Oil Feels Sting of Recession Concerns as Weekly Losses Pile Up

(Bloomberg) -- Oil headed for a third weekly drop, its longest losing run this year, on concern that a potential recession will cut into energy demand.

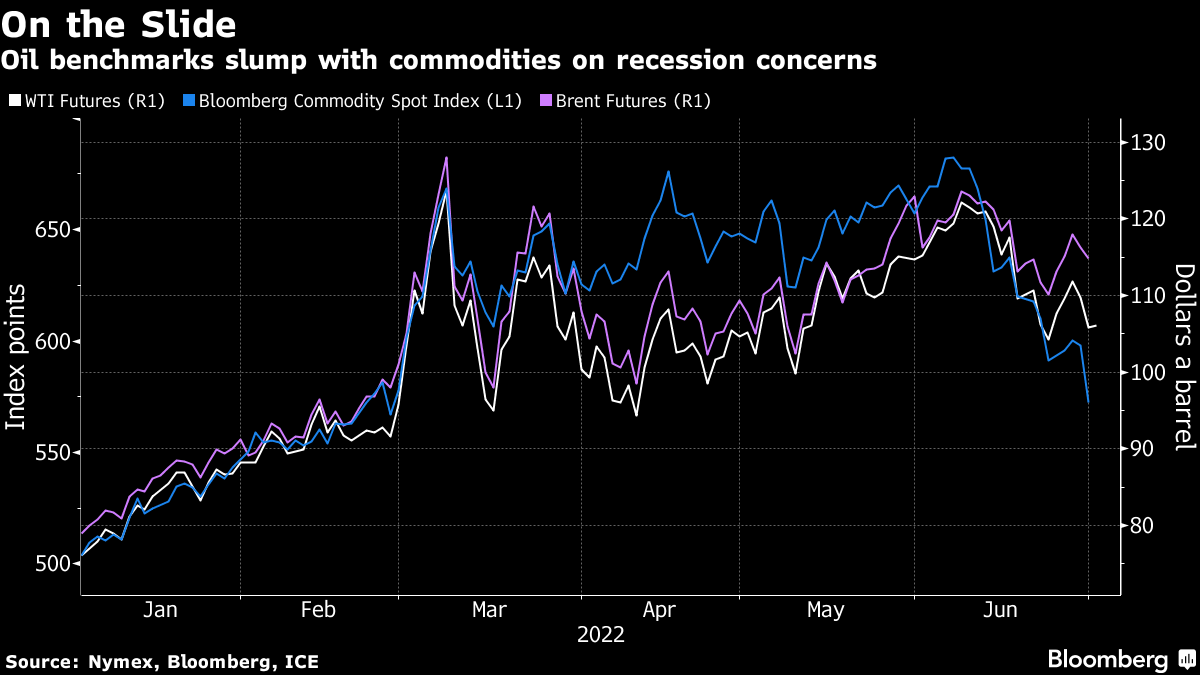

West Texas Intermediate fell toward $105 a barrel after tumbling on Thursday as commodities were pummeled. The US benchmark has shed more than 2% this week despite signs that the physical crude market remains tight.

India on Friday increased levies on exports of gasoline and diesel as part of a drive to control a fast-widening currency deficit. The nation has become an important destination for Russian crude this year as other nations shun flows because of the war in Ukraine. The new levies may crimp product exports.

Oil fell about 8% in June as investors fretted over a potential global slowdown, eroding a rally spurred by the war in Ukraine, interruptions to supplies and rising demand. The jump in prices alarmed President Joe Biden, who’s spearheading efforts to get producers in the Middle East to boost crude output.

“Oil may remain choppy,” said Zhou Mi, an analyst at Chaos Research Institute in Shanghai, which is affiliated with Chaos Ternary Futures Co. Deepening recession fears would hurt oil products and squeeze refining margins, although high run rates are offering support with fundamentals still tight, said Zhou.

As crude backtracked on Friday, commodities suffered a fresh wave of selling, with copper and iron ore among the biggest losers. Since hitting a record in early June, the Bloomberg Commodity Spot Index has sunk 16%. The dollar rose, making raw materials more expensive for holders of other currencies.

Data this week showed weakness in US consumer spending, which is by far the biggest contributor to gross domestic product. That follows a pivot by the Federal Reserve to aggressively tighten policy to quell raging inflation.

The Organization of Petroleum Exporting Countries and its allies ratified an oil-production increase this week, completing the return of supplies halted during the pandemic. Biden will travel to the Middle East later this month to urge Saudi Arabia and the United Arab Emirates to increase supplies further.

In a sign that US demand remains robust for now a record number of drivers are expected to hit the road this weekend for Independence Day travel, buttressing gasoline consumption. Average retail pump prices have eased slightly in recent weeks after hitting a record above $5 a gallon in June.

Oil’s time spreads, which traders track for indications on the strength of underlying demand, continue to flash broadly positive signals. Brent’s prompt spread -- the difference between its two nearest contracts -- was $3.50 a barrel in backwardation, up from $2.73 a month ago.

Economic data from Asia, however, pointed to weakening conditions. Purchasing manager indexes from across the region eased in June, with South Korea and Thailand among those showing the biggest declines, according to S&P Global.

“For oil, it is clear that macro developments are still the key driver for price direction at the moment,” Warren Patterson, the Singapore-based head of commodities strategy at ING Groep NV, said in a note. “Fundamentally, the market is still tight, so we expect only limited downside in prices.”

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.