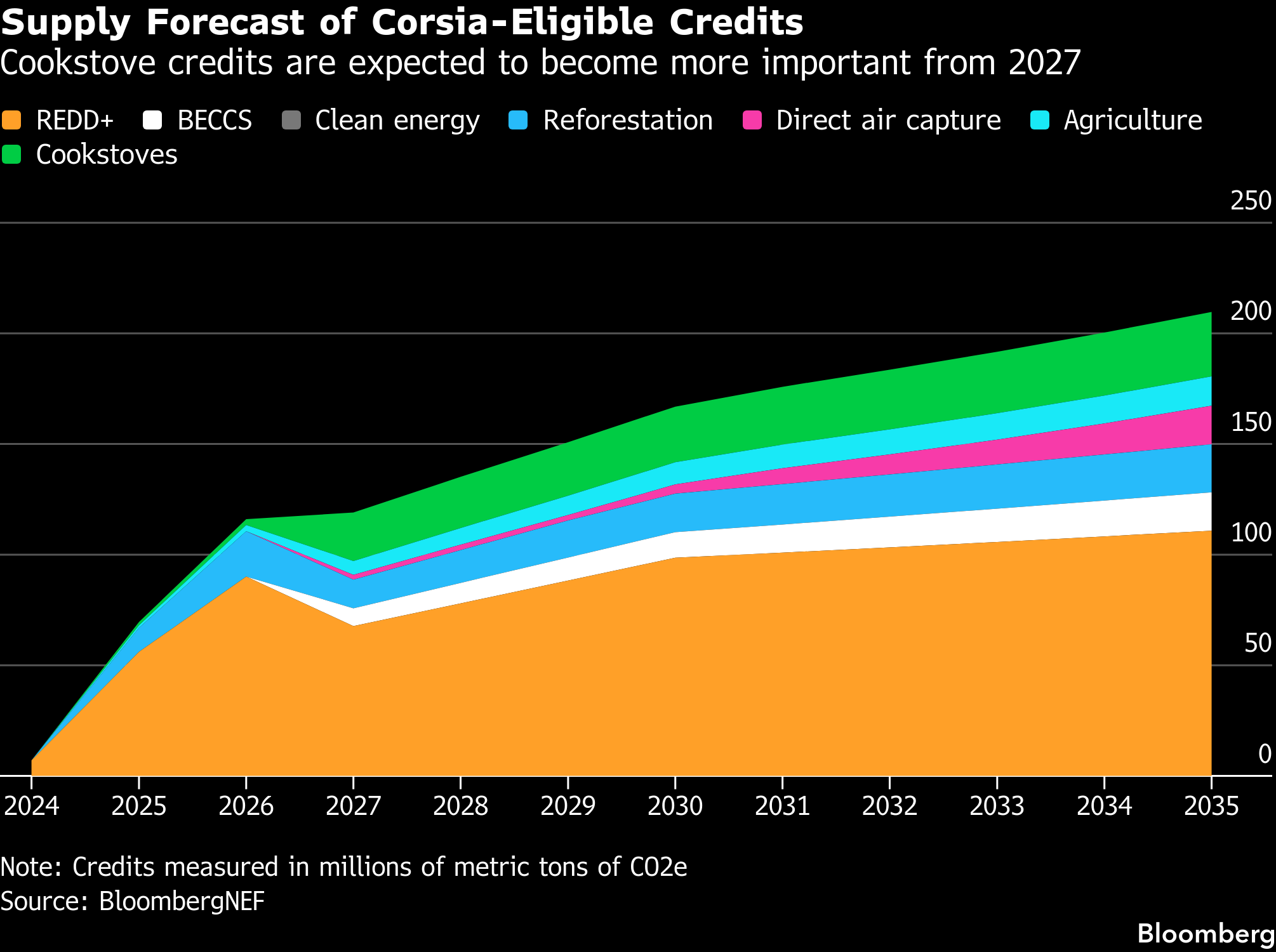

Carbon offsets have long been a Rorschach test among climate experts. Some carbon markets allow companies to offset their greenhouse gas emissions by purchasing credits from businesses whose activities reduce the production of pollutants. Each credit represents a ton of carbon dioxide; Koko generated credits by attempting to quantify the deforestation avoided by shifting its customers away from cooking over wood and charcoal fires.

Proponents argue that carbon credits channel crucial funds from companies and rich governments to poorer nations and communities, incentivizing the protection of important natural environments. Others argue that because the vast majority of projects focus on avoided emissions — trees that aren’t cut down or fossil fuels that aren’t burned — the sector is prone to unreliable carbon math or even fraud.

“Given all the doubts, issues, flaws, conflicts of interest in the market, lack of clarity on financial flows, it can’t be used for offsetting or to claim a company’s or country’s emissions are lower,” said Jonathan Crook, global carbon markets lead at nonprofit Carbon Market Watch. “That said, there can still be value from some carbon-crediting projects.”

Projects must result in emissions reductions — known as additionality — and the broader market needs to improve its methodologies and ensure there is enough oversight, he said.

In the longer term, that means supply is a bigger issue than demand.

“Any time there are concerns about a prominent project’s ability to deliver carbon removal, that hurts the overall reputation of the sector,” said Kyle Harrison, head of sustainability research at BloombergNEF. “It’s a fairly persistent trend with projects around the world.”

The UN’s International Civil Aviation Organization, which oversees Corsia, declined to comment on whether Koko’s collapse had impacted prices. Still, high-quality carbon credits of the sort Corsia requires are hard to come by and Koko’s collapse has tightened supply even further. Corsia launched in 2021 on a voluntary basis, but most airlines will be required to comply from 2027.

“The process for approving Corsia-eligible projects is time-intensive and only a handful of projects are eligible now,” Harrison said. Because the market is nascent and not very liquid, removing an advanced project like Koko from the pipeline “will have a big impact on fundamentals.” But demand will bounce back, he added, because aviation companies will ultimately be required to buy Corsia-eligible credits.

The ICAO is “actively facilitating the assessment of more emissions unit programmes to enhance the supply of Corsia eligible emissions units,” a spokesperson for the agency wrote in an emailed reply to questions. The ICAO said it doesn’t speculate on potential future developments or comment on matters pertaining to specific external parties or member states. However, it did call on governments in countries where Corsia-eligible projects take place to issue the necessary permits to increase availability.

Koko attributed its bankruptcy to the Kenyan government’s failure to issue permits known as letters of authorization, which the government had agreed to provide as part of an investment pact. Rivals, including Burn, have questioned whether the agreement was ironclad, saying that, unlike several other African governments, Kenya has shown little appetite for issuing LOAs for biomass-based credits. The Kenyan government didn’t respond to a request for comment.

Suppliers, governments and buyers are at risk of deadlock, said Burn’s Greenwell, unless parties become willing to “oil the market.” Cooking companies, including Burn, DelAgua Group and Hestian Innovation, are starting to deliver credits to carbon markets now. “But that’s only going to continue if we, as developers, keep being confident the buyers are there to buy,” he said.

“A lot of market players were banking on [Koko] receiving letters of authorization to be traded via Corsia at premium prices,” said BNEF’s Layla Khanfar.

Companies are starting to find creative ways to bridge the market’s gaps. In March, Sistema.bio, a provider of biodigesters for smallholder farmers in Africa and Asia, launched a $53 million investment vehicle for pre-financing biogas projects that will generate carbon credits.

Backed by BNP Paribas Asset Management’s alternative investment platform, the Shell Foundation and development finance institution British International Investment, the funding facility is designed to deliver credits to buyers through multi-year purchase agreements.

“We saw a clear mismatch in investment,” said Alex Eaton, chief executive officer at Sistema.bio. “There were larger investors that wanted to put money into carbon markets but didn’t want to take project risk, and others who wanted to support project developers, startups and climate technology, but were less clear about the carbon-market risk.”

A rush to secure supply risks undermining one of the most crucial goals for carbon markets — to make reducing hard-to-abate emissions affordable for developing countries, said Carbon Market Watch’s Crook. Emissions from energy-intensive sectors such as transport and heavy industry are considered particularly difficult to prevent.

Ultimately, countries participating in carbon markets need to make sure they’re getting something out of them, he said.

“The real risk right now is there’s a lot of pressure on governments to approve things and especially things that are not very expensive, leaving them with having to do the more expensive mitigation themselves,” Crook said. “There is a need for more caution for governments as to how they're going to approach these markets.”

©2026 Bloomberg L.P.