Oil Extends Decline as Trump Says ‘Great Progress’ in Iran Talks

(Bloomberg) -- Oil fell a second day as US President Donald Trump said “Great Progress” has been made on a final agreement to end the war with Iran.

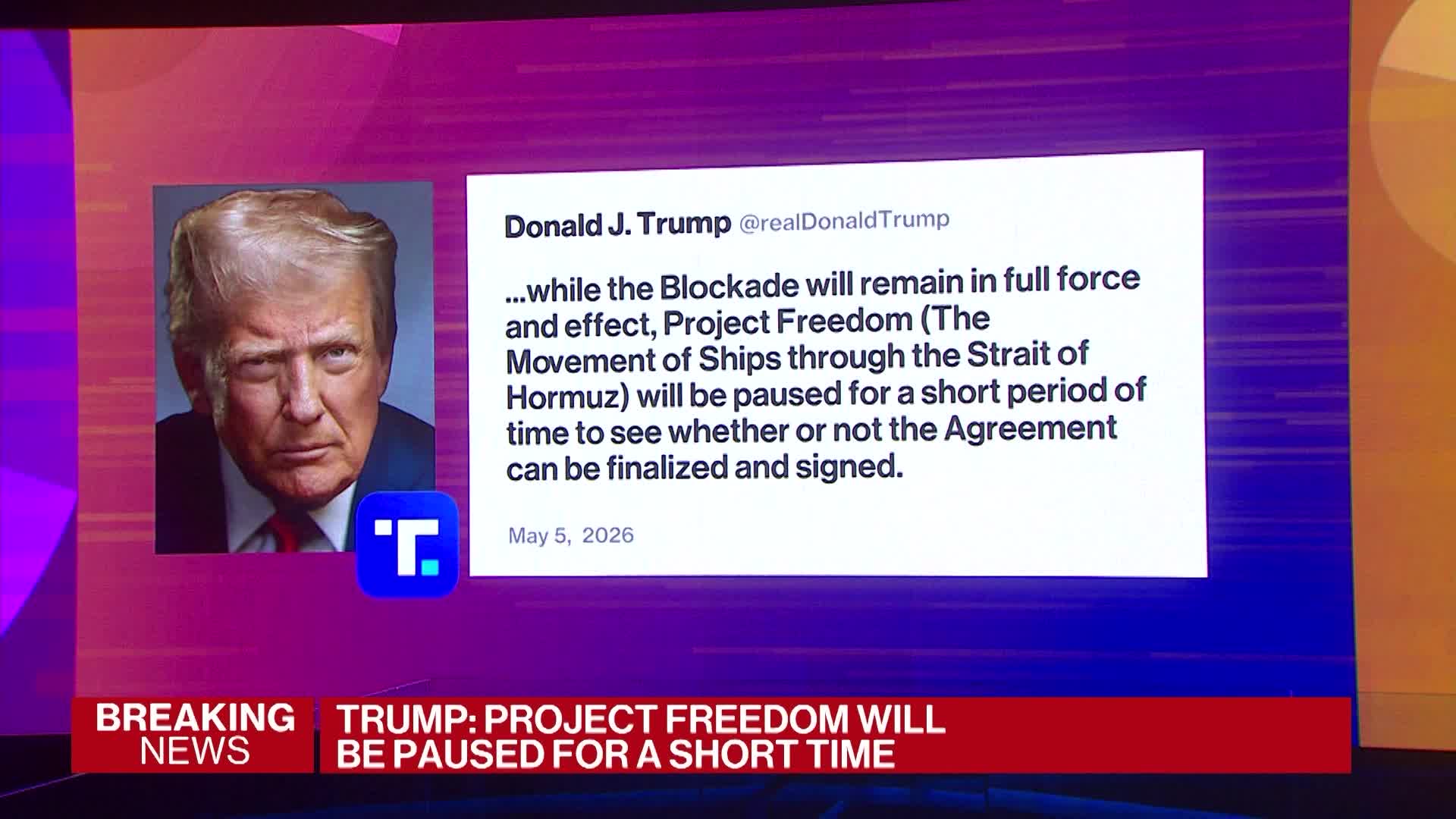

Brent dropped toward $108 a barrel after sliding 4% on Tuesday, while West Texas Intermediate was near $100. US efforts to move ships through the Strait of Hormuz will be paused, but a naval blockade will remain in place, Trump said in a Truth Social post.

The global benchmark has climbed by about 50% since the conflict started at the end of February, cutting off hundreds of millions of barrels of Gulf oil from global markets. Flows through the chokepoint are now constrained by a double blockade, with Tehran obstructing shipping while the US is stopping vessels from accessing Iranian ports.

Earlier, Secretary of State Marco Rubio told reporters at the White House that “Operation Epic Fury is concluded,” 66 days after the US and Israel began bombing Iran. “We achieved the objectives of that operation,” he said.

On Tuesday, Washington played down the prospect of a return to active war, with Defense Secretary Pete Hegseth confirming the truce that began just under a month ago is still in place. Meanwhile, General Dan Caine, the chairman of the Joint Chiefs of Staff, said attacks by Tehran on vessels in the Gulf and the United Arab Emirates didn’t constitute a breach of a ceasefire.

The shutdown around Hormuz has left more than 1,550 commercial vessels, carrying some 22,000 sailors, trapped in the Persian Gulf, Caine said.

“Even if we see some deescalation headlines, the supply recovery is inherently delayed,” said Dilin Wu, a research strategist covering cross-asset markets at Pepperstone Group. “This is not a switch you can just flip: You still see limited oil shipment through the strait and it still needs time for stranded tankers to be rerouted, for the insurance market to reprice risk and for production to ramp back up,” she said.

In the US, industry data showed crude inventories fell 8.1 million barrels last week, which would be the biggest draw since mid-February if confirmed by official data due later Wednesday.

“We’re holding the pattern from rally to profit-taking each day,” said Carl Larry, an oil and gas analyst at Enverus. “Markets may take it in stride but irrational exuberance usually gets the best of the market. Draws bring all the bulls to the yard.”

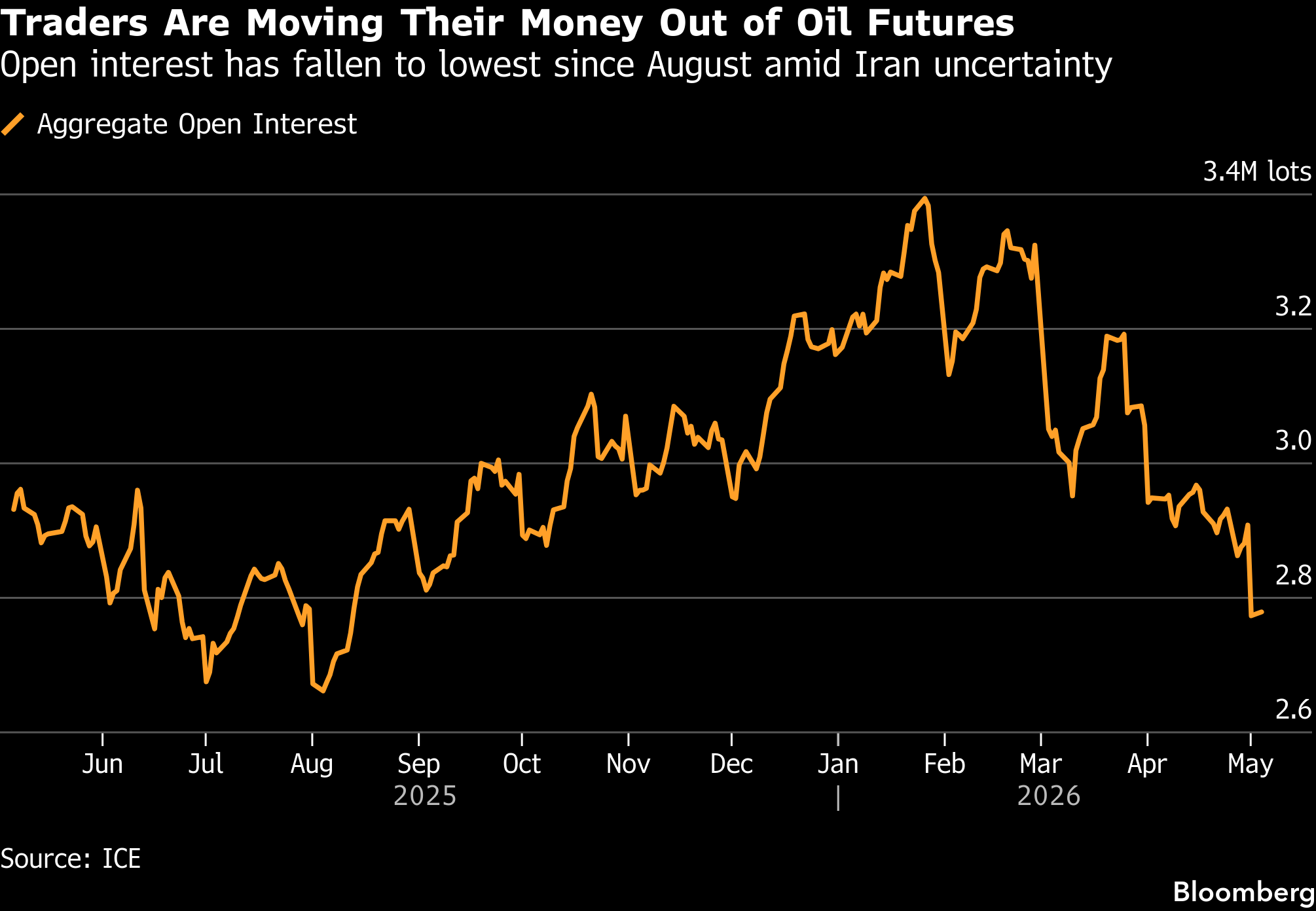

Oil has seen wild price swings since the war started, prompting traders to move to the sidelines to avoid extreme volatility. Aggregate open interest in Brent has dropped to its lowest level since August.

Meanwhile, Saudi Arabia cut the price of its main oil grade for Asia next month from a record-high in May. It remained elevated as the hostilities in the Middle East continue to severely disrupt supplies.

©2026 Bloomberg L.P.