EQT Warns of Exit Risks for Alternative Energy Assets Held by PE

(Bloomberg) -- EQT AB, Europe’s biggest private equity firm, says the path to exiting investments in clean-energy developers and operators faces a growing number of hurdles.

In many cases, such assets have become too big to be absorbed by the kinds of private or industrial buyers PE firms traditionally turn to when looking for an exit, according to Alex Darden, the head of EQT’s infrastructure investment for the Americas.

Initial public offerings would be the natural next step, but because such companies often still have negative cash flows and complex risk profiles, the IPO route so far “hasn’t been developed enough” for PE investors to feel they can easily tap it, he said in an interview.

“The IPO market remains a question market,” Darden said.

And without a clearer path to exiting holdings, PE fund managers are “going to run the risk of people not being able to invest capital in the same way in the private markets that they’re currently doing,” he said. At the same time, EQT will continue bankrolling clean energy firms and “finding creative ways to monetize” such deals, he added.

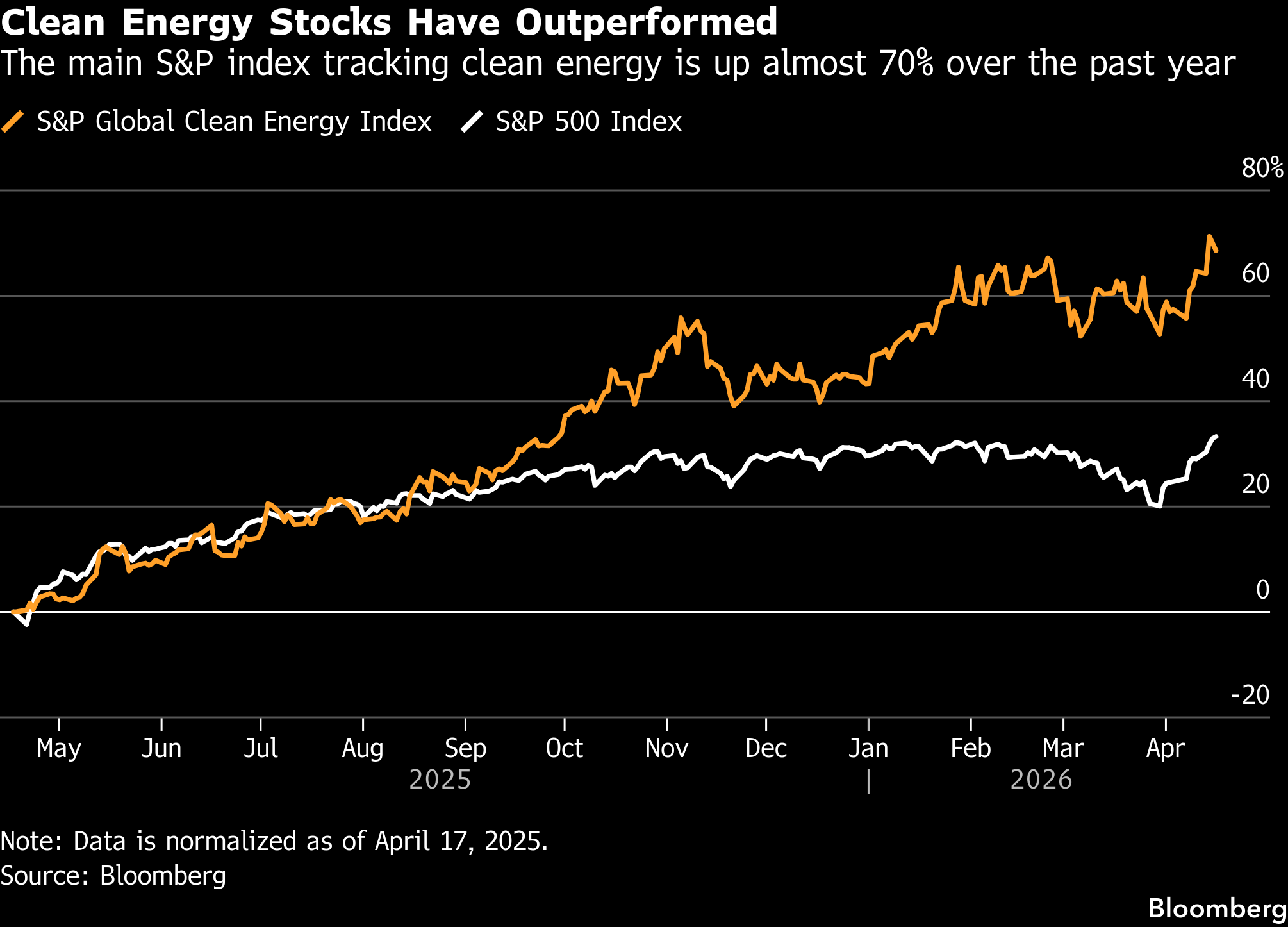

The comments touch on a divide playing out in the market for clean tech. Though the sector has enjoyed an overall rebound — with the main S&P index for such companies gaining almost 70% over the past year — most of that rally has rested on the performance of equipment makers like Nordex SE and SMA Solar Technology AG.

Energy developers and operators, meanwhile, have seen a different trajectory, often because their fate is tied to ongoing client contracts and continual disruptions in the regulatory and legislative landscape. Examples include Altus Power Inc, a major US commercial-scale solar operator that was taken private last year after its market value plunged by about two-thirds from a 2022 high, in large part due to delays in getting projects up and running.

“There still are active exit routes and exit opportunities, and there’s still a very active buyer universe,” Darden said. However, “the challenge that is starting to develop on the private side is that many of these companies have scaled very large.”

He says at the beginning of the decade, many clean energy developers owned about 1 or 2 gigawatts worth of operating assets, a figure that’s now soared to as much as 8 gigawatts. “It creates a dynamic where you’ve got to look for potentially multiple buyers to partner up to be able to buy these companies.”

Others have made similar observations. Joost Bergsma, global head of clean energy at Nuveen Infrastructure, said opportunities to exit investments is still “good,” but not at the same level seen four or five years ago, when there was “really a lot of interest.” What’s more, “interest is quite selective” now amid an atmosphere that’s become “really quite cautious,” he said.

Any disruption to investments in alternative energy would risk limiting future supply as the world struggles to adapt to the fallout of the Iran war. The failure to reach a lasting truce has injected extreme volatility into oil and gas markets, threatening to trigger a wave of inflation and higher interest rates as the conflict drags on.

As a result, investment banks like Jefferies have predicted that demand for clean-energy assets will soar as governments and regular households look for alternatives. And firms including Brookfield Asset Management, Eurazeo SE and Tikehau Capital say their green portfolios are currently thriving.

“What we’re seeing on the ground, it’s honestly never been better than it is today,” Natalie Adomait, chief operating officer for Brookfield’s energy group, said in a recent interview.

Against that backdrop, there continue to be opportunities for financial professionals capable of navigating the current hurdles, Darden said.

EQT is “very interested in trying to understand how companies within this sector can be positioned effectively for public markets, from a size standpoint, from a cash standpoint,” he said, declining to offer specifics.

In March, EQT teamed up with BlackRock Inc.’s Global Infrastructure Partners to acquire AES Corp., a US firm which generates the majority of its power from renewable energy. That deal valued AES at about $10.7 billion.

Other private capital firms are also signaling they continue to be interested in investing in alternative energy assets, with KKR & Co. and Brookfield Asset Management among those to have indicated that they’re scouting for possible acquisitions.

But without clear exit routes, investor demand may start to fade, Darden said.

“If you don’t have the public markets and the public capital capability, you run a risk of slowing down the overall development of the industry, especially as the industry is now hitting a very high growth rate and a very steep trajectory of growth over the next decade,” he said.

Ultimately, demand for clean energy developers needs to spread beyond private markets, Darden said. “Or else everything is going to grind to a halt.”

(Adds comment in fourth paragraph.)

©2026 Bloomberg L.P.