Oil Traders Pile Into $70-a-Barrel Longer-Term Crude Price

(Bloomberg) -- Oil traders are betting that longer-term crude prices could be set to spike because of a lack of investment in future supply.

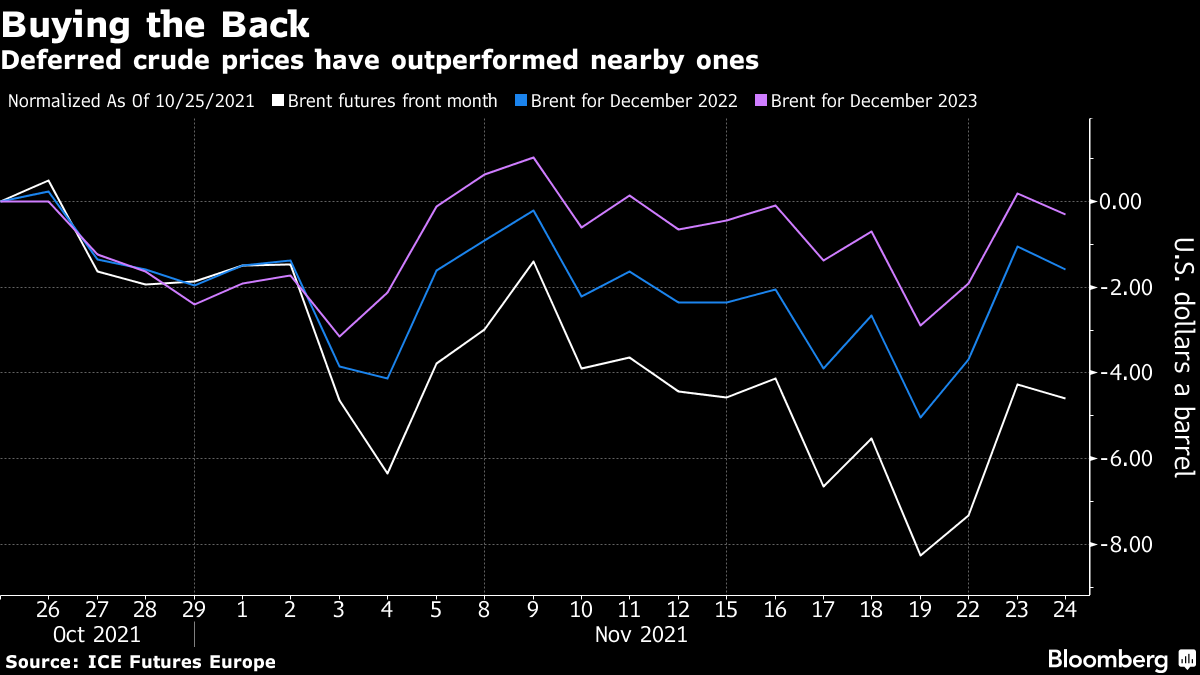

Since hitting their high for the year last month, the most-active oil futures have fallen almost 5%. By comparison, those for late 2022 and 2023 have barely moved, sticking above $70 a barrel.

With nearby contracts rattled by U.S.-led efforts to boost supply -- and the potential for an OPEC+ backlash -- those further out are being boosted by dwindling investment in production, and a dearth of producers selling deferred futures to lock in their future sales.

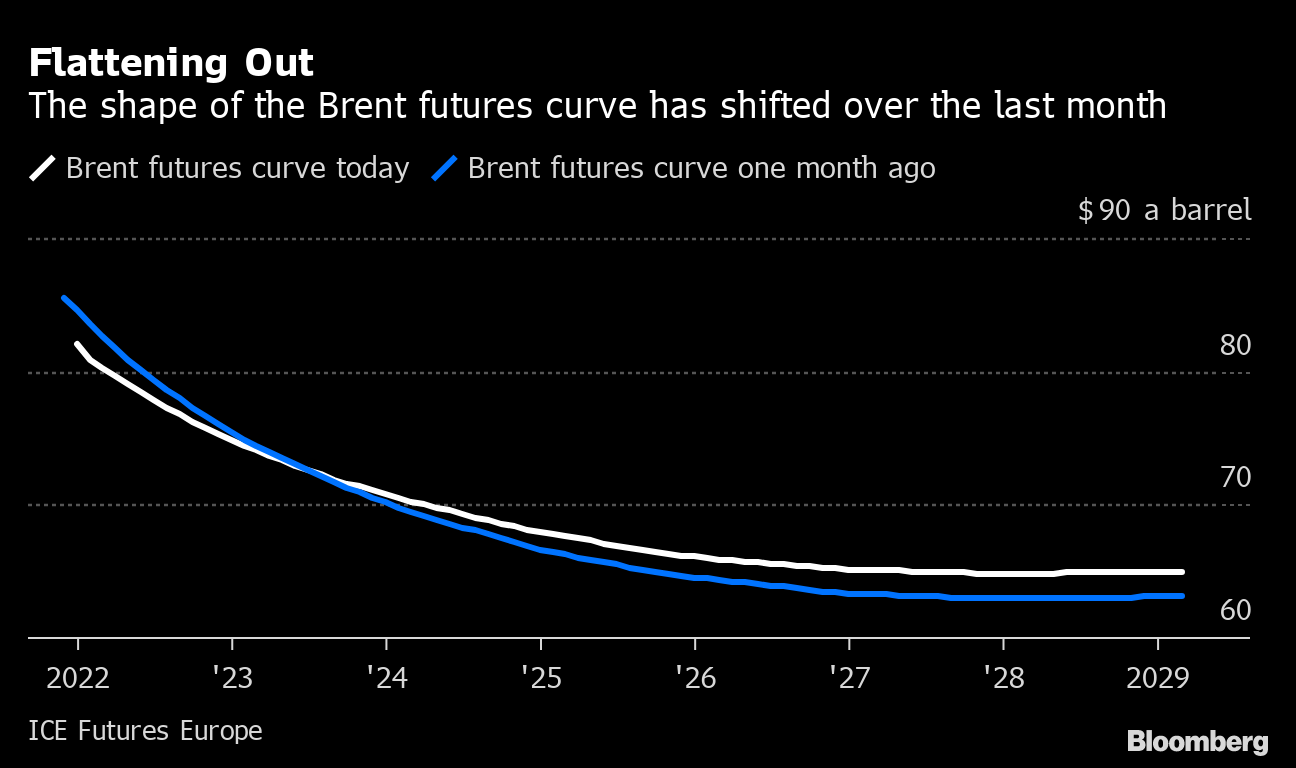

For much of the past two months, the market has been veering on the point of a super-backwardation -- industry speak for a steeply downward sloping curve that indicates tight supply. But in recent weeks there has been a shift, flattening that structure, as traders bet that robust demand and falling investments in new supply will keep the market tighter for longer.

“I think forward oil prices will roll up beyond spot prices,” said Marwan Younes, Chief Investment Officer at Massar Capital Management LP, which has about $970 million under management across commodity and macro markets. “The world can decarbonize but the sources of oil are easier to shut down than the demand. You’re going to see prices rise higher than you would expect if you had normal producer hedging.”

The views echo comments from officials at some of the world’s largest banks and commodity trading houses over the past few weeks.

During that period, U.S. President Joe Biden has been orchestrating global efforts to release strategic petroleum reserves, something that finally happened on Tuesday. The market is now waiting to see what, if anything, OPEC and its allies do in response when they meet early next month.

“Most market participants that we talk to are still inclined to be constructive,” said Michael Tran, an analyst at RBC Capital Markets. “Over the past several weeks, many who didn’t want to get caught up in the policy back and forth with Biden seemed to move risk away from the front and allocated more risk along the term.”

The slowdown in spending shows up in industry figures. The number of rigs drilling for oil and gas across the globe is down about 30% compared with where it was before the virus hit. At the same time, demand recently returned to pre-pandemic levels, according to Vitol Group, with several other major traders putting demand in a similar ballpark.

Trafigura Group, one of the world’s largest commodity trading houses, has said that prices for December 2022 and 2023 are still cheap around $70 a barrel as prices could reach $100.

Deferred prices matter because they influence the pace of spending on future supply.

OPEC Plans

Still, buying into looming-supply-shortage theories -- a lingering concern in the market for several years now -- is fraught with risk.

With demand growth set to relent toward the end of the decade it is possible OPEC and its allies decide to try and pump more oil sooner in order to make the most of their resources while demand is still strong, according to Greg Sharenow, a portfolio manager focused on energy and commodities at Pacific Investment Management Co.

“If you’re in a world with a deceleration of demand growth, particularly for refined crude oil, the supposition that OPEC+ members don’t revisit how they approach their reserves is one that could see revisions in time,” Sharenow said. Still, “as investment into long-lived assets becomes more complicated, it is potentially net-bullish to price,” as the risks of investing in assets over the long-term become harder to assess, he added.

The bullishness is also about the hedging activity -- or lack of it -- from companies that pump oil.

As crude prices have embarked on their 60% rally this year, producers have been steadily scaling back their hedge books, ensuring that they are exposed to the full extent of the market’s rally -- while also putting themselves at risk if the market plunges.

Pioneer Natural Resources Co. said it won’t add any hedges for the foreseeable future, while Continental Resources Inc. has also said it’s largely unhedged. And it’s a momentum that’s not just restricted to the U.S. shale patch. North Sea producer Neptune Energy has said it is limiting its hedges too.

That leaves traders facing less selling pressure when buying the back of the oil curve, compared to the politics-driven price swings that have dominated headline prices since late-October.

“The US-led effort to reduce crude prices in the short run will -- with all else held equal -- result in higher prices next year,” Energy Aspects analysts including Amrita Sen wrote in a report. “While prompt prices might be volatile, the back end of the curve is likely to move higher on the need to refill inventories.”

More stories like this are available on bloomberg.com

©2021 Bloomberg L.P.