Oil Extends Drop Below $100 as U.S. Plans Huge Reserves Release

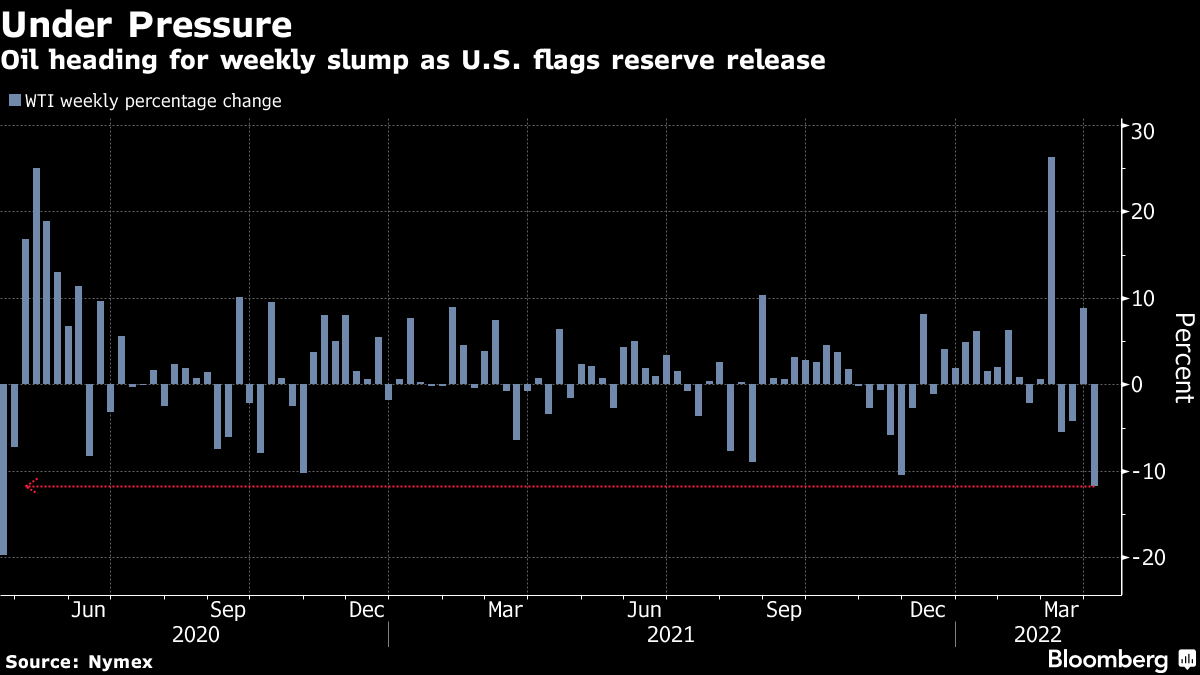

(Bloomberg) -- Oil slid below $100 a barrel and is heading for the biggest weekly loss in almost two years after the Biden administration ordered an unprecedented release of strategic U.S. reserves to tame rampant prices

West Texas Intermediate futures lost as much as 1.7% on Friday after tumbling 7% in the previous session. The U.S. plans to release 1 million barrels a day for six months, although analysts warned any reprieve would be short-lived. The news filtered into the market early on Thursday, just before the OPEC+ alliance gathered to ratify a modest increase in supply for May.

Russia’s war in Ukraine has roiled global commodity markets and driven up the price of everything from food to fuels, challenging governments seeking to encourage economic growth after the pandemic. It’s led to tumultuous trading in the oil market, with wild swings during sessions throughout March.

President Joe Biden blamed a spike in gasoline prices this year on his Russian counterpart Vladimir Putin and the invasion of Ukraine, calling it “Putin’s price hike.” He also criticized U.S. oil companies that have been reluctant to boost production. The cost of retail gasoline at the pump was already high prior to the invasion, but the war has turbocharged prices worldwide.

The U.S. has already tapped its reserves twice in the past six months but it’s done little to cool prices. As much as 180 million barrels may be released this time, and Biden said he expects allies to release 30 million to 50 million more barrels from their own reserves. American physical crude prices tumbled.

The release by the U.S. and potentially other countries will not have a material impact on the supply-demand balance, said Jeffrey Halley, a senior market analyst at Oanda Asia Pacific Pte. Brent crude will likely fluctuate in a broad range of $100 to $120 a barrel in the weeks ahead, he added.

Goldman Sachs Group Inc. cut its forecast for Brent in the second half by $10 a barrel to $125 following news of the U.S. release. The bank said in a note that the release won’t resolve “oil’s structural deficit.”

The market also faced pressure this week from concerns about Chinese demand as the world’s biggest oil importer implements a series of lockdowns to curb a virus resurgence. Those curbs are starting to have an impact on the economy, with manufacturing activity contracting in March.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.

KEEPING THE ENERGY INDUSTRY CONNECTED

Subscribe to our newsletter and get the best of Energy Connects directly to your inbox each week.

By subscribing, you agree to the processing of your personal data by dmg events as described in the Privacy Policy.

More oil news

Asian Stocks Fall as China’s Confab Disappoints: Markets Wrap

China’s Weak Winter LNG Demand Provides Relief for Rival Buyers

Oil Edges Higher Ahead of US Inflation Figures and OPEC Report

Oil Slips as Glut Outlook Outweighs Optimism on China Stimulus

Oil Edges Higher as Traders Weigh Fallout From Syrian Upheaval

China’s Solar Industry Looks to OPEC for Guide to Survival

Five Key Charts to Watch in Global Commodity Markets This Week

Oil Steadies as OPEC+ Opts Again to Delay Plan to Restore Output

NMDC LTS to acquire 70% equity stake in Emdad