Hedge Funds, Tech Spur Texas Wealth Boom as California Fades

(Bloomberg) -- Big Tech is flocking to Austin. Big Finance is expanding in Dallas. Houston, the epicenter of the U.S. energy industry, is diversifying away from Big Oil.

Florida may be the destination of choice for A-list money managers looking to flee Wall Street. But in the post-pandemic economy, Texas is rising, welcoming a rush of talented, wealthy people from California, New York and Illinois with the lure of lower taxes, luxury suburbs and opportunities to invest their cash -- even as state lawmakers cast a wary eye at their potential blue-state politics.

In the last year, Tesla Inc. broke ground on a pickup-truck factory in Austin, and Oracle Corp. said it would shift its headquarters to the Texas capital. Hewlett Packard Enterprise Co. announced it was moving to the Houston area. Charles Schwab Corp. left San Francisco for the affluent Dallas suburb of Westlake, where Fidelity already has a campus. Vanguard plans to open an office in the area early next year.

And hedge funds are sprouting up or expanding all over Dallas. Izzy Englander’s Millennium Management, which has had offices in Texas since 2016, is backing a new fund, Meridiem Capital Partners, that’s expected to start trading in the second half of this year with $1.5 billion. Canyon Partners, which manages $24 billion, should have 55 employees in town by year end.

“A change of scenery sometimes is a great way to energize an organization, and Texas is clearly a very, very business friendly state,” Canyon co-CEO Josh Friedman said in an interview with Bloomberg TV. “Dallas has a particularly good base, I think, of very sophisticated families and it’s a good community intellectually in which to run a business.”

Cinctive Capital Management opened an office in Dallas this year with capacity for about 20 people. The fund, which manages about $1 billion, is expanding its Texas operation believing there are talented managers in the state that might be overlooked by other firms. Avidity Partners has more than doubled its footprint in the state since it began in 2019, and its assets have swelled to $4 billion. All of these moves are according to people familiar with each fund’s plans.

Tesla’s Gigafactory under construction in Austin.

Photographer: RoschetzkyIstockPhoto/iStock/Getty Images

A lack of income tax is only part of the draw. Housing is relatively affordable. The health care system in Houston and other cities feature some of the best hospitals in the country. In addition to a warmer climate, plentiful restaurants, activities for families and lots of space to roam, job creation in the state has served as a magnet.

“Employment growth has typically been twice the national average over the years,” said Pia Orrenius, an economist at the Federal Reserve Bank of Dallas. “And when you compare it with places like California and New York, the cost of living is still substantially lower, even though it’s starting to rise.”

Texas has long used cash grants and local-tax incentives to coax companies to relocate. Now, a slew of growth-minded local businesses are attracting money to an economy that state leaders say would be the world’s ninth largest if Texas were an independent country.

“Covid really just accelerated it,” said Andrew Brock, the Austin-based head of Private Bank for Central Texas. “People are coming here to invest. They’re coming here because they believe there are opportunities to deploy capital.”

Family Offices, Private Equity

Brock says Austin is benefiting from an influx of family offices and private equity firms looking to scale up growing businesses alongside established giants as Dell Technologies Inc. and more recent successes such as Yeti Holdings Inc.

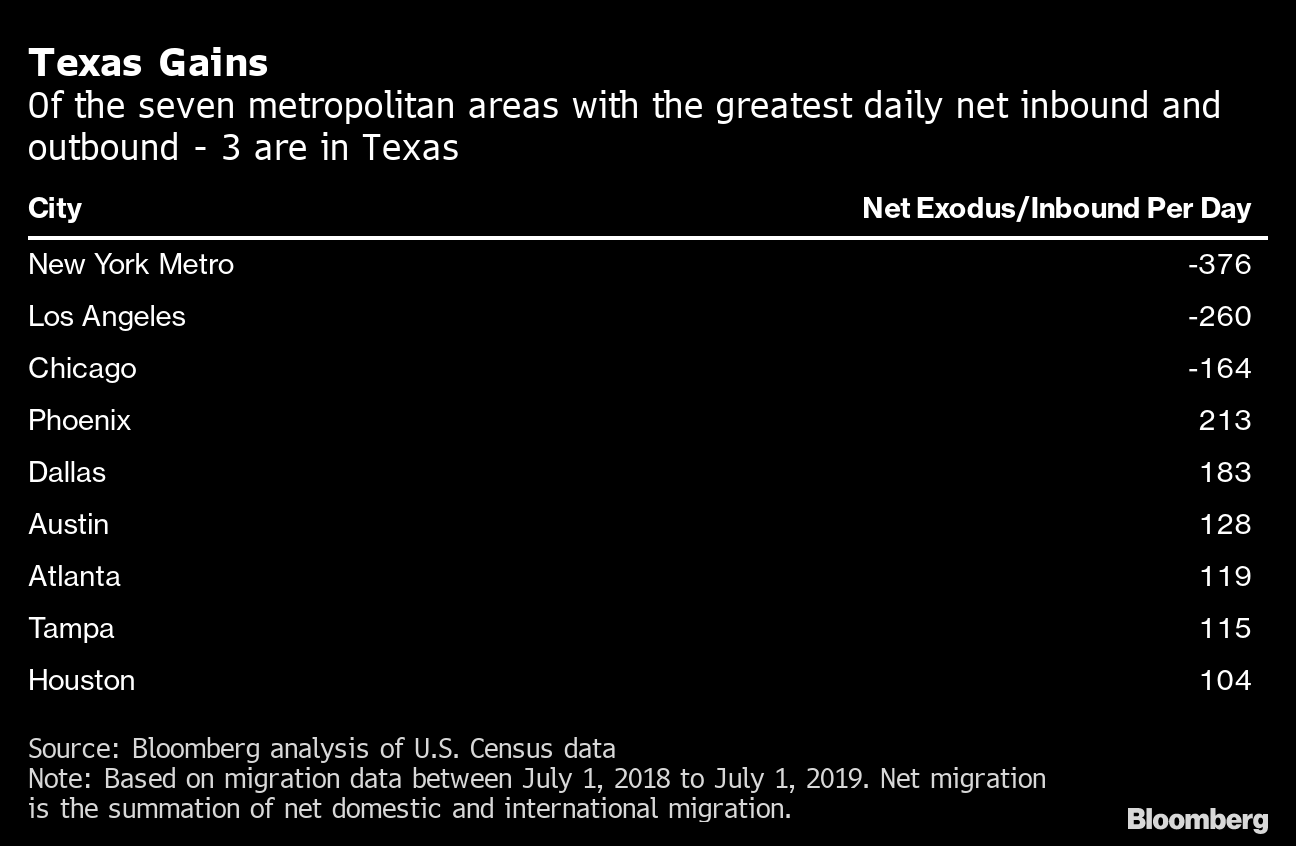

Texas was already in the midst of robust growth. In the past decade, Dallas and Houston added more people than any other metro areas, pushing the state population to about 29 million. Austin expanded at the fastest clip for urban areas of at least a million people.

The state picked up two seats in Congress over the last decade while California and New York each lost one. The Golden State lost population in 2020 for the first time. The most popular destination for people fleeing: Texas.

“The dynamic of people leaving the coasts and coming to places like Texas is a durable trend,” said Mark Okada, chief executive officer of Dallas-based Sycamore Tree Capital Partners, which he started last year with Jack Yang and Trey Parker to invest in alternative credit. He points out the state has an optimal tax rate, is a few hours flying distance from both coasts, and is only an hour behind New York.

Real estate agents are trying to keep up. Supply is limited in desirable neighborhoods, and it’s not unusual for houses to attract dozens of bidders -- many of them from California. In some cases, buyers are showing up without a job but with plenty of cash after selling their houses in more expensive locales.

WATCH: Austin, Texas Mayor Steve Adler discusses the large migration of technology industry workers to the city.

Source: Bloomberg.

The median home price in Texas jumped 14% in March to a record $283,200, spurred by a 29% surge in Austin and double-digit gains in Dallas and Houston, according to Texas A&M University’s Real Estate Research Center.

“It’s the reverse of the way people used to move to California,” said Marie Bailey, who relocated in 2017 to Dallas’s northern suburbs from the Los Angeles area and became a real estate agent. She started a Facebook group three years ago for Californians moving to Texas and recently surpassed 33,500 members.

Booms -- and busts -- have a long history in Texas. The oil and savings-and-loan industries both flamed out in the 1980s, leaving years of economic wreckage in their wake. These days, the state’s big cities are less dependent on petroleum and natural gas. Houston still the pain when energy prices fall, but the city can also fall back on big industries in aerospace and medicine, plus growing clusters in biotech and clean energy.

Property Taxes

The growth comes with headaches. Traffic is getting worse and public transportation is limited. The influx of people is driving up housing prices, forcing up the cost of living by boosting property taxes. Given high levies on real estate and the state sales tax, the fiscal burden on middle-class people is higher in Texas than in California, at least according to the Institute on Taxation and Economic Policy.

What’s more, Texas can be its own worst enemy when it comes to economic development. The state’s independent power grid failed under the strain of unusually cold temperatures in February, stoking doubts about Texas’s views on electricity deregulation and aversion to federal oversight.

And then there are the recent headlines out of Austin, where the state’s Republican-dominated legislature has spent the past few months taking on a raft of controversial measures, including restricting voting and abortion rights, expanding the ability to carry a gun without a permit, and limiting trans-gender kids’ participation in sports. The debates have drawn the ire of the national media, pleasing far-right conservatives and worrying moderates who fear that state’s brand will continue to become a caricature.

Texas Governor Greg Abbott

“We’re basically doing things that flat offend highly educated workers we need to attract,” said Ray Perryman, a former economist at Baylor University in Waco who has been tracking the Texas economy for 40 years.

Inequality Fears

Perryman said he’s also worried the state isn’t investing enough in health care or education. More than half of its school kids are Hispanic, but Hispanic families only control about 5% of the state’s wealth, he said. Black children make up more than 12% of students, and African-American families are similarly underrepresented in wealth accumulation.

“I fear that we’re not looking beyond our noses,” Perryman said.

For now, the rush is on. Alex Wilcox, CEO of a small upscale airline called JSX, moved the company to Dallas from California three years ago to tap a labor pool full of former employees of American Airlines Group Inc. and Southwest Airlines Co. He went looking for a home in the swanky Park Cities area, but instead ended up building a house on an empty lot.

“It sounds extravagant, but it was actually more economical than buying a place,” he said. “We spent half for a 5,000 square foot house of what we would have spent for half that size and 60 years old in Newport Beach.”

(Updates with comment from Canyon co-CEO in fifth paragraph.)

More stories like this are available on bloomberg.com

©2021 Bloomberg L.P.