Fear Gauge Shows India Stock Strain as Iran Shock Eases in Asia

(Bloomberg) -- Stock-market volatility in India is staying elevated unlike in the rest of Asia, signaling deeper investor unease about the nation’s energy exposure, high valuations and renewed focus on corporate governance troubles.

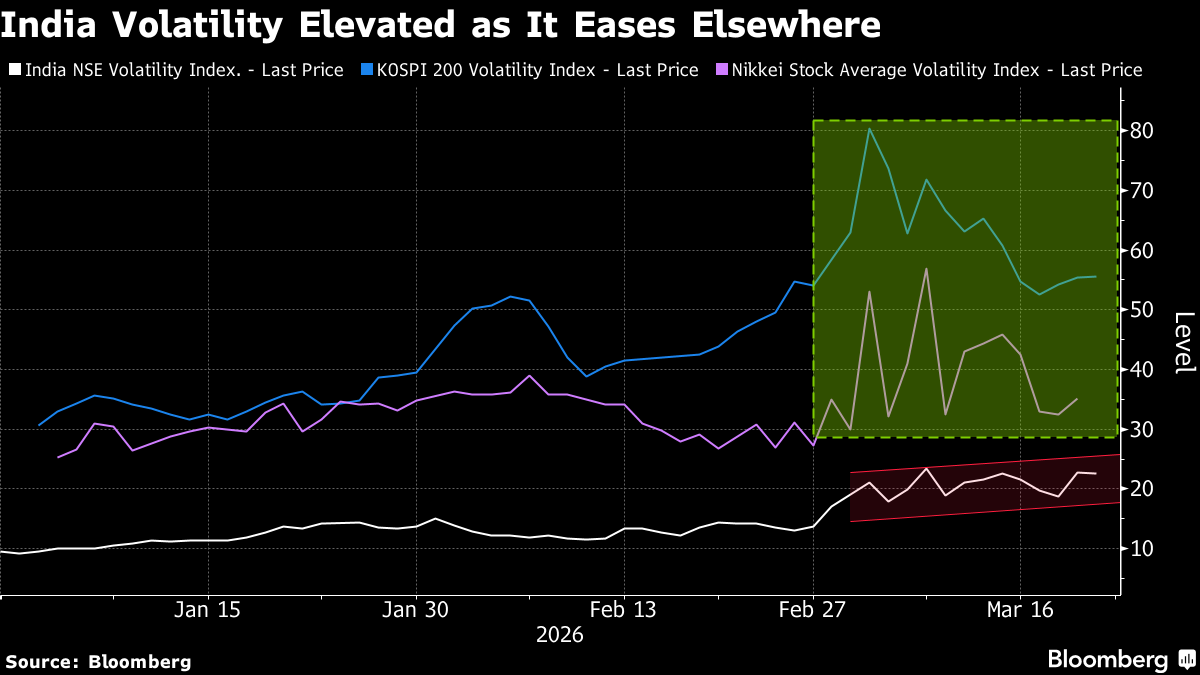

India’s volatility gauge remains near its March 9 peak, which was the highest since June 2024. Similar measures for Japan and South Korea, countries that rely heavily on fuel shipped through the Strait of Hormuz, have dropped from their respective Iran war–driven highs. The Cboe Volatility Index has also eased.

The divergence suggests India’s risk premium is turning stickier with the energy shock hitting the economy. Even before the conflict, India faced high valuations, the risk of AI disruption without notable chipmakers, and currency weakness. The selloff has pushed its stocks benchmark near levels last seen during the market turmoil after the US tariff rollout a year ago, just as governance concerns erupted at the nation’s biggest private-sector bank.

“Elevated oil prices, rupee at record lows, sustained foreign outflows, and high valuations together form a challenging macro backdrop, for equities to deliver immediately,” said Gary Dugan, chief executive officer at the Global CIO Office. “Even if the geopolitical temperature cools, there is still meaningful downside if domestic concerns linger.”

The NSE Nifty 50 Index has lost 11% this year, compared with a gain of about 5% gain in the MSCI Asia-Pacific Index. Among equity gauges in countries exposed to the Iran energy shock, Korea’s Kospi is up 37%, while Japan’s Nikkei 225 is up 6%.

“India’s volatility reflects more than geopolitics,” said Song Zhe, an investment specialist for emerging-market equities at BNP Paribas Asset Management. “India needs to win back attention on its own merits — better earnings breadth, a steadier rupee, lower oil anxiety and valuations that are compelling rather than merely less expensive.”

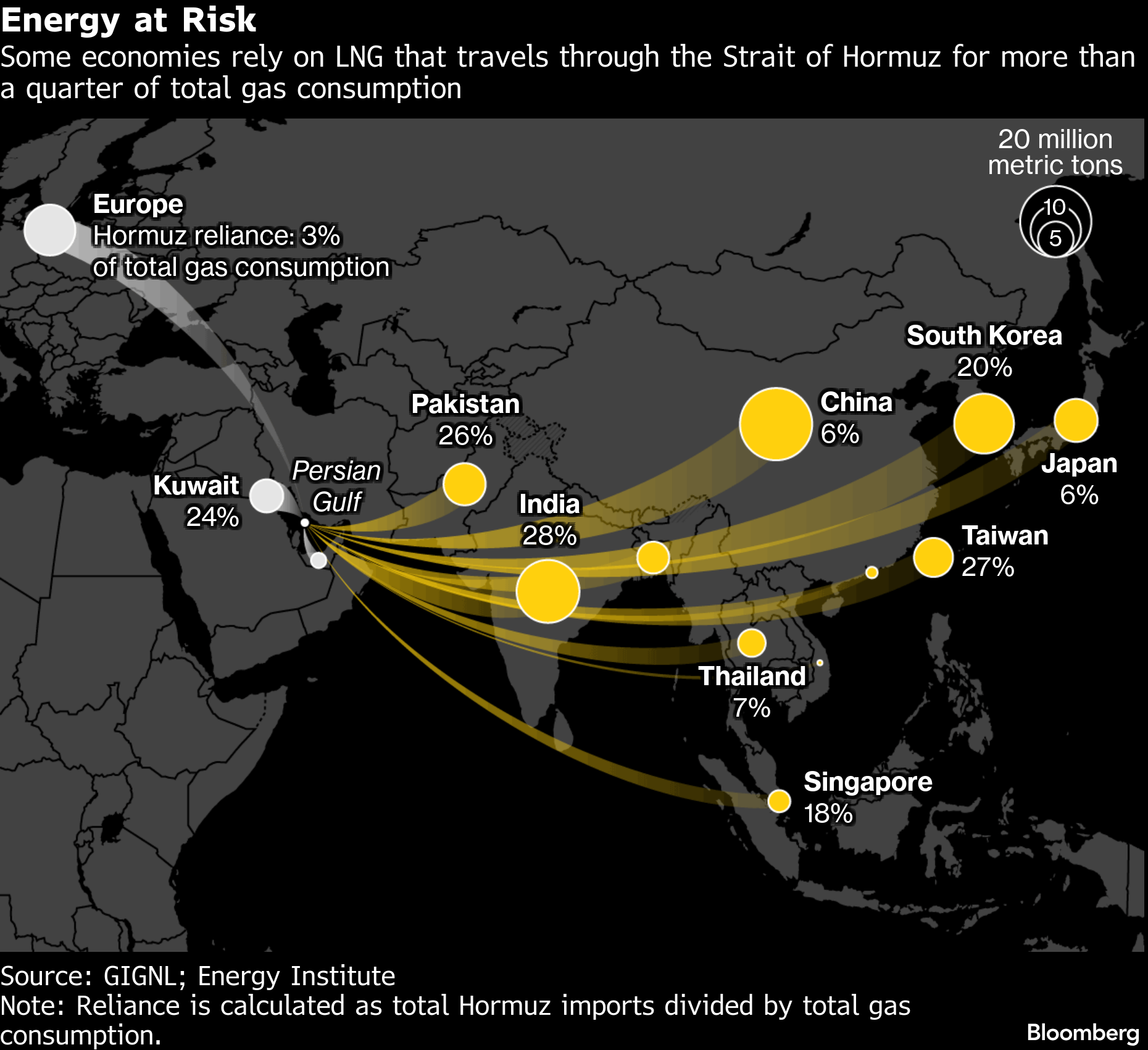

The energy exposure is the most immediate problem. India imports roughly 90% of its crude oil and nearly 50% of its liquefied petroleum gas, with about half of that crude and over three-quarters of the LPG transiting the Strait of Hormuz, which Iran has effectively shut.

In addition, the rupee’s slide is amplifying the impact, with the currency weakening to a record against the dollar. Foreign investors pulled almost $7.8 billion from Indian equities in March alone as the central bank’s intervention was unable to fully arrest the move.

The war is worsening India’s pre-existing issues, and “there are multiple macro factors that can derail for India” with rupee depreciation being the biggest risk, said Rita Tahilramani, an investment director at Aberdeen Investments.

Data from EPFR, a provider of metrics on fund flows and asset allocations, also underscores the positioning shift. In the week ending March 11, redemptions in funds dedicated to India were the largest since EPFR started tracking the group in 2000, eclipsing the previous record set in 2008 when the great financial crisis was roiling global asset markets, the data provider said in a note dated March 17.

On top of the existing sources of weakness, governance concerns have recently reemerged as a drag on the country’s equities. The chairman of India’s biggest private-sector lender, HDFC Bank, resigned over ethical issues, sparking a fresh market rout.

And underscoring the valuation concerns, the MSCI India index trades at a forward price-to-earnings ratio of about 19 times, compared with the emerging market average of 12 times.

“Volatility trends suggest India needs more than the conflict to end for sentiment to improve,” said Charu Chanana, chief investment strategist at Saxo Markets. “This is an ugly stack of risks, and rupee weakness is adding another layer of strain.”

©2026 Bloomberg L.P.