Stocks, Futures Rise as October Optimism Continues: Markets Wrap

(Bloomberg) -- Asian stocks advanced alongside US equity-index futures, suggesting that the seven-month rally in global equities may still have room to run amid strong tech earnings and easing US–China trade tensions.

Contracts for the S&P 500 and the Nasdaq 100 rose 0.2% after the underlying gauges gained Friday, with earnings optimism outweighing worries about a rally that’s heavily concentrated on tech giants. Asian shares advanced 0.3%, with South Korea reaching a record, while Chinese indexes fell. Markets in Japan and cash trading of Treasuries were closed on Monday due to a holiday.

Commodity markets were in focus, with gold fluctuating after early declines following China’s scrapping of a long-standing tax incentive. West Texas Intermediate crude rose 0.5% after OPEC+ decided to pause output increases.

Stocks have rallied to record levels, even after Federal Reserve Chair Jerome Powell warned that a December rate cut isn’t a foregone conclusion and megacap tech earnings were mixed. Trade tensions have also eased, with Beijing signaling plans to suspend new export controls on rare earth metals and end investigations into US firms in the semiconductor supply chain.

“Powell’s FOMC press conference last week threw a curveball to the markets, but the broader context of a one-year ceasefire in the US-China trade relations and global AI boom should keep investors in a positive mood at the start of November,” said Homin Lee, a senior macro strategist at Lombard Odier Singapore. “The market’s focus will be on private sector data releases in the US as well.”

From geopolitics to trade risks, a US government shutdown and high valuations, traders had a lot to digest in October. Ultimately, what prevailed was confidence in US companies and bets that rate cuts will keep momentum going for profits. The artificial intelligence theme also remained a key driver as several megacap tech firms reported earnings.

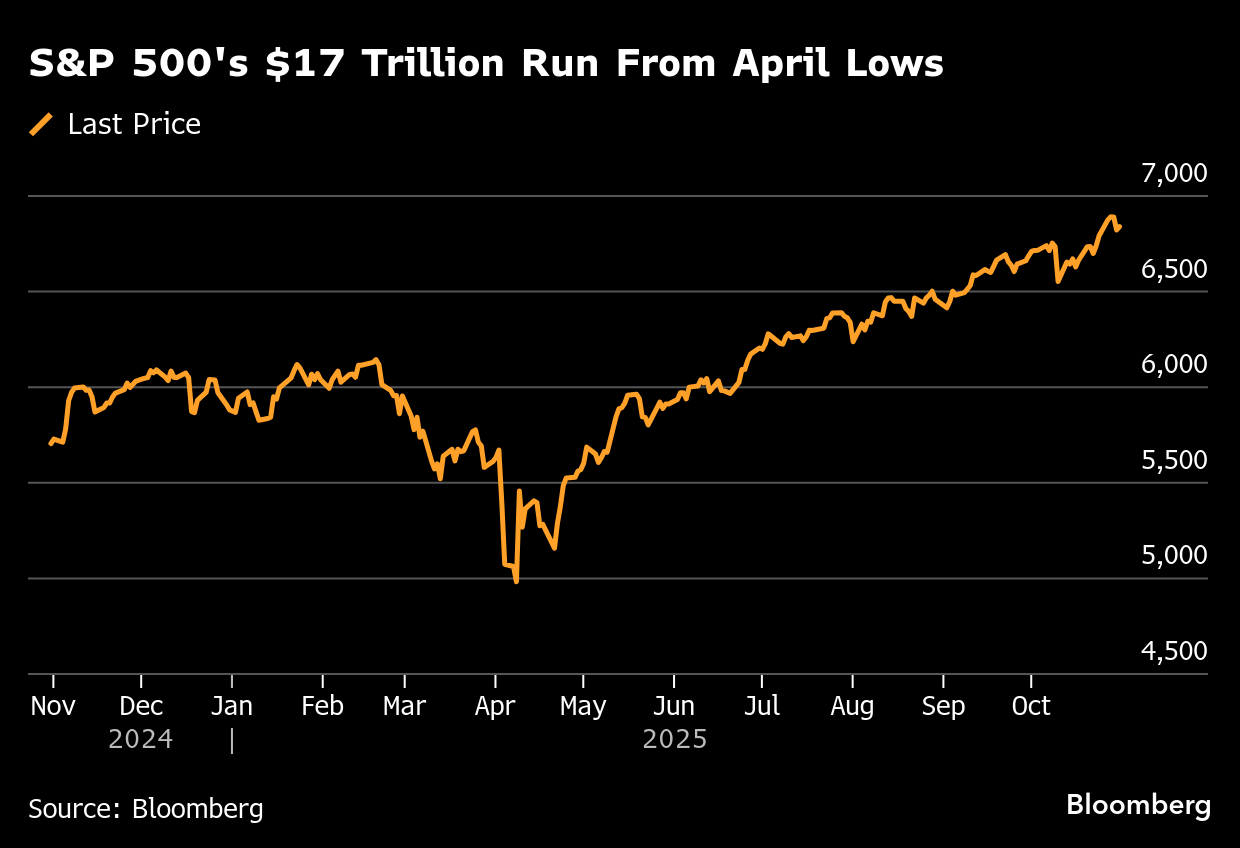

Since its April slump, the S&P 500 has roared back nearly 40%, marking its longest monthly winning streak since 2021. The Nasdaq 100’s performance has been even more striking: a seven-month rally, its best run in eight years, powered by tech’s strong balance sheets and unrelenting AI optimism.

The S&P 500 “will only pause running if something surprises meaningfully to the downside,” said Anna Wu, a cross-asset strategist at Van Eck. “In last week’s case, we had Xi-Trump talks disappoint moderately, but soon after, earnings took over again with Apple and Amazon reporting strongly. That strength is extending to this week, supporting overall risk sentiment.”

In other corners of the market, Treasury futures inched higher while Australian yields rose ahead of an interest rate decision by the country’s central bank on Tuesday. A gauge of the dollar steadied as investors awaited speeches from Fed officials for more clues on the central bank’s policy path.

Attention was also on commodities as China announced the scrapping of a long-standing gold tax incentive in a potential setback for consumers in one of the world’s top bullion markets. The precious metal surged to a record high in early October, aided by a buying frenzy among retail investors, before dropping sharply in the final two weeks of the month.

“The tax changes in gold’s heaviest consumer nation will dent global sentiment,” said Adrian Ash, director of research at BullionVault. “This news could prove very welcome to traders and investors hoping for a deeper correction after last month’s spike.”

Meanwhile, oil rose. OPEC+ said it will pause output increases after making another modest hike next month.

The move came as the market faces the prospect of a ballooning oversupply that has seen Brent lose 10% over the past three months. Prices have pulled back from a five-month low after increased US sanctions on Russia created question marks about the supply prospects from the major exporter.

Traders will also be watching a packed week for global central banks. Policymakers from Australia to Sweden and Brazil are expected to keep rates steady, while their counterparts in Mexico may deliver a cut. The Bank of England is expected to skip an interest rate cut on Thursday.

In the US, the ongoing federal shutdown continued to cloud the outlook by disrupting key economic data releases.

Corporate News:

- Berkshire Hathaway Inc.’s cash pile soared to $381.7 billion in the third quarter, a fresh record, and operating earnings surged 34% at Chief Executive Officer Warren Buffett’s conglomerate.

- Westpac Banking Corp.’s profit came in line with estimates as growth in mortgages and loans to businesses buoyed the Australian lender.

- Distressed Hong Kong builder New World Development Co. has launched an exchange offer for its outstanding perpetual notes, issuing up to $1.9 billion worth of new securities, according to an exchange filing.

- Two Singapore property asset managers are mulling a merger that could create one of Asia’s largest real estate firms with more than $150 billion under management, Dow Jones reported on Monday.

- China Vanke Co.’s bonds slumped after its state-owned shareholder pressed the developer to secure earlier loans with collateral — tightening financing terms just as Vanke reported a deeper third-quarter loss.

- The US auto safety regulator investigating whether certain Tesla Inc. door handles are defective received more complaints within days of initiating its probe from consumers who were unable to get into or out of their vehicles after battery failures.

- Pony AI Inc. is poised to raise HK$6.7 billion ($863 million) in its Hong Kong listing after telling prospective investors the Chinese autonomous-driving company plans to price shares at HK$139 each.

- BYD Co. shares neared the lowest in almost nine months Monday after the automaker posted its second consecutive drop in sales.

Some of the main moves in markets:

Stocks

- S&P 500 futures rose 0.1% as of 1:05 p.m. Tokyo time

- Australia’s S&P/ASX 200 was little changed

- Hong Kong’s Hang Seng rose 0.6%

- The Shanghai Composite was little changed

- Euro Stoxx 50 futures rose 0.2%

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro was little changed at $1.1535

- The Japanese yen was little changed at 154.05 per dollar

- The offshore yuan was little changed at 7.1178 per dollar

Cryptocurrencies

- Bitcoin fell 2.2% to $107,596.34

- Ether fell 3.5% to $3,724.32

Bonds

- Japan’s 10-year yield advanced one basis point to 1.655%

- Australia’s 10-year yield advanced six basis points to 4.35%

Commodities

- West Texas Intermediate crude rose 0.4% to $61.21 a barrel

- Spot gold rose 0.1% to $4,007.83 an ounce

This story was produced with the assistance of Bloomberg Automation.

©2025 Bloomberg L.P.