Options Markets Show Traders Reposition as Mideast Tension Fades

(Bloomberg) -- Stocks hit record highs last week and energy futures retreated after Middle East tensions eased. But in some parts of the options markets, there are still signs of stress as investors position for potential geopolitical and macroeconomic upsets.

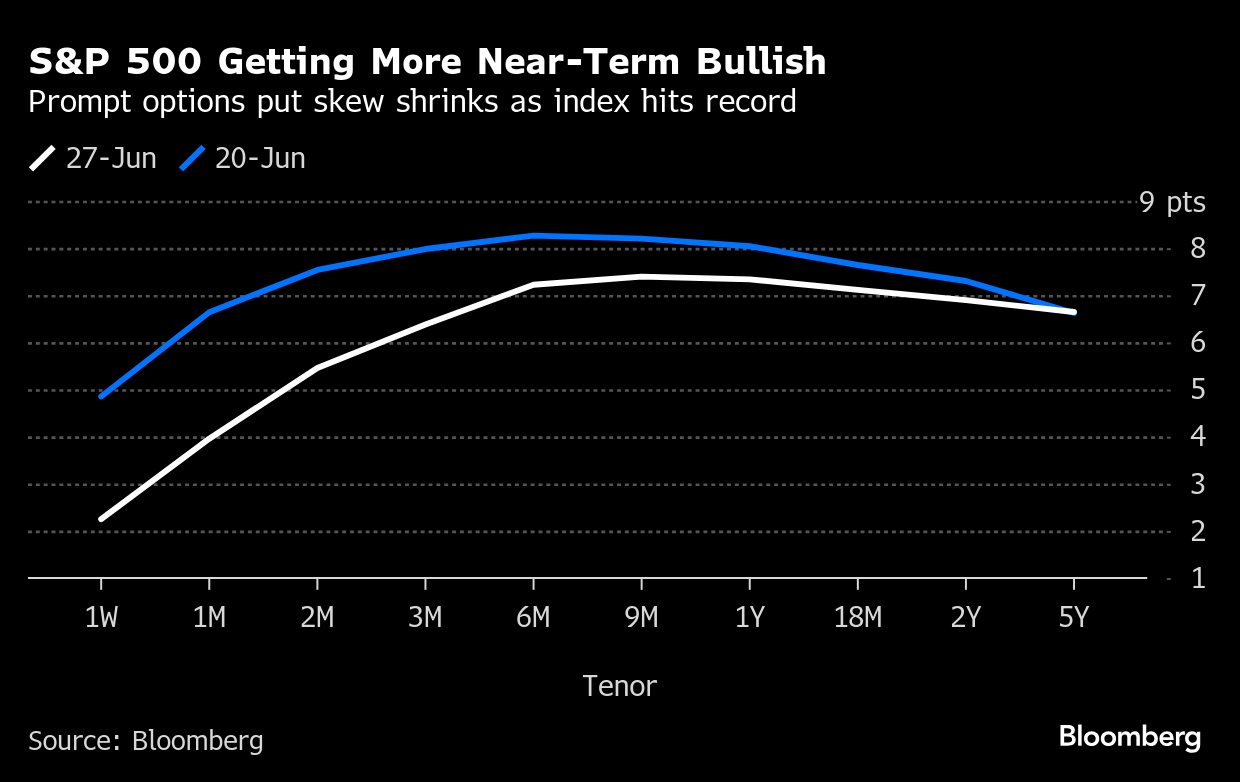

In the short term, equity investors are getting more bullish, with the premium for puts shrinking. But longer term, skew has barely changed, signaling less enduring optimism. Likewise, longer-dated futures on the Cboe Volatility Index have remained higher, showing more deferred angst around the economic impact of tariffs.

“Derivative markets have not fully returned to February levels,” Rocky Fishman, the founder of research firm Asym 500 LLC, wrote in a note Friday. “This shows a justifiable lasting effect of April’s volatility. The VIX futures curve has steepened, leaving the six-month area of the curve at a level that was rare in much of 2023-24.”

There were signs of VIX call buying last week, when the Cboe VVIX Index — the so-called vol of vol — dropped below 90, which has been the lower end for the measure since last July.

Oil markets are also slow to fully recover from the Israel-Iran conflict, even as attention is turning back to economic and fundamental factors. Brent implied volatility has fallen to the levels from early June, and the skew is flat, indicating there’s no bullish or bearish bias. Still, bets for crude swings hold a wider premium to equities, after the S&P 500 Index’s rally to a peak has put options under pressure.

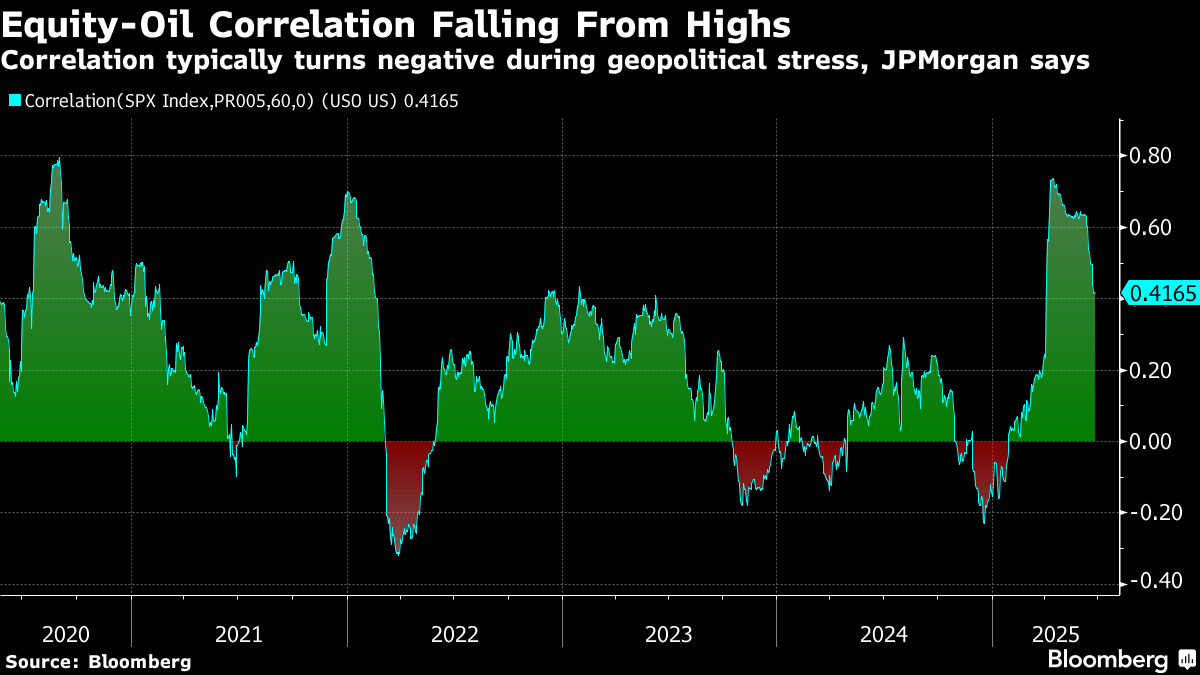

In a note last week, JPMorgan Chase & Co. derivatives strategists including Emma Wu suggested equity-oil hybrid trades, saying crude prices could rise should Middle East stress flare back up just as stocks may fall with interest rates staying higher for longer. While correlation between the two asset classes recently reached a high, they highlighted that the relationship tends to turn negative in periods of geopolitical tension.

The fast-evolving geopolitical situation has given many investors whiplash. Hedge funds and other large money managers cut their net-long positions in Brent crude futures and options by the most since early April in the week through June 24, according to ICE Futures Europe data, after building up the largest bullish position in 11 weeks.

And it’s not just for oil. In the European natural gas market, trend-following Commodity Trading Advisors flipped to 18% net shorts from 9% net longs last Tuesday, according to data from Bridgeton Research Group LLC. The algorithms often exacerbate market moves, making it harder for traders with physical exposure to navigate the market.

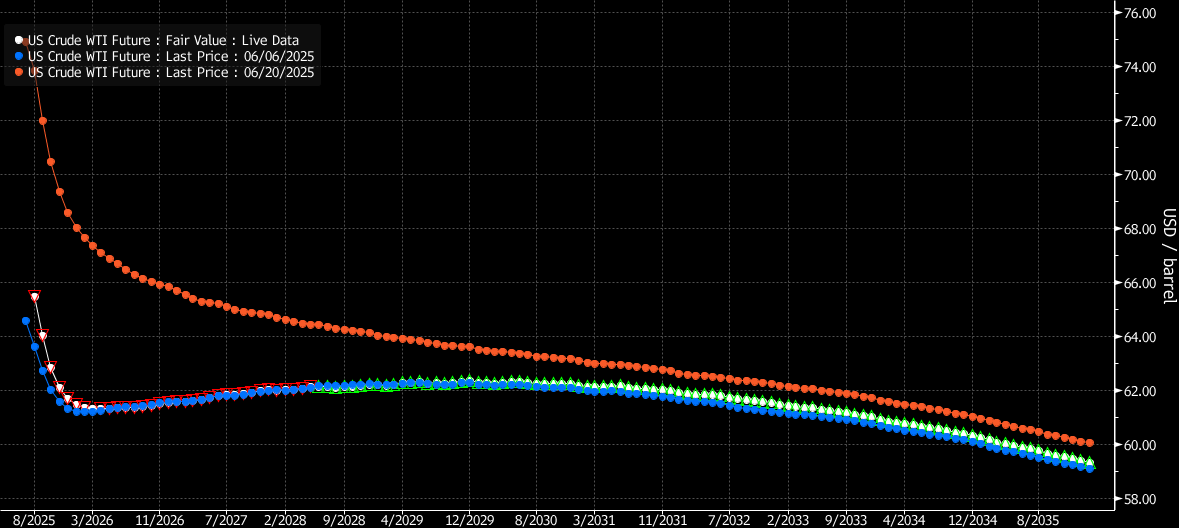

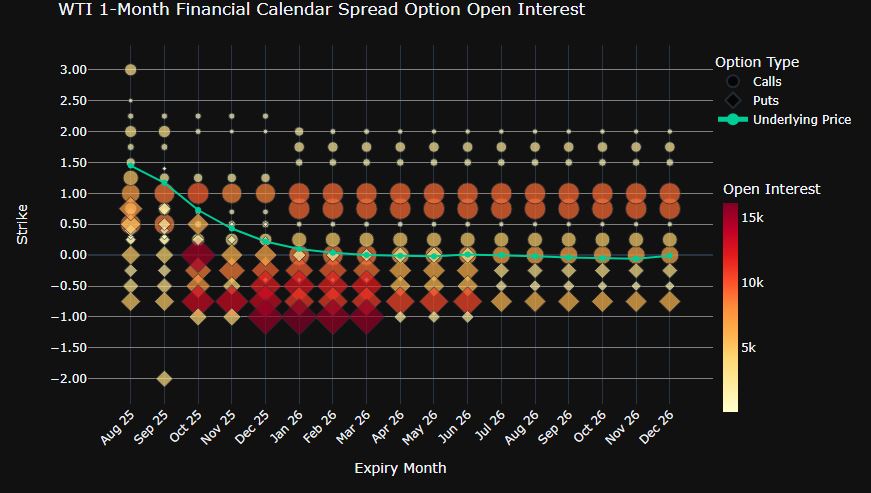

One area that has seen a rare influx of investor interest has been calendar spreads on crude oil, with options open interest reaching a record high this month. In an unusual situation, traders had bet that short-term tightness could reverse to a glut as OPEC and other producers add barrels to the market just as an uncertain economic outlook risks crimping demand. That “hockey-stick” shaped curve — which disappeared due to the Israel-Iran attacks — has reverted to where it was three weeks ago.

“The sharp drop in the geopolitical risk premium likely reflects traders’ recent experiences with major geopolitical shocks without significant oil disruptions, Iran’s restrained response, strong US and China incentives to avoid large disruptions, and the likely shift to large inventory builds from the fall,” Goldman Sachs Group Inc. analysts including Yulia Zhestkova Grigsby and Daan Struyven wrote in a note.

©2025 Bloomberg L.P.