US Airstrikes on Iran: What Next for Oil Markets?

(Bloomberg) -- The oil market has been wrestling for days with President Donald Trump’s next act in an escalating Middle East conflict. Now American jets have struck Iran’s three main nuclear sites, a move that leaves traders preparing for a price surge — but still guessing where the crisis goes from here.

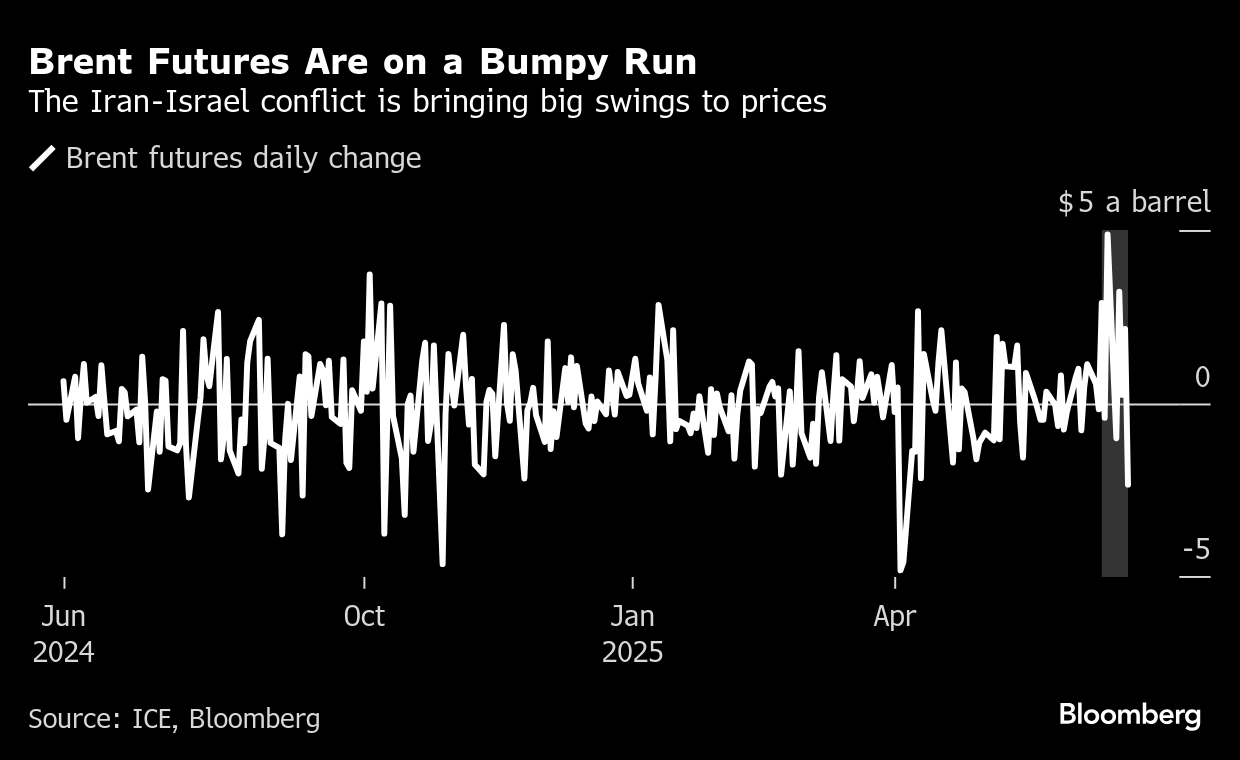

In a wild week, Brent futures have jumped 11% since Israel attacked its nemesis, but with sharp moves up and down from one day to the next. That rise is expected to restart on Monday, after the US assault — which targeted sites at Fordow, Natanz, and Esfahan — dramatically raised the stakes in a region that accounts for a third of global oil output.

From frenzied options markets, to soaring freight and diesel pricing, to a radical redrawing of crude’s pivotal forward curve, all of that volatility is expected to intensify in the week ahead.

“Much depends on how Iran responds in the coming hours and days — but this could set us on a path toward $100 oil, if Iran responds as they have previously threatened to,” said Saul Kavonic, an energy analyst at MST Marquee. “This US attack could see a conflagration of the conflict to include Iran responding by targeting regional American interests that include Gulf oil infrastructure in places such as Iraq, or harassing passage through the Strait of Hormuz.”

The maritime chokepoint at the mouth of the Gulf is a vital conduit for not just Iranian shipments, but also for those from Saudi Arabia, Iraq, Kuwait and other members of the Organization of the Petroleum Exporting Countries (OPEC).

Central to everything is the Trump administration’s ultimate intention in Iran, having joined Israel’s attack.

At one stage last week, it appeared more a question of when than if. That then changed late Thursday, when Trump said he’d mull his decision for two weeks. Then in the early hours of Sunday, Iranian time, he announced that Fordow, Natanz, and Isfahan were struck, and described a “payload of BOMBS” dropped on Fordow, a key location of uranium enrichment.

Hours later, in a televised address to the nation, the US president said the strikes had “totally obliterated” the trio of targets, while also threatening further military action if Tehran did not make peace with Israel.

“The market wants certainty, and this now firmly pushes the US into the Middle East theater,” said Joe DeLaura, a former trader and global energy strategist at Rabobank, adding prices were now expected to rise when oil reopens. “But I think that this means the US Navy will be tasked to keep the Strait open,” he said, adding prices could head into the $80-to-$90 a barrel range.

Still, so far there has been little sign of disruption to oil flows from the region.

“Should the US provide direct military support to Israel and play its part in removing the current regime the initial market reaction will be a price spike,” said Tamas Varga, an analyst at brokerage PVM Oil Associates Ltd, said at the end of last week. But his firm’s expectation is that oil will not become part of the conflict because it’s not in the interests of either side.

The fate of oil matters because it drives fuel prices and inflation — something Trump said he would quell when he was campaigning for office. In times of extreme volatility, shortages of oil have even precipitated recessions.

So far, there’s been no meaningful curtailment through the Strait of Hormuz, through which about a fifth of the world’s produced and consumed oil flows every day. Indeed, Iran even appears to be racing to lift its exports as part of its logistical response to the conflict.

Avoiding a wider conflagration and preventing disruptions to supply would push oil prices lower, while also bringing down everything that spiked in tandem with them. Against that, America joining could be all-defining, calling into question security through the waterway and from the region at large.

On Friday, Iran said it might consider adjustments to its enrichment program, driving down futures and reminding the world that Tehran’s actions are important to petroleum markets too.

Among assets roiled by the tension are options contracts, where traders paid enormous premiums to hedge against further price spikes.

At times since the conflict began, they paid the most to protect against a rally since at least 2013. Record volumes of bullish call options have changed hands since the attacks started.

Exiting Trades

The market, though, was on edge even before Trump’s announcement.

Traders have been exiting futures positions at one of the fastest rates on record — an indication of both the stress that higher levels of volatility is placing on derivatives books, and the unpredictable path ahead.

In total, the number of futures contracts held on the main exchanges plunged by the equivalent of 367 million barrels, or about 7%, since the close on June. 12, the eve of Israel’s attack. Traders and brokers say the higher levels of volatility have made pricing deals harder over the past week.

“Traders and analysts should be viewing the current oil price gyrations in the context of speculative de-risking,” said Ryan Fitzmaurice, senior commodities strategist at Marex Group Plc. “Going forward, market volatility and open interest will be key areas to watch.”

The cost of hiring a ship to carry crude from the Middle East to China has jumped close to 90% since before Israeli attacks began. Earnings for vessels carrying fuels like gasoline and jet fuel have also leaped, as have insurance premiums.

The danger to vessels in the region’s waters was underscored when two oil tankers crashed into each other causing a fiery explosion — though on this occasion, the ship’s owner asserted there was no link to the conflict.

Still, almost 1,000 ships a day are having their GPS signals jammed, creating growing safety risks. The MICA Center, a French liaison between the military and commercial shipping, said the tanker crash was likely “aggravated” by jamming.

“Next days will be critical in determining whether a diplomatic solution with Iran is possible and if the US might resort to military action,” it said in an update. “Maritime trade is not being targeted. The situation might change abruptly.”

The risk to flows from the region, coupled with the sharp increase in shipping costs, is bolstering demand for crudes from outside of the Gulf.

Pullback Risk

The higher different prices race, the greater the risk of a pullback if the prospect of de-escalation takes shape.

And even if tensions do remain high, there’s precedent from a few years ago for a meaningful supply disruption to quickly get resolved.

When an attack in 2019 on processing facilities at Abqaiq in Saudi Arabia knocked out 7% of global supply, it took just a few weeks for crude futures to trade lower than before the attacks occurred, as supplies were quickly restored and backfilled.

That’s one reason, coupled with a persistent threat of geopolitical risks that often don’t morph into real supply curbs, why traders say prices haven’t spiked more in recent days.

“This is the big one,” said John Kilduff, a partner at Again Capital, pointing to a $8-a-barrel risk premium as plausible. “The market default on this development is higher. How high depends on Iran’s response — or the realistic prospects of a meaningful response, which may not be there.”

©2025 Bloomberg L.P.