Oil Drops as Tariff Fallout Overshadows Risks to Russian Supply

(Bloomberg) -- Oil fell as US President Donald Trump reignited his global trade war, while his latest plan to pressure Russia into a ceasefire with Ukraine didn’t include new measures aimed directly at hindering Moscow’s energy exports.

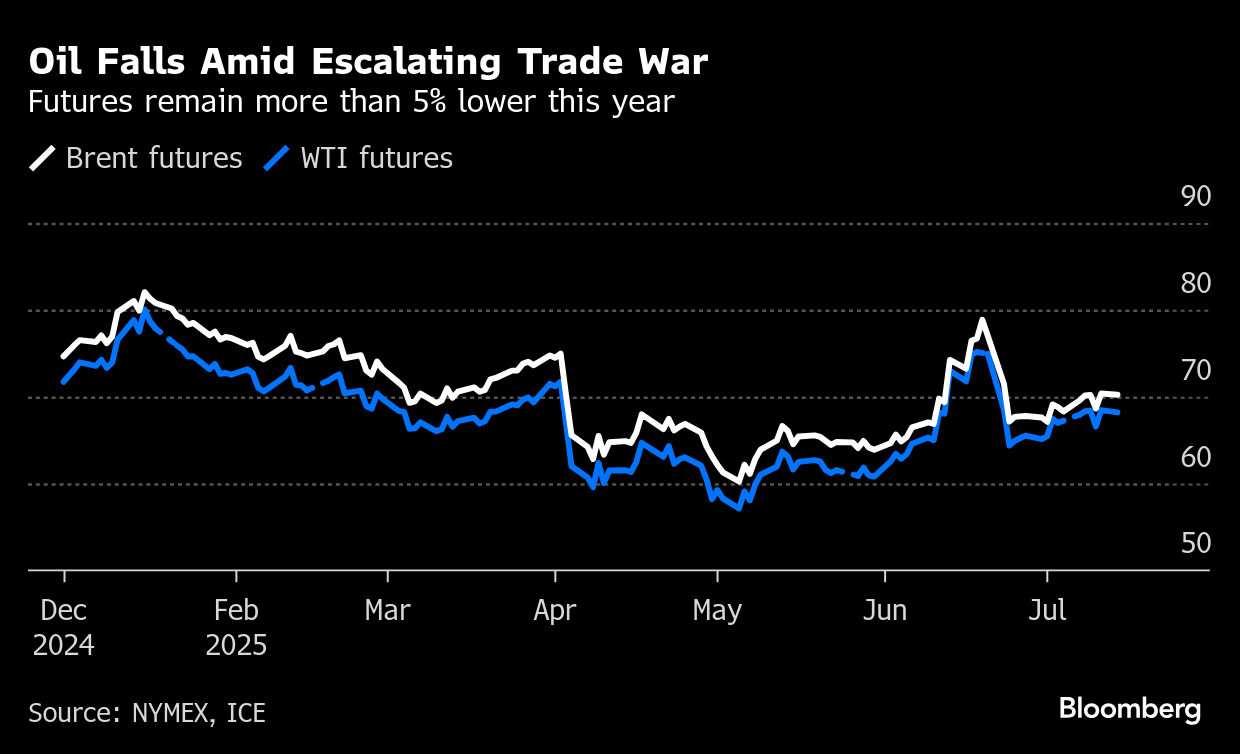

West Texas Intermediate slid more than 1% to trade below $68 a barrel after Trump threatened 30% tariffs on goods from the European Union and Mexico over the weekend, hurting the outlook for energy demand.

Meanwhile, his latest push to resolve the Ukraine war included threatening 100% “secondary” tariffs on countries that do business with Russia if there’s no ceasefire in 50 days. But he didn’t announce direct sanctions on the nation’s oil shipments, which traders had speculated might be coming when Trump promised a “major statement” on Russia last week. Oil slipped to intraday lows after he released details of the plan.

Trump’s barrage of tariff demand letters last week contained some of the highest tax rates yet on major US trading partners. The attacks revived concerns that energy demand would deteriorate and added to widespread expectations of a glut later this year, leading hedge funds to turn bearish on oil at the fast pace since February last week.

In the near-term, though, demand appears to be holding. China ended the first half of the year with a record trade surplus, with factories riding out the tariff roller-coaster. The trade data also showed that crude imports have risen so far this year. The country’s purchases of Iranian barrels jumped in June, according to data from Vortexa.

Oil is still more than 5% lower this year as traders and investors balance geopolitical tensions in the Middle East, which stoked concern over supplies, with the US-led trade war. OPEC+ is relaxing supply curbs, which could lead to an oversupply in the second half of the year.

Traders are now looking ahead to Tuesday’s US consumer price index data for clues on the path forward for monetary tightening.

©2025 Bloomberg L.P.