Trump Planned for Big Oil’s Global Dominance. Then He Went to War With Iran

(Bloomberg) -- From capturing Venezuela’s president to attacking Europe’s methane rules, President Donald Trump had created a slipstream for his oil-industry backers to expand production of fossil fuels and boost profits.

But his war against Iran, now entering its fourth week, is threatening to derail some of their longer-term plans, even as they benefit from the recent surge in crude and natural gas prices.

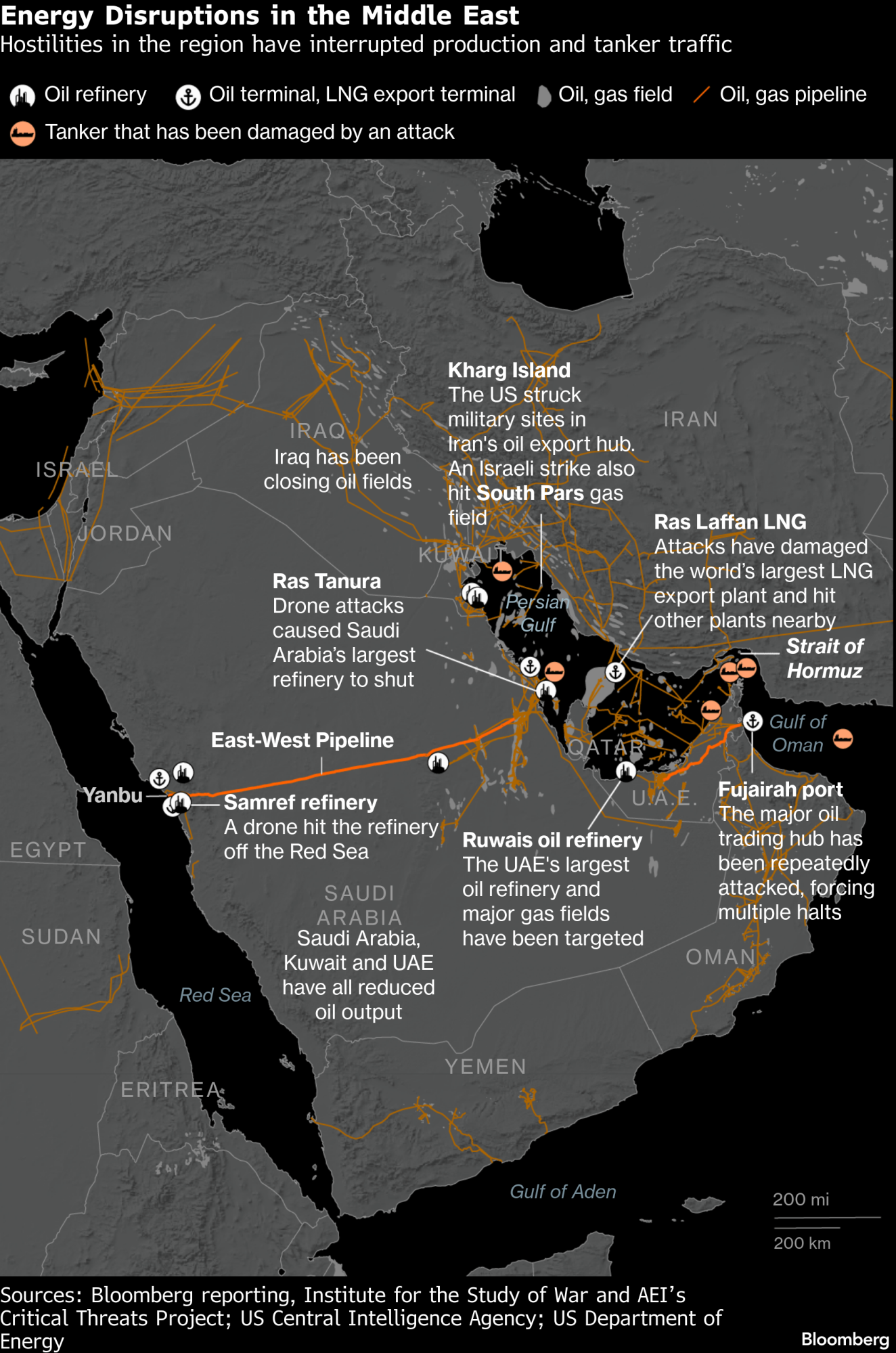

The conflict — which has killed more than 4,200 people across the Middle East — has all but halted tanker traffic through the vital Strait of Hormuz and curbed oil and gas output, causing chaos in a region energy executives had hoped Trump would help open up for foreign investment. Overseas expansion now carries heightened risk and higher costs — a development that will be front of mind for oil bosses as they gather in Houston for the annual CERAWeek by S&P Global conference this week.

“There’s going to be a security premium” baked into oil prices once the war in Iran is over, Dan Yergin, vice chairman of S&P Global and founder of the conference, said in an interview. “I don’t think after this we’re going to return to where we were before.”

Until recently, Trump’s aggressive foreign policy and support for fossil fuels — which included behind-the-scenes backing for US energy companies looking to expand overseas — appeared to benefit Big Oil.

His administration’s efforts have helped companies including Exxon Mobil Corp., Chevron Corp. and Shell Plc regain access to countries like Venezuela, Iraq and Libya, home to some of the world’s biggest reserves. While many of these expansion plans are in their infancy, they have become priorities for oil executives looking to restock their portfolios at a time when US shale production growth is slowing and the International Energy Agency expects crude consumption to continue rising through 2050.

Since the war on Iran started, the Trump administration has had in-person meetings with executives from Exxon and Chevron to discuss ways to lower oil prices and ramp up supply, according to a White House official. Though the administration has moved forward with some of those options, including plans to release oil from US strategic reserves and temporarily waiving a century-old shipping mandate to lower transportation costs, others are not on the horizon.

Growth is a key strategic priority for Exxon.

“We’ve had a clear view that global energy demand is going to continue to grow and that oil and gas is going to continue to play a very significant role,” Dan Ammann, Exxon’s upstream president, said in an interview last month before the war in Iran. “The challenge is to grow in a capital-efficient way, in a responsible way and to do that in partnership with resource owners around the world.”

But the spiraling conflict, which Trump says is crucial for long-term stability in the Middle East, throws these prospects into doubt. Attacks on infrastructure and production shutdowns at some of the world’s most important oil and gas fields in Iraq, Kuwait and Qatar underscore the risk of sinking billions of dollars of capital into new investments in the region. Though crude prices are up more than 50% since the war began, the market has been exceptionally volatile.

“Oil companies think in multidecade commitments but the risk in some of these countries is higher today than it was a few weeks ago,” said Noah Barrett, a research analyst at Janus Henderson, which manages about $493 billion. “Wild oscillations in price without a clear view of US strategy for the war doesn’t give investors confidence.”

So far, energy executives have said little publicly about how the war in Iran has shifted their plans. They may be wary of drawing Trump’s ire. When Exxon CEO Darren Woods called Venezuela “uninvestable” in January, Trump responded by saying he was inclined to shut the oil giant out of the South American country altogether.

For much of the last 15 years the oil industry’s focus has been on the US, where the explosion of output from shale basins made America the world’s biggest producer and essentially energy independent for the first time since the 1950s. But with some of the best shale drilling locations already tapped out after years of breakneck growth, companies are beginning to look to new markets.

Trump has proved to be a key partner in this effort, despite a rocky start due to tariffs and the administration’s fixation on low crude prices.

The removal of Venezuelan strongman Nicolás Maduro creates a path toward opening up the world’s largest oil reserves. The pushback against the European Union’s move to curb methane, a powerful greenhouse gas, could remove a key hurdle to US natural gas exports. Financial and political backing are helping to take fracking global.

American officials actively supported Exxon and Chevron as they negotiated exploration licenses in major-producing OPEC nations Iraq, Libya, Algeria, Azerbaijan and Kazakhstan over the past year. Just last month, Chevron signed preliminary agreements to negotiate with Iraq’s national oil company about taking over the country’s second-largest oil complex from Russian producer Lukoil PJSC after the Russian producer was hit with sanctions — slapped on by Trump.

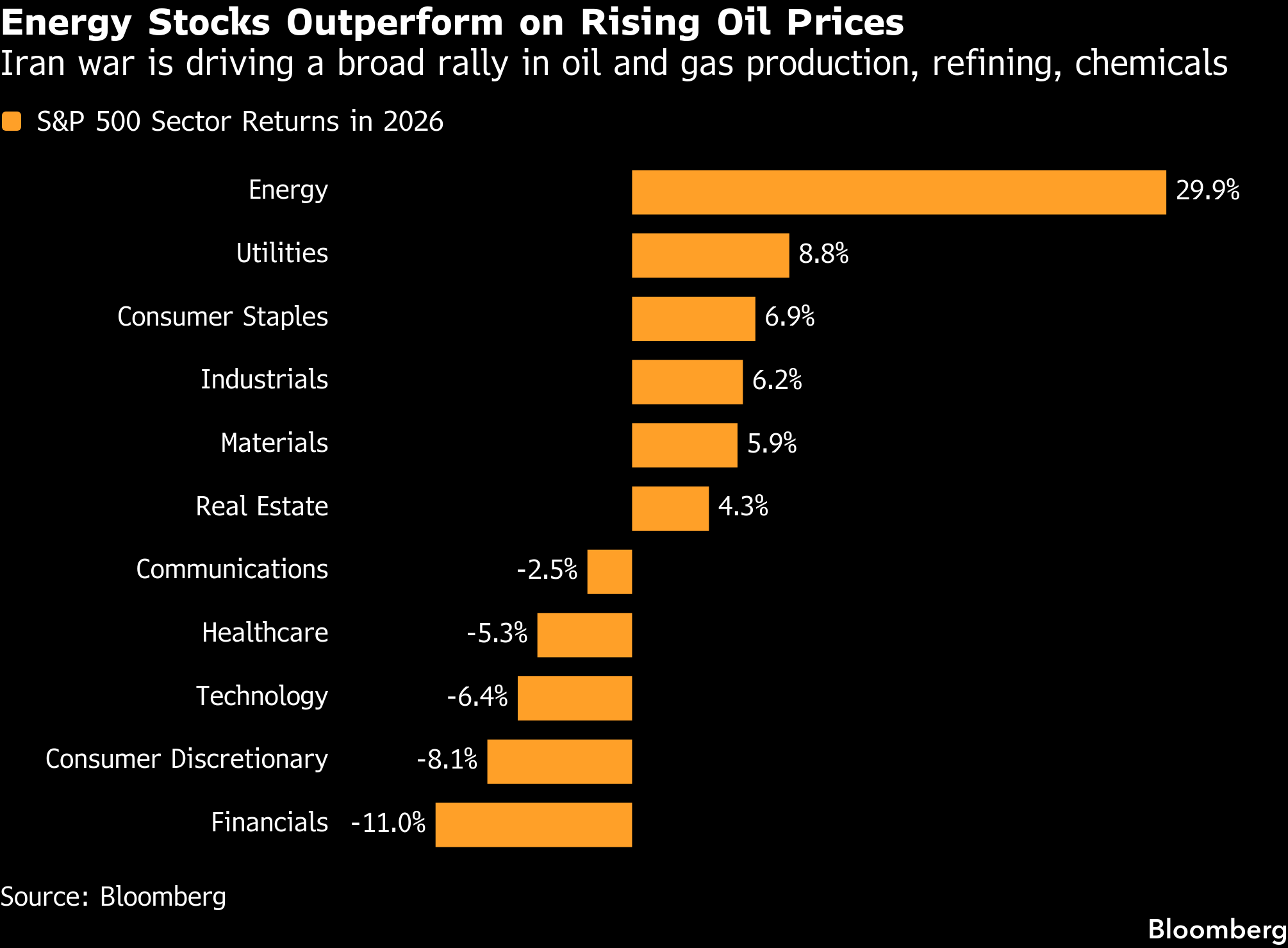

Boosted by rising oil and liquefied natural gas prices, energy is the best performing sector in the S&P 500 Index this year. Exxon, Chevron and Shell are trading at all-time highs after rising more than 25% this year, compared to the wider market’s drop of about 4%.

But risks abound. Exxon and and French oil major TotalEnergies SE have about 10% of their cash flow from operations exposed to curtailed production — mainly liquefied natural gas in Qatar — in the Middle East, according to analysts at TD Cowen. Qatar's Ras Laffan liquefied natural gas complex, in which Exxon is a joint-venture partner, has suffered extensive damage as a result of Iranian missile attacks that could take as long as five years to repair, Qatar Energy said Thursday. Shell's gas-to-liquids plant in the same complex was also damaged.

And with OPEC’s five largest members now affected by a conflict that is blocking transportation for 20% of the world’s oil and LNG production, the stability and free-flowing trade needed for Big Oil to commit billion of dollars to new investments appear to be distant prospects.

“Risk premiums will be higher for production out of this region” even if the Strait of Hormuz is reopened soon, said Arjun Murti, a partner at Veriten, a Houston-based energy research and advisory firm. “This will favor the next leg of shale, the next leg of Canadian oil sands, exploration outside of the Middle East.”

The propensity of Trump to pressure companies to invest in difficult environments, like he did with Venezuela, further impedes long-term investment by making it more difficult for companies to invest based on market signals alone, according to Karen Young, a senior research scholar at Columbia University’s Center on Global Energy Policy.

“It actually complicates the market logic, and the victory of capitalism,” she said.

The war with Iran will be a major topic at CERAWeek, where the heads of Shell, ConocoPhillips, Kuwait Petroleum Corp., and dozens of others are scheduled to speak. Energy Secretary Wright is among the first scheduled to present on Monday, followed by Chevron CEO Mike Wirth.

The White House, which maintains the Strait of Hormuz will be open soon, has so far rejected the idea that its actions in Iran will hurt US energy interests over the long term.

“Ultimately the energy industry is going to benefit from the president’s actions with respect to Iran, because Iran will no longer be controlling the Strait of Hormuz and restricting the free flow of energy,” spokeswoman Karoline Leavitt said earlier this month.

But the longer Brent crude trades above $100 a barrel as a result of the Strait’s effective closure, the more concern investors will have over the security of supply from the Middle East.

“There hasn’t been a disruption of this scale of ferocity before,” said Yergin of S&P Global. “The question is who pays: producers, consumers or governments?”

©2026 Bloomberg L.P.